Savory Snacks Market Summary

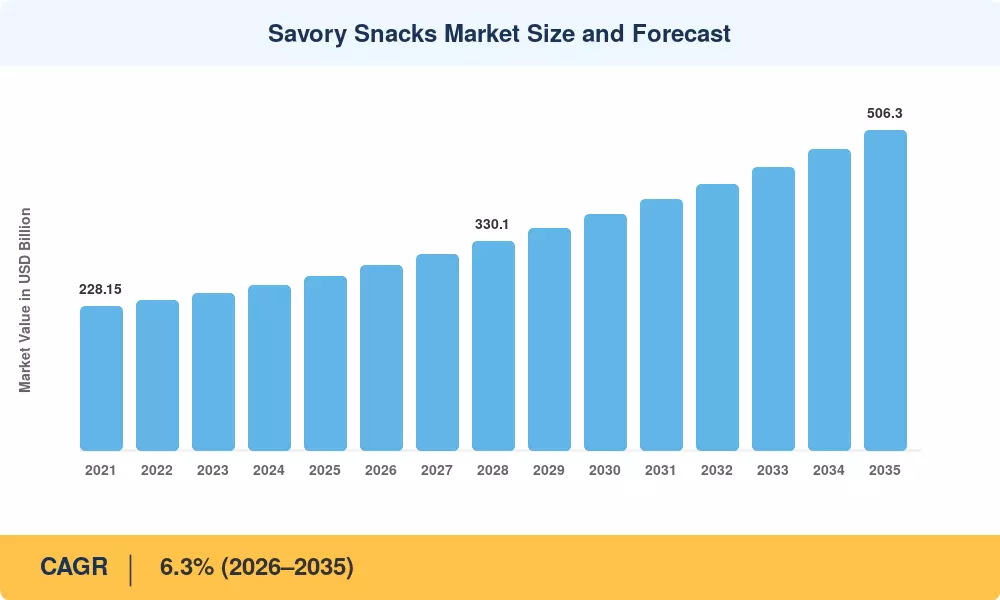

The global Savory Snacks Market was valued at USD 274.82 billion in 2025 and is projected to grow from USD 292.13 billion in 2026 to USD 506.30 billion by 2035, registering a CAGR of 6.3% during the forecast period (2026–2035). Two structural forces are anchoring this trajectory: the worldwide shift toward between-meal eating occasions — snacking now accounts for roughly 50% of all food consumption moments in mature economies [1] — and the parallel surge in online grocery penetration, which the USDA Economic Research Service projects will exceed 21% of total food retail by 2028 [2]. These catalysts are creating persistent tailwinds for both incumbent multinationals and agile regional producers competing in the Savory Snacks Market.

Product innovation has become the primary battleground. Legacy deep-fried platforms are steadily giving way to baked, air-popped, and protein-fortified formats as consumers respond to clean-label positioning and front-of-pack nutrition scoring systems such as Nutri-Score in Europe and the Health Star Rating in Australia [3]. Capital expenditure across the top ten manufacturers collectively surpassed USD 8.4 billion in 2024, with the bulk directed at flexible extrusion lines, AI-driven flavor profiling, and salt-reduction technologies. The Savory Snacks Market is also absorbing adjacent snack occasions previously held by confectionery and bakery categories.

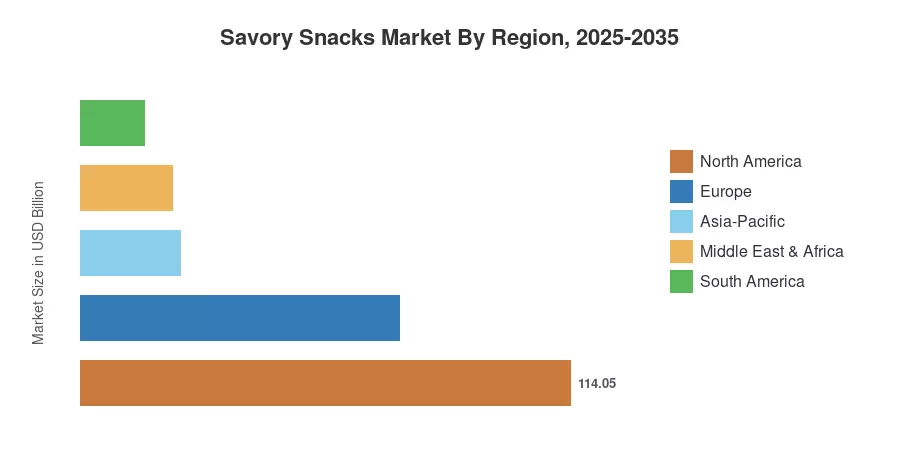

From a regional standpoint, North America commanded approximately 41.5% of the Savory Snacks Market in 2025, reinforced by the density of modern retail and deeply embedded snacking culture in the United States. Asia-Pacific represents the fastest-growing region, expanding at an estimated 8.5% CAGR through 2035, propelled by urbanization in India and Southeast Asia. Europe accounts for the second-largest share at roughly 27%, driven by premiumization and regulatory-led reformulation. The decade ahead will test whether health-forward innovation can sustain current growth rates as sodium-reduction mandates and input-cost pressures intensify across all geographies.

Key Report Takeaways

• By Product Type

- Chips and crisp-based snacks held approximately 41% of global Savory Snacks Market share in 2025, underscoring the dominance of the category's convenience and impulse-purchase appeal.

- Nuts, seeds, and trail mixes are forecast to expand at a 7.5% CAGR through 2035, reflecting consumer migration toward protein-rich snacking formats.

• By Flavor Profile & Category

- Flavored variants captured roughly 80% of the Savory Snacks Market in 2025, with regional and limited-edition launches accelerating rotation cycles.

- Free-form snacks are advancing at an 8.1% CAGR over 2026–2035, outpacing conventional packaged alternatives.

• By Region

- North America retained the largest regional revenue share in the Savory Snacks Market at approximately 41.5% in 2025.

- Asia-Pacific is the fastest-growing region with an 8.5% CAGR, fueled by disposable income growth and modern trade expansion across India, China, and ASEAN nations.

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulation of manufacturer revenue filings, trade-level shipment data from national customs authorities, and proprietary primary research spanning 1,200+ industry stakeholders across 38 countries. Historical figures (2021–2024) rely on audited annual reports and syndicated retail audit panels; forecast values (2026–2035) apply bottom-up demand modeling calibrated to macroeconomic indicators including GDP per capita, urbanization rate, and food CPI.