SLI Battery Market Summary

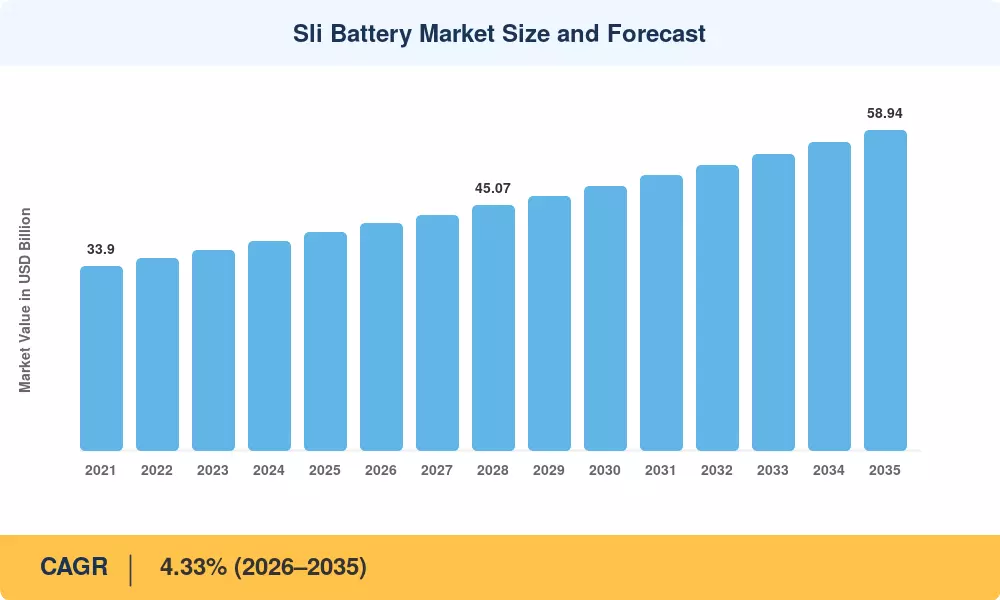

The SLI Battery Market reached an estimated USD 40.17 Billion in 2025, with forecast-period revenues projected to grow from USD 41.91 billion in 2026 to USD 58.94 billion by 2035, registering a CAGR of 4.33% across the forecast window. Rising vehicle production volumes in Asia and Latin America, coupled with tightening OEM SLI Battery specification standards under Euro 7 and EPA Tier 4 emission norms, are creating sustained demand for high-performance starting lighting ignition SLI Battery units across both passenger and commercial vehicle platforms[2].

A quiet but consequential technology shift is reshaping the SLI Battery Market. Legacy flooded lead-acid cells—still the workhorse in roughly half the global vehicle fleet—are steadily yielding ground to AGM EFB start-stop SLI Battery designs that tolerate deeper cycling and regenerative braking loads. European OEMs now specify AGM or EFB technology in more than 65% of new-vehicle builds, a figure that surpassed 50% only in 2021 [3]. Meanwhile, investments in lead recycling infrastructure exceeded USD 2.8 Billion globally in 2024, driven by circular-economy mandates in the EU Battery Regulation [4].

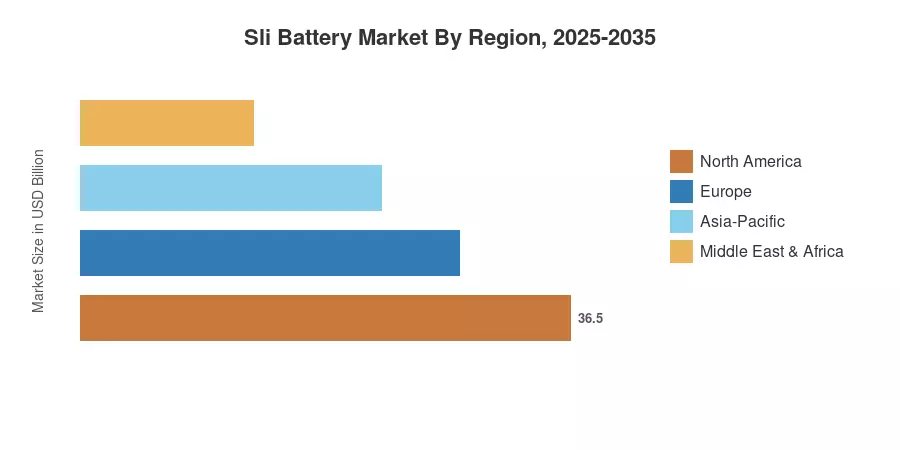

Asia-Pacific commands the largest share of the SLI Battery Market at approximately 46% of global revenue, propelled by China's and India's expanding vehicle parc and a robust SLI Battery aftermarket distribution network. The region also posts the fastest CAGR at an estimated 5.1%, outpacing Europe's 3.8% share-weighted growth. North America holds the second-largest regional share near 22%, anchored by replacement-cycle demand across the continent's aging light-vehicle fleet The decade ahead will hinge on how quickly car SLI lead acid replacement cycles shorten as start-stop electrification becomes standard.

Key Report Takeaways

• By Type

- VRLA batteries account for the fastest-growing type segment in the SLI Battery Market, posting a CAGR of approximately 5.2% through 2035, driven by AGM EFB start-stop SLI Battery adoption in micro-hybrid vehicles

- Flooded batteries retain the dominant revenue share, underpinned by cost advantages in price-sensitive aftermarket channels and deep SLI Battery cold cranking amps CCA compatibility across legacy platforms

- EFB batteries are projected to reach roughly USD 8.6 billion by 2035, reflecting OEM SLI Battery specification upgrades across European and Asian automakers

• By End-User

- The automotive segment captures more than 82% of the SLI Battery Market, spanning passenger cars, light commercial vehicles, and two-wheelers

- Non-automotive end users—including agriculture, marine, and standby power—register a combined CAGR of approximately 4.0% as industrial starting lighting ignition SLI Battery demand expands

• By Region

- Asia-Pacific leads the SLI Battery Market with an estimated 46% revenue share, reflecting China's dominant production base

- South America posts a CAGR near 4.7%, buoyed by Brazil's growing vehicle fleet and expanding SLI Battery aftermarket distribution networks

Market Size and Forecast (2021–2035)

MRFR's market sizing combines top-down revenue analysis of leading battery OEMs with bottom-up shipment tracking across flooded, VRLA, and EFB product lines. Historical figures (2021–2024) are triangulated against company filings, trade association data, and customs statistics. Forecast projections apply a calibrated CAGR of 4.33% to the 2026 base, stress-tested against IEA vehicle-stock models and regional production forecasts[5].