Savory Ingredients Market Summary

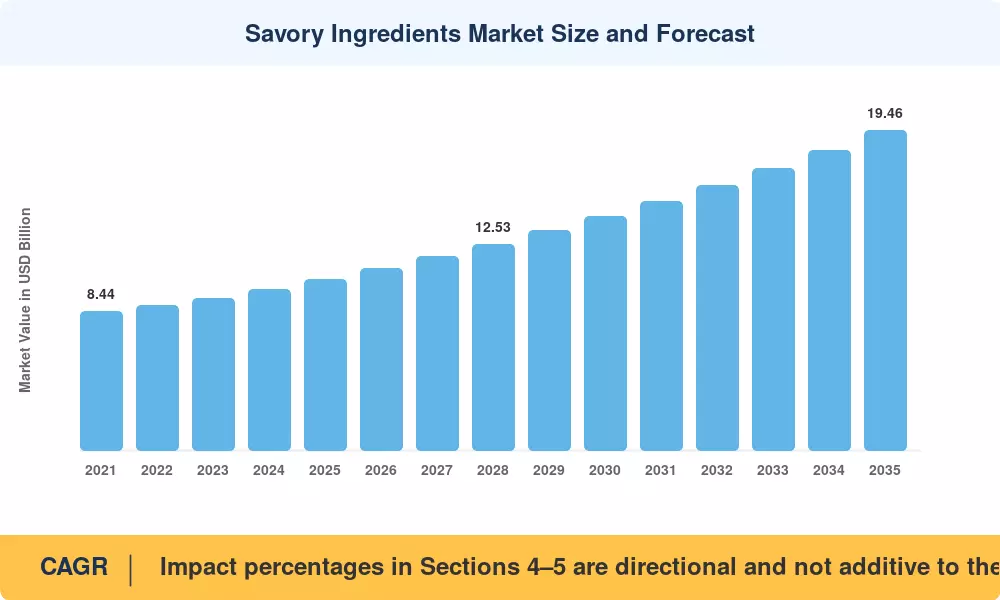

The Savory Ingredients Market reached a valuation of USD 10.38 Billion in 2025, with a forecast starting point of USD 11.05 Billion in 2026 and an expected trajectory toward USD 19.46 Billion by 2035, reflecting a compound annual growth rate of 6.50% across the forecast window. Two primary catalysts underpin this expansion: tightening sodium-reduction mandates across major food-regulatory bodies (the EU's Farm-to-Fork sodium targets and the FDA's voluntary sodium guidance for packaged foods) and the accelerating consumer pivot toward clean-label formulations that demand recognizable ingredient lists [1][2]. These policy and preference shifts are compelling food manufacturers to rethink seasoning architectures, channeling billions in reformulation budgets into savory ingredient innovation.

A meaningful transformation is reshaping how the industry produces flavor-active compounds. Traditional chemical synthesis routes for glutamate-based seasonings are giving way to precision-fermented nucleotides and continuous-fermentation yeast extract processes. Capital expenditure in fermentation-based flavor production exceeded USD 1.2 Billion globally during 2023–2024, as mid-tier producers challenged legacy spray-drying incumbents on cost-per-kilogram metrics [3][4]. The result is a supply landscape where bio-derived ingredients are approaching price parity with their synthetic counterparts roughly two to three years ahead of earlier projections.

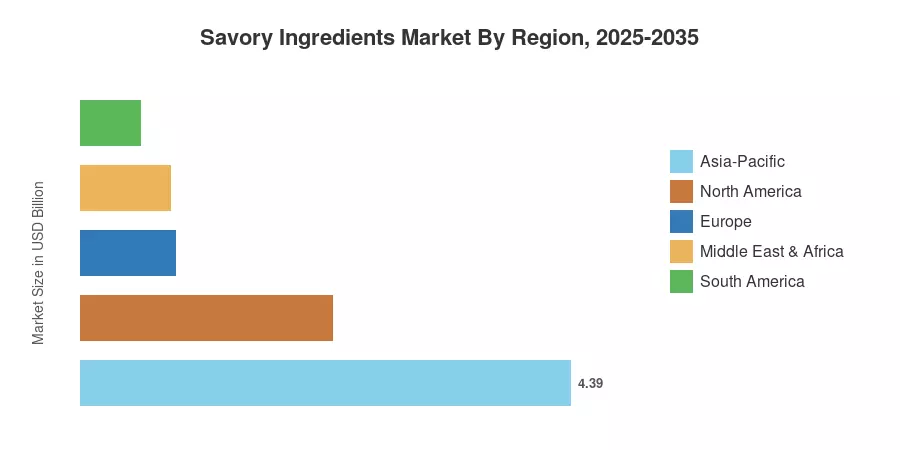

From a geographic standpoint, Asia-Pacific commands the largest share of the Savory Ingredients Market at approximately 42.3% of global revenue in 2025, driven by massive processed-food output in China, India, and ASEAN economies. Europe is advancing as the fastest-growing region at a CAGR of 8.15% through 2035, propelled by stringent clean-label regulation and premiumization trends. North America holds the second-largest position, anchored by the snack and ready-meal reformulation cycle underway among major CPG brands. The decade ahead will be defined by the intersection of regulatory pressure, fermentation economics, and consumer transparency demands.

Key Report Takeaways

• By Type

- Yeast extracts accounted for 38.1% of the Savory Ingredients Market in 2025, reflecting their versatility across snack seasoning and soup-base applications.

- Nucleotides are projected to register a CAGR of 8.13% from 2026 to 2035, fueled by precision-fermentation scale-ups and sodium-reduction regulations.

• By Form

- Powder formats represented 61.4% of the Savory Ingredients Market in 2025, remaining the dominant delivery vehicle for seasoning blends.

- Liquid and paste formats are forecast to expand at a 7.56% CAGR through 2035 as ready-meal and sauce manufacturers demand pumpable ingredient solutions.

• By Application

- Snacks captured USD 3.57 Billion of the Savory Ingredients Market in 2025, underscoring the category's role as the single largest demand pool.

- Ready meals are expected to grow at an 8.42% CAGR through 2035 as convenience-food penetration rises in emerging economies.

• By Region

- Asia-Pacific held a 42.3% share of the Savory Ingredients Market in 2025, supported by high per-capita seasoning consumption in China and Southeast Asia.

- Europe is forecast to advance at an 8.15% CAGR between 2026 and 2035, driven by EU clean-label mandates and premiumization.

Savory Ingredients Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines primary interviews with ingredient suppliers, food manufacturers, and trade-association datasets, triangulated against customs-trade data and company filings. Historical figures (2021–2024) are validated against industry-association volumes; forecast projections (2026–2035) apply econometric modeling anchored to the 6.50% CAGR.