Small Arms Market Summary

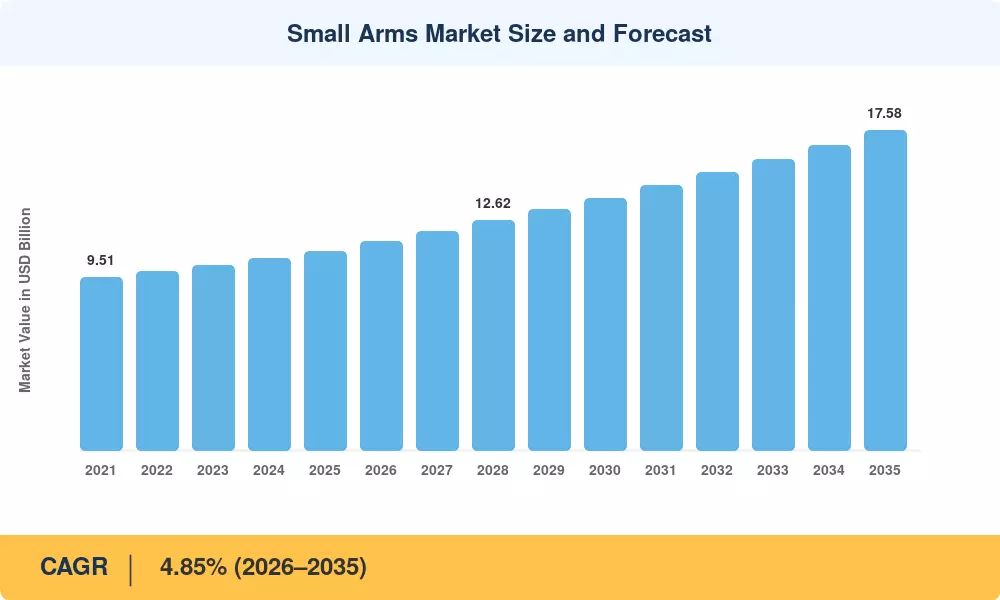

The Small Arms Market was valued at USD 10.96 billion in 2025 and is projected to reach USD 11.48 billion in 2026 before expanding to USD 17.58 billion by 2035, registering a CAGR of 4.85% during the 2026–2035 forecast window. Defense modernization budgets across NATO member states and Indo-Pacific allies have accelerated procurement cycles, while civilian firearm demand in North America continues to sustain baseline volume. The US Army's Next Generation Squad Weapon (NGSW) program — a 10-year initiative valued at up to USD 4.7 billion — exemplifies the institutional shift reshaping the Small Arms Market [2].

A technology transformation is redefining platform design across this sector. Legacy 5.56 mm infantry systems are giving way to advanced 6.8 mm modular weapon platforms engineered to defeat modern body armor at extended ranges. SIG Sauer's XM7 rifle and XM250 automatic rifle, selected under the NGSW contract, represent a generational leap in lethality and fire-control integration that defense ministries worldwide are evaluating for adoption [3]. Smart optics, suppressor-ready barrels, and digitally networked fire-control units are rapidly becoming standard requirements rather than optional upgrades.

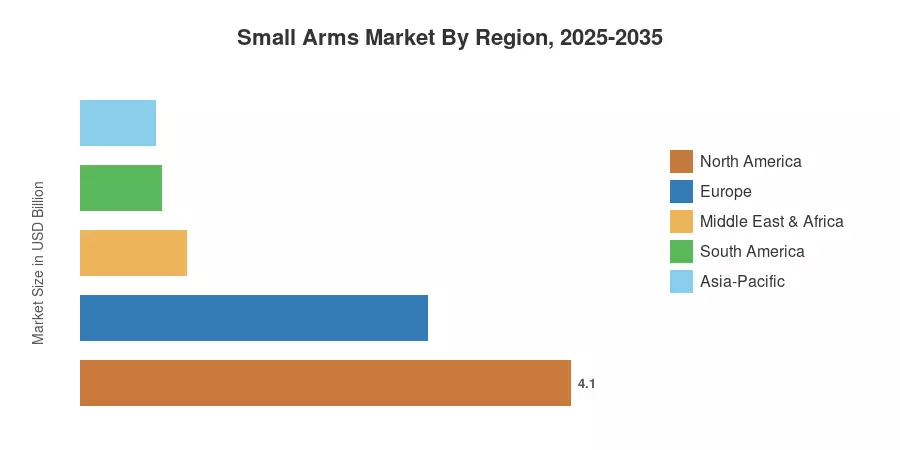

North America commands approximately 37.4% of the global Small Arms Market, driven by the world's largest civilian ownership base and sustained Department of Defense procurement. Asia-Pacific is the fastest-growing region at a projected CAGR of 5.78%, propelled by defense corridor investments in India, the Philippines, and South Korea [4]. Europe holds the second-largest regional share at roughly 26.5%, anchored by Franco-German joint weapons programs and post-2022 rearmament budgets across Eastern European NATO members. The Small Arms Market is poised for a decade of sustained expansion as geopolitical tensions and domestic security priorities converge.

Key Report Takeaways

• By Type

- Pistols accounted for 35.2% of the Small Arms Market share in 2025, reflecting broad adoption across law enforcement and civilian concealed-carry segments.

- Assault rifles are projected to grow at a CAGR of 5.48% through 2035, driven by infantry modernization programs and next-generation caliber migration.

• By Caliber

- 9 mm rounds represented approximately USD 2.82 billion in Small Arms Market revenue in 2025, reinforcing the caliber's dominance in sidearm and submachine-gun platforms.

- 6.8 mm rounds are expected to register the highest caliber-segment CAGR of 8.46% through 2035, reflecting the NGSW transition.

• By Operation

- Semi-automatic systems held 47.2% of the Small Arms Market in 2025, preferred across both civilian sporting and military sidearm applications.

- Fully automatic platforms are advancing at a CAGR of 5.06% as military forces procure next-generation squad automatic weapons.

• By End User

- Civil and law enforcement customers captured 53.9% of the Small Arms Market in 2025.

- The military segment is anticipated to achieve the highest end-user CAGR of 5.36% through 2035.

• By Region

- North America maintained a 37.4% share of the Small Arms Market in 2025.

- Asia-Pacific is forecasted to grow at a CAGR of 5.78% through 2035, led by India's defense manufacturing corridor initiative.

Market Size and Forecast (2021–2035)

Market Research Future's forecasts integrate primary interviews with defense procurement officials, civilian retail channel surveys, and customs-trade databases from 42 countries. Historical figures (2021–2024) derive from verified shipment data and government defense-expenditure disclosures, while forecast projections (2026–2035) apply scenario-weighted regression models calibrated against macroeconomic indicators and defense-budget trajectories.

.webp?v=1783951712)