Smart Workplace Market Summary

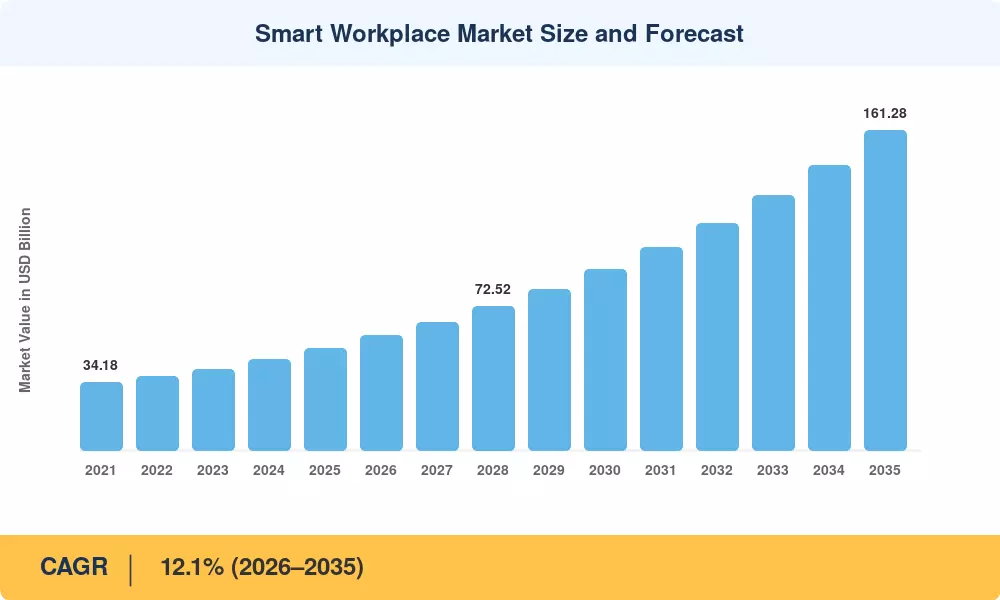

The Smart Workplace Market reached an estimated USD 51.48 billion in 2025, poised to climb from USD 57.71 billion in 2026 to USD 161.28 billion by 2035 at a compound annual growth rate (CAGR) of 12.1% during the 2026–2035 forecast window. Two forces are accelerating adoption at a pace few technology categories match: first, updated energy-performance mandates like ASHRAE Standard 90.1-2022 and local building-performance laws in cities such as New York (Local Law 97) and London (MEES regulations) are pushing landlords toward intelligent HVAC, lighting, and space-utilization platforms [1][2]. Second, the structural shift to hybrid work has turned real-time occupancy data from a convenience into an operational necessity for facility managers juggling fluctuating headcounts.

The cloud-connected sensor networks, AI-powered climate control, and integrated desk-reservation platforms are replacing the traditional building-management systems built for static 9-to-5 occupancy. In fact, corporate real-estate teams claim energy savings of 25-35% after adopting intelligent building systems; productivity metrics measured by anonymized workplace analytics imply production improvements of over 40% in pilot projects [3][4]. In 2024, commercial smart building retrofits attracted investments of over USD 28 billion globally, indicating that even the existing building stock is being included in the Smart Workplace Market fold [5].

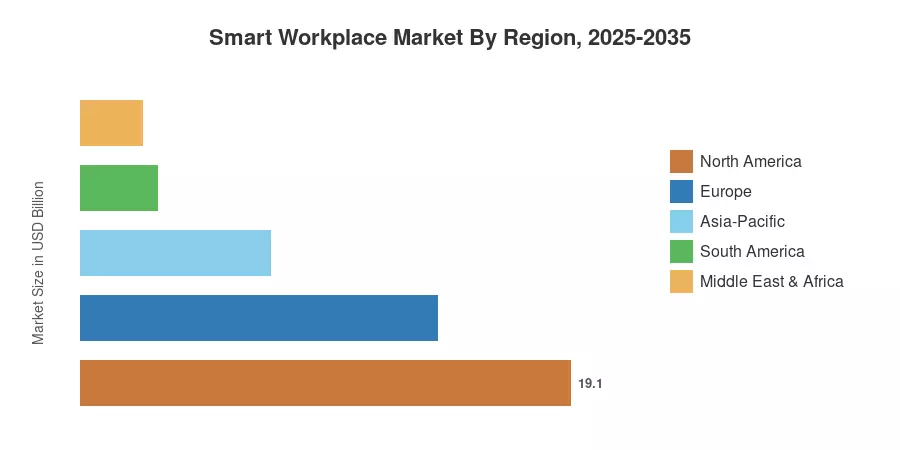

North America represented a substantial share of the Smart Workplace Market in 2024, around 37.1%, due to early enterprise adoption in the United States and Canada. Asia-Pacific is the fastest-growing area and is expected to have a CAGR of 14.4% through 2035, as increasing urbanization in China, India and ASEAN countries drives new commercial buildings. The second highest share was held by Europe with roughly 27.0% because to the need to meet EU taxonomy-aligned standards for restoration. With maturing AI capabilities and falling sensor prices, the Smart Workplace Market is approaching a decade of compounding momentum.

Key Report Takeaways

• By Component

- Smart lighting systems accounted for approximately 30.6% of Smart Workplace Market revenue in 2024, reflecting strong adoption of tunable-white and human-centric lighting across Class A office buildings.

- Sensors and edge devices are forecast to expand at a 14.7% CAGR from 2026 to 2035, driven by falling hardware costs and growing demand for real-time environmental monitoring.

• By Solution Type

- Hardware represented roughly 49.3% of the Smart Workplace Market in 2024, encompassing connected luminaires, HVAC actuators, occupancy sensors, and access-control endpoints.

- Cloud and SaaS solutions are projected to grow at a 14.8% CAGR through 2035, outpacing on-premises software as multi-tenant analytics platforms gain traction.

• By Geography

- North America commanded a 37.1% share of the Smart Workplace Market in 2024, with the United States alone contributing over two-thirds of regional revenue.

- Asia-Pacific is set to record the highest regional CAGR of 14.4% during the forecast period, propelled by smart-city initiatives across China, India, and South Korea.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a bottom-up revenue model, which sums vendor shipments, software license and managed-service contract values in commercial working contexts. Historical estimates (2021-2024) are based on available financial disclosures and industry association data; the prediction employs a calibrated 12.1% CAGR for 2026-2035, tested against macroeconomic indices and technology adoption curves.