Smart Lock Market Summary

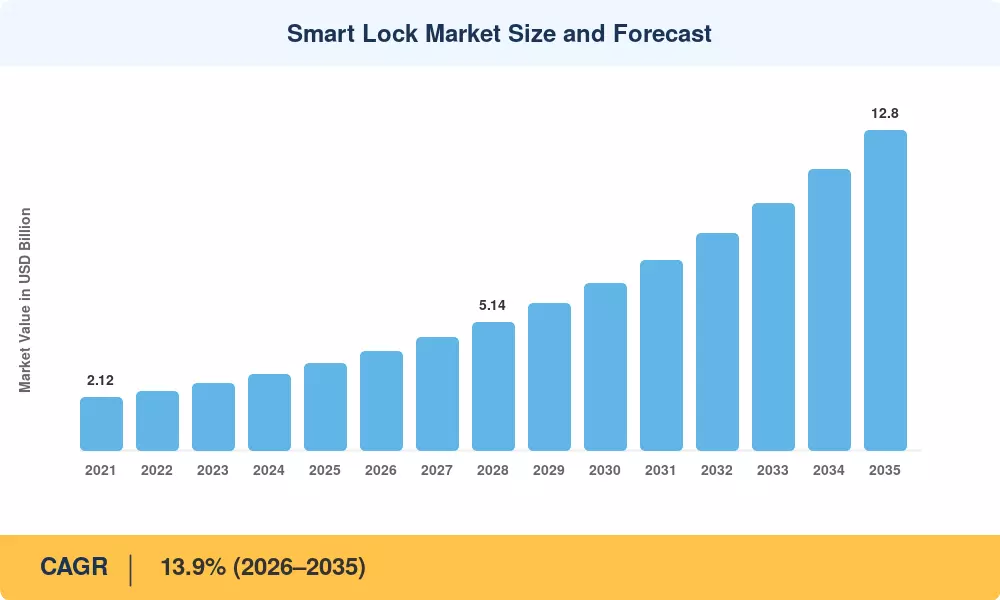

The Smart Lock Market reached USD 3.48 billion in 2025 and is projected to grow from USD 3.96 billion in 2026 to USD 12.80 billion by 2035, registering a CAGR of 13.9% during the forecast period (2026–2035). This expansion is rooted in accelerating smart home platform adoption, tightening urban safety mandates, and the maturation of interoperability standards such as Matter and Thread that are collapsing long-standing integration barriers across device ecosystems [1].

There’s a fundamental technology transition underway to linked, credential-free entry systems that are replacing classic pin-tumbler and mechanical deadbolts. Lower prices for capacitive fingerprint modules (roughly 38% since 2021 per industry component trackers [2]) have driven biometric authentication into the mid-range price points, and the Connectivity Standards Alliance’s release of Matter 1.2 has brought over 40 smart lock SKUs into a unified control layer [3]. Insurance providers in the U.S. and U.K. currently provide 5–15% premium savings for certified smart lock installations, providing a measurable total-cost-of-ownership incentive for home upgrades [4].

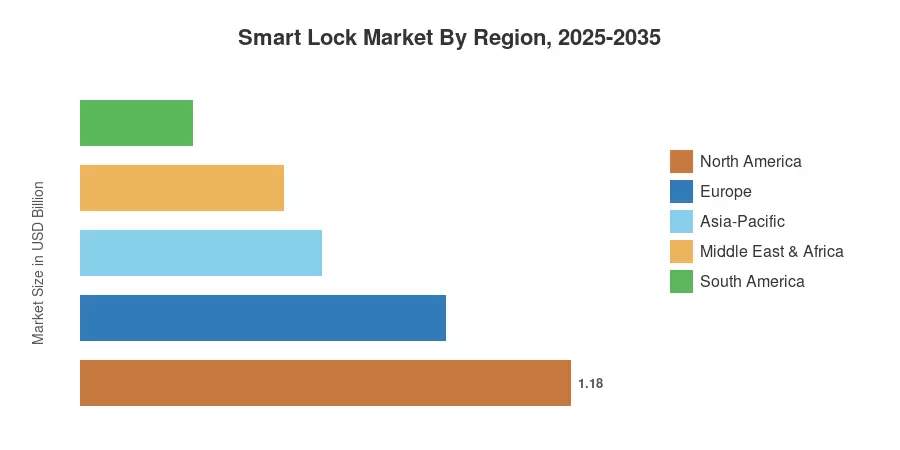

North America held ~33.9% of the Smart Lock Market revenue share in 2025, supported by mature e-commerce distribution and short-term rental usage driven by Airbnb. The Asia-Pacific area is the fastest growing, expected to grow at a 16.7% CAGR till 2035, driven by large-scale urbanization in India, China and ASEAN countries. Europe holds the second-highest market at about 25.3%, with commercial installations being driven by EN 15684 regulatory harmonization and sustainability-linked building norms. The Smart Lock Market is at the junction of physical security, digital identification and property technology – a convergence that will define access control for the next decade.

Key Report Takeaways

• By Lock Type

- Deadbolt smart locks captured approximately 48.2% of Smart Lock Market revenue in 2025, driven by retrofit compatibility with existing residential door preparations.

- Lever handle systems are forecast to advance at a 16.3% CAGR through 2035, gaining traction in commercial office and hospitality settings.

• By Authentication

- Keypad-based authentication accounted for roughly 45.0% of Smart Lock Market share in 2025, favored for guest-code flexibility in rental properties.

• By Geography

- North America led the Smart Lock Market with 33.9% share in 2025.

- Asia-Pacific is projected to register the highest regional CAGR of 16.7% through 2035.

Smart Lock Market Size and Forecast (2021–2035)

Market Research Future (MRFR) projections are based on primary interviews with lock OEMs, component suppliers and channel distributors and secondary data from trade groups, patent filings and regulatory databases. Historical values are based on reported shipment revenues, adjusted for ASP erosion and currency effects. Forecast values are based on a compound annual growth model calibrated to macro factors such as house starts, commercial development permits and IoT device penetration rates.