Shapewear Market Summary

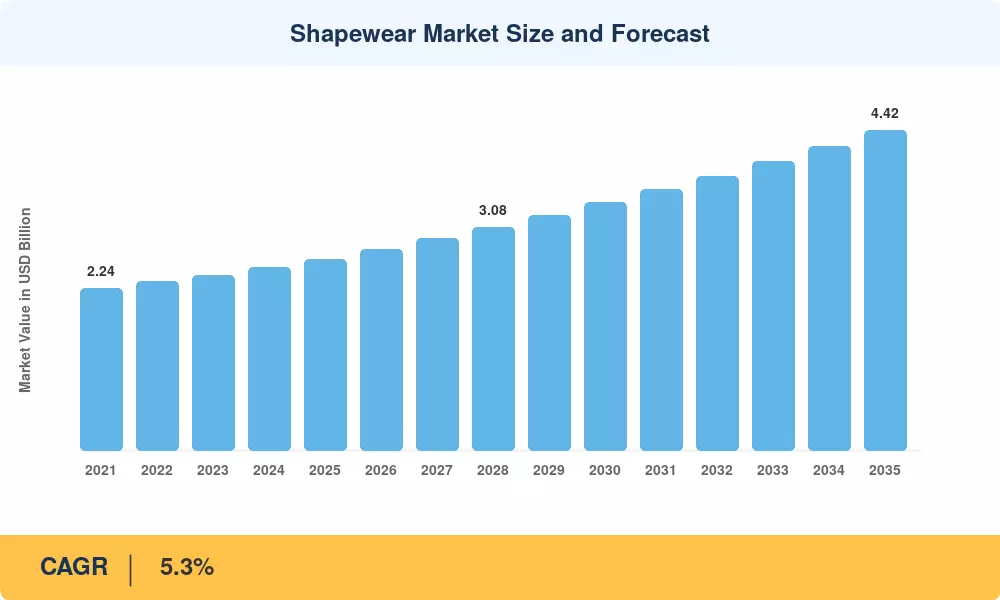

The Shapewear Market was valued at USD 2.64 Billion in 2025 and is projected to grow from USD 2.78 Billion in 2026 to USD 4.42 Billion by 2035, registering a CAGR of 5.3% during the forecast period (2026–2035). A combination of shifting consumer attitudes toward body confidence and rising disposable incomes across developing economies has accelerated demand. The global body positivity movement has reframed shapewear from a corrective undergarment into a confidence-boosting wardrobe essential, attracting both legacy intimate-wear brands and digitally native startups into the category [1].

Technological innovation is rewriting the product playbook for the Shapewear Market. Traditional rigid-panel construction is giving way to seamless knitting technologies, 3D body-mapping, and breathable micro-fiber composites that deliver targeted compression without sacrificing comfort. Brands invested an estimated USD 180 Million in fabric R&D between 2022 and 2024, and that pace of spending is expected to accelerate as smart textiles with moisture-wicking and thermoregulation properties enter pilot production [2]. Inclusive sizing initiatives — now covering up to 6XL at several leading brands — have opened addressable consumer pools that were historically underserved.

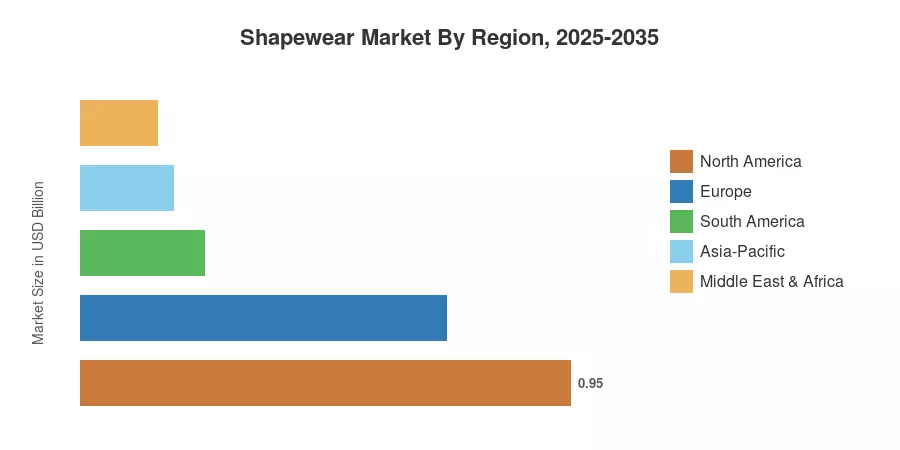

North America commands roughly 36% of global revenue, anchored by a mature e-commerce infrastructure and high brand awareness. Asia-Pacific is the fastest-growing region with a projected CAGR of 6.8%, propelled by urbanization and expanding middle-class spending in China, India, and ASEAN nations. Europe holds the second-largest share at approximately 27%, driven by premiumization trends and sustainability-conscious purchasing behavior. The Shapewear Market is poised to broaden its consumer base considerably as men's shapewear and athleisure-hybrid categories gain traction through 2035.

Key Report Takeaways

• By Type

- Full-Body Shapers account for the largest share of the Shapewear Market at roughly 33%, driven by demand for all-over silhouette control during formal and bridal occasions.

- High-Waist Shapers are forecast to grow at a CAGR of 5.9% through 2035 as everyday wear adoption increases.

- Shapewear Panties represent an estimated USD 0.66 Billion in 2025 value, benefiting from accessible price points and impulse purchasing patterns in the Shapewear Market.

• By Distribution Channel

- Online Retail Stores capture approximately 38% of the global Shapewear Market sales, fueled by influencer marketing and virtual try-on technology.

- Specialty Stores maintain a CAGR of 4.2% as personalized fitting experiences sustain brick-and-mortar relevance.

• By Region

- North America holds a 36% share of the Shapewear Market, with the United States contributing the majority of regional revenue.

- Asia-Pacific is expected to register a CAGR of 6.8%, making it the fastest-growing region in the Shapewear Market.

- Europe accounts for roughly 27% of global value, with Germany and the United Kingdom leading consumption.

Shapewear Market Size and Forecast (2021–2035)

Market Research Future's sizing model combines top-down revenue analysis from brand financial disclosures with bottom-up demand modeling using retail panel data, import-export statistics, and primary surveys across 22 countries. Historical figures (2021–2024) rely on audited company filings and trade databases; forecast figures (2026–2035) apply a calibrated constant-CAGR growth trajectory validated against macroeconomic indicators and consumer spending projections.