Smart Inhalers Market Summary

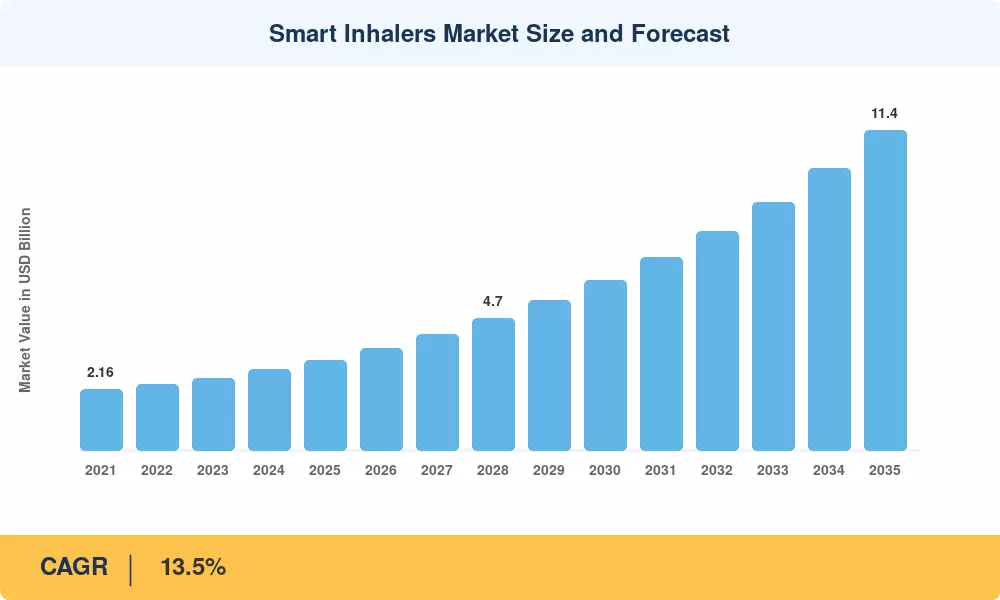

The Global Smart Inhalers Market size was valued at USD 3.21 Billion in 2025, and the market is projected to grow from USD 3.64 Billion in 2026 to USD 11.40 Billion by 2035, registering a CAGR of 13.5% during the forecast period 2026–2035. This trajectory reflects a fundamental shift in chronic respiratory disease management, where payers and regulators alike are rewarding measurable adherence outcomes over simple prescription volume. The FDA's 2024 guidance on connected drug-delivery device validation compressed approval timelines by an estimated 30%, unlocking a wave of new product filings that will sustain double-digit growth well into the next decade [1].

Legacy pressurized metered-dose inhalers — devices essentially unchanged since the 1950s — are giving way to sensor-equipped platforms that capture inhalation technique, dosing frequency, and environmental triggers in real time. AstraZeneca's next-generation Breztri program, designed around near-zero global-warming-potential propellants, exemplifies how sustainability mandates and digital health are converging within a single device architecture. Pharmaceutical companies invested an estimated USD 1.8 Billion in digital inhaler R&D during 2023–2024, a figure expected to climb as reimbursement frameworks increasingly tie payment to documented patient outcomes [2].

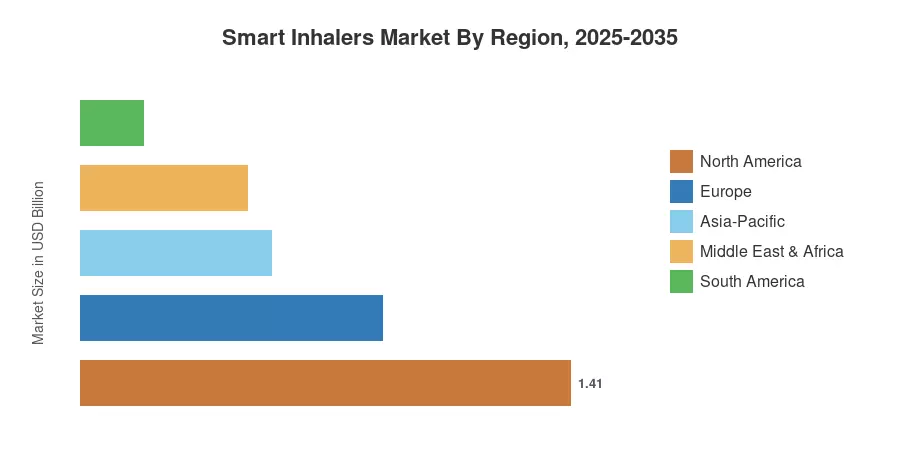

North America commands roughly 43.9% of the Smart Inhalers Market, anchored by robust insurance incentives for connected devices and high smartphone penetration among COPD patients. Asia-Pacific stands as the fastest-growing region at a projected 17.2% CAGR through 2035, driven by India's and China's national respiratory health programs. Europe holds the second-largest share, supported by the EU MDR classification pathway that streamlines digital health device approvals. The decade ahead will test whether emerging markets can close the adoption gap before exacerbation costs overwhelm public healthcare systems.

Key Report Takeaways

• By Product Type

- Metered Dose Inhalers accounted for 68.7% of the Smart Inhalers Market in 2025, reflecting decades of prescriber familiarity and an established supply chain for propellant-based delivery systems.

- Dry Powder Inhalers are forecast to expand at a 14.5% CAGR through 2035, as breath-actuated designs eliminate coordination challenges that reduce adherence among elderly COPD populations.

• By Indication

- COPD represented 54.3% of Smart Inhalers Market revenue in 2025, given the condition's higher per-patient device utilization rates and reimbursement premiums.

- Asthma is projected to grow at a 13.9% CAGR over 2026–2035, fueled by pediatric digital health initiatives and school-based monitoring programs across North America and Europe.

• By Distribution Channel

- Hospital pharmacies led distribution with a 46.4% share of the Smart Inhalers Market in 2025, benefiting from integrated electronic health record connectivity at the point of discharge.

- Online pharmacies are positioned to post a 14.2% CAGR through 2035, as direct-to-patient subscription models gain traction among younger demographics.

• By Region

- North America captured 43.9% of the Smart Inhalers Market in 2025, supported by Medicare Advantage value-based care contracts that incentivize connected device adoption.

- Asia-Pacific will register the fastest CAGR of 17.2%, with India's Ayushman Bharat Digital Mission and China's chronic disease management platforms accelerating uptake.

Smart Inhalers Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up revenue estimation from device manufacturers, top-down demand modeling from respiratory disease epidemiology databases, and cross-validation against insurance claims data and regulatory filing records. Historical figures draw on audited company reports and WHO respiratory burden statistics, while forecast projections apply a constant CAGR reflective of structural demand drivers identified in Sections 4 and 6.

.webp?v=1782478111)