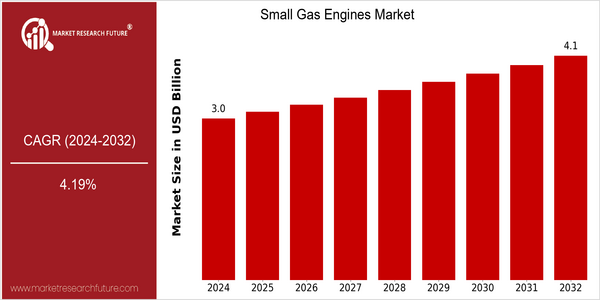

Small Gas Engines Size

Market Size Snapshot

| Year | Value |

|---|---|

| 2024 | USD 2.97 Billion |

| 2032 | USD 4.12 Billion |

| CAGR (2024-2032) | 4.19 % |

Note – Market size depicts the revenue generated over the financial year

Gasoline engines are a growth market, and the small engines market is expected to grow from $3.97 billion in 2024 to $ 4.12 billion in 2032. The average annual growth rate (CAGR) for this period is 4.19%. The growing demand for small engines for various applications such as lawn mowers, construction equipment and portable generators is the main driving force for this market growth. Industry X is increasingly demanding in terms of fuel efficiency and reliability, and advanced technology is becoming the main force driving the market. There are many reasons for the optimistic outlook of the small gasoline engine market. There is a great demand for engines in the construction machinery industry, and the demand for small engines in the construction machinery industry is expected to grow steadily. The engine is the core of the machine, and the core technology is constantly improving, such as the development of cleaner and more efficient combustion, which can improve the performance of the machine and reduce the exhaust gas. The demand for small engines will also increase due to the popularity of lawn mowers and other lawn mowers. Honda Motor Co., Ltd., Briggs & Stratton Co., and Kohler Co., etc., have been investing in research and development to launch new products and improve their existing products. The competition is getting stronger and stronger. , and the cooperation between companies is also increasing. , The trend of the market is also changing.

Regional Market Size

Regional Deep Dive

The world of the small gas engine is one of the most complex in the world. The North American market is bolstered by the growing demand for outdoor power equipment and the growing trend towards greener solutions. Europe is experiencing a change in its regulations that require engines to be more and more efficient. The Asia-Pacific region is experiencing rapid urbanization and industrialization, which is boosting the demand for small engines in a variety of applications. The Middle East and Africa are growing because of their growing need for infrastructure. The Latin American region is influenced by its agricultural needs and its manufacturing capabilities. Each region presents unique opportunities and challenges that influence the global small gas engine market.

Europe

- The European Union's Green Deal aims to reduce greenhouse gas emissions, leading to increased investments in low-emission small gas engines, with companies like Stihl adapting their products to comply with new regulations.

- Innovations in fuel efficiency and noise reduction technologies are being prioritized, with firms such as Husqvarna launching new models that cater to both regulatory demands and consumer expectations for quieter operation.

Asia Pacific

- Rapid urbanization in countries like India and China is driving demand for small gas engines in construction and agricultural sectors, with local manufacturers such as Mahindra & Mahindra expanding their offerings.

- Government initiatives promoting mechanization in agriculture are leading to increased adoption of small gas engines, with programs aimed at providing subsidies for farmers to purchase modern equipment.

Latin America

- The agricultural sector in Brazil is a significant driver for small gas engines, with local companies like Tatu Marchesan innovating to meet the specific needs of farmers.

- Government programs aimed at enhancing rural productivity are encouraging the adoption of small gas engines, with initiatives providing financial assistance for purchasing equipment.

North America

- The U.S. Environmental Protection Agency (EPA) has introduced stricter emissions standards for small engines, pushing manufacturers like Honda and Briggs & Stratton to innovate towards cleaner technologies.

- The rise of electric alternatives is prompting traditional gas engine manufacturers to diversify their product lines, with companies like Generac investing in hybrid solutions to meet changing consumer preferences.

Middle East And Africa

- Infrastructure projects in the Gulf Cooperation Council (GCC) countries are boosting demand for small gas engines, with companies like Caterpillar supplying engines for construction machinery.

- The region's growing focus on renewable energy is influencing the development of hybrid small gas engines, as seen in initiatives by local firms to integrate solar power with traditional gas engines.

Did You Know?

“Did you know that small gas engines are used in a variety of applications, from lawn mowers to portable generators, and account for a significant portion of the outdoor power equipment market?” — Outdoor Power Equipment Institute (OPEI)

Segmental Market Size

The small gas engine market is currently growing steadily. The main reason for this is the increasing demand for portable power in various industries. Also, the popularity of outdoor activities, which require the availability of lawnmowers and power generators, as well as the increasingly stricter regulations on emissions, are important growth drivers. Furthermore, the efficiency and emissions of small engines have improved, which increases the attractiveness of the products in a competitive environment. At present, the market is in a mature phase of development. The main innovators are Honda and Briggs & Stratton. The leading manufacturers are introducing advanced technology to meet the stricter emissions regulations, especially in North America and Europe. The main applications are in the gardening, construction and agricultural industries, where small engines are an essential part of the equipment. In the future, the market will be influenced by the development of sustainable energy and the electrification of various industries, which will lead to the development of hybrid and alternative fuel solutions to meet the changing needs of consumers.

Future Outlook

The small gas engine market is set to experience a substantial growth between 2024 and 2032, when the market value is projected to increase from $2.97 billion to $4.12 billion at a compound annual growth rate (CAGR) of 4.19%. This growth will be driven by the increasing demand for small gas engines in various industries, such as agriculture, construction, and recreation, where they are used in lawn mowers, generators, and power tools. In addition, the rising urbanization and the growing need for efficient and portable power will further drive the penetration of small gas engines. The growth will be significant in both developed and emerging economies. The market will be influenced by technological developments, such as the increasing efficiency and the decreasing emissions of small gas engines. The integration of digital controls and hybrid systems will increase the performance of small gas engines while complying with the stringent regulations. Government initiatives to promote cleaner energy solutions and to incentivize the use of low-emission engines will also play a key role in the market’s growth. The shift towards electric alternatives will also affect the competition in the market, which will force manufacturers to adapt their products to meet the changing preferences of consumers. In the end, the small gas engine market will grow at a substantial rate, influenced by technological developments, government support, and rising demand.

Leave a Comment