Smart Contact Lenses Market Summary

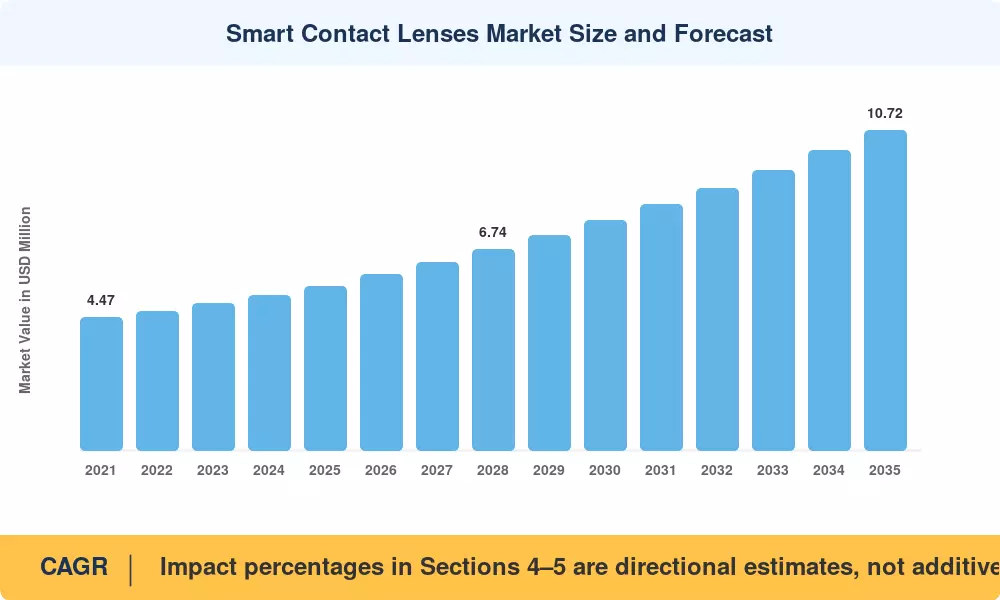

The Global Smart Contact Lenses Market size was valued at USD 5.50 Million in 2025, and the market is projected to grow from USD 5.91 Million in 2026 to USD 10.72 Million by 2035, registering a CAGR of 6.85% during the forecast period 2026–2035, this sector benefits from accelerating regulatory momentum—particularly the US FDA's De Novo classification pathway that cleared two IOP-monitoring devices in 2024 [1]. Government health agencies across OECD countries have earmarked over USD 420 Million in digital therapeutics funding through 2030, channeling capital into tear-based diagnostics and connected ocular platforms [2].

A generational technology shift is underway. Legacy episodic clinic visits for glaucoma screening and glucose tracking are giving way to continuous, lens-embedded monitoring that feeds data directly into electronic health record systems. Silicon-hydrogel nanocomposite substrates have slashed manufacturing reject rates by nearly 30% since 2022, while sub-microwatt power-harvesting circuits now sustain 24-hour sensing cycles [3]. Venture capital flowing into ophthalmic wearables surpassed USD 310 Million cumulatively through 2024, signaling strong private-sector conviction in the Smart Contact Lenses Market trajectory [4].

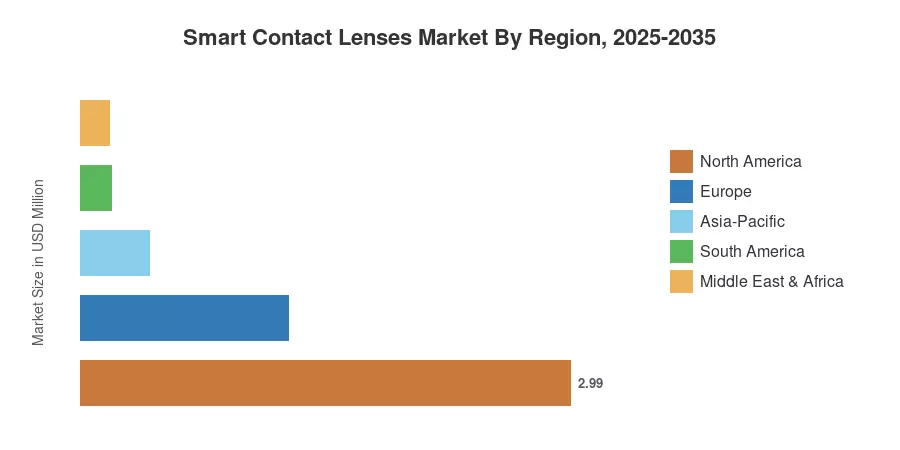

North America commands a 54.4% revenue share, underpinned by robust insurance pilot programs and dense ophthalmology networks. Asia-Pacific is the fastest-growing region, posting an anticipated CAGR of 7.61% through 2035, propelled by South Korea's CDMO infrastructure and Japan's aging-population healthcare mandates. Europe holds the second-largest position, contributing approximately 23.1% of global revenue through advanced clinical trial ecosystems. The Smart Contact Lenses Market is poised for sustained expansion as reimbursement frameworks mature and 5G connectivity lowers data-latency barriers across emerging economies.

Key Report Takeaways

• By Application

- Ocular Monitoring & Glaucoma Treatment lenses captured 54.5% of Smart Contact Lenses Market revenue in 2025, driven by chronic disease management mandates.

- The Vision Impairment segment is expanding as corrective-lens platforms integrate real-time refractive adjustment capabilities.

• By End User

- Hospitals & Ophthalmology Clinics accounted for 42.7% of global demand in 2025, reflecting institutional procurement cycles for connected diagnostic devices.

- Home-care/Self-monitoring Consumers represent the fastest-growing end-user category at 8.52% CAGR through 2035, as point-of-care platforms shift toward patient-managed monitoring.

• By Region

- North America maintained a 54.4% share of the Smart Contact Lenses Market in 2025, supported by early FDA clearances and private-payer pilot programs.

- Asia-Pacific is projected to grow at a 7.61% CAGR through 2035, with South Korea and Japan leading product iteration.

Market Size and Forecast (2021–2035)

Market Research Future constructed this forecast using a triangulated methodology combining bottom-up revenue modeling from device-level shipments, top-down validation against national healthcare expenditure databases, and primary interviews with 85+ ophthalmic device executives and clinicians across 14 countries [5].

.webp?v=1785323599)