Sodium Chloride Market Summary

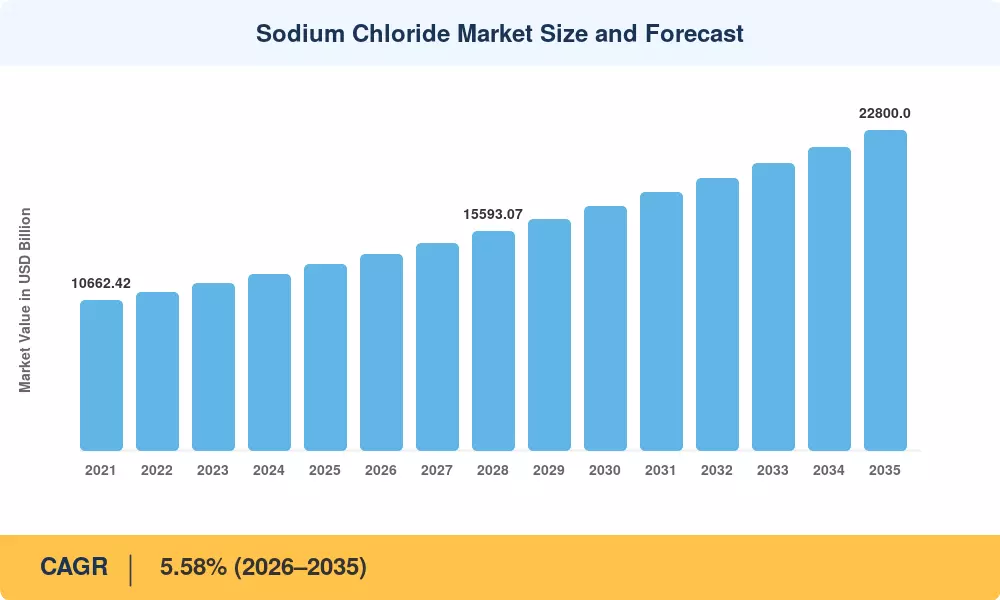

The Sodium Chloride Market reached an estimated USD 13,250 Million in 2025 and is projected to grow from USD 13,990 Million in 2026 to approximately USD 22,800 Million by 2035, registering a CAGR of 5.58% across the forecast window. Two catalysts stand behind this acceleration: pharmaceutical-grade supply constraints flagged by the U.S. FDA through 2024 continue to strain dialysis and intravenous therapy supply chains, while sodium-ion battery cathode programs — particularly in China — are scaling rapidly, pulling high-purity industrial salt into energy-storage value chains that barely existed five years ago [1].

Legacy extraction and refining methods are giving way to precision-graded processing. Vacuum evaporation facilities now target the sub-10-ppm impurity thresholds demanded by pharmaceutical-grade salt buyers and chlor-alkali electrolysis cells. Concentrated solar-power installations across Morocco, South Africa, and the Gulf states have adopted molten-salt thermal storage, creating a demand channel for chemical processing salt that fossil-fired plants never required [2]. Global investment in these next-generation salt applications exceeded USD 2.8 billion in 2024, according to BloombergNEF estimates [3].

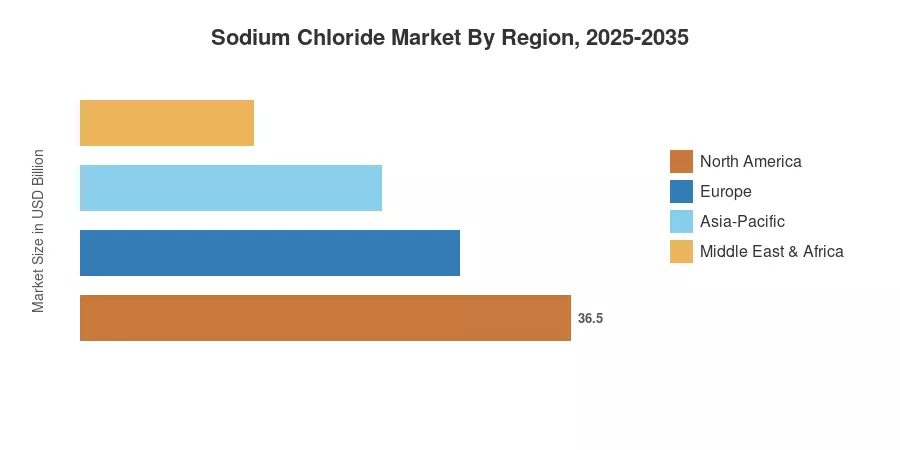

Asia-Pacific commands roughly 49.8% of the Sodium Chloride Market by value, driven by China's integrated chlor-alkali complexes and India's expanding food processing salt output. The region also registers the fastest CAGR at 6.92%. North America follows as the second-largest region, supported by robust deicing salt consumption and water softening salt mandates in hard-water municipalities. Europe rounds out the top three, where tightening EU chemical-safety standards are pushing producers toward higher-purity grades and reshaping the competitive mix heading into the next decade

Key Report Takeaways

• By Grade

- Rock salt accounted for 38.8% of the Sodium Chloride Market in 2025, reflecting its dominance in deicing salt and bulk chemical feedstock applications

- Vacuum salt is forecast to expand at a 7.56% CAGR through 2035, fueled by rising demand for pharmaceutical grade salt and high-purity industrial salt

- Solar salt generated approximately USD 4,320 Million in 2025, anchored by evaporation operations in Australia and India

• By Application

- Chemical production represented 35.4% of the Sodium Chloride Market size in 2025, with chlor-alkali plants consuming the largest single volume

- Pharmaceuticals are poised to expand at an 8.44% CAGR during 2026–2035, the fastest of any application segment

- The Sodium Chloride Market for food processing reached approximately USD 2,220 Million in 2025 as packaged-food output scaled in emerging cities

• By Region

- Asia-Pacific captured 49.8% of the Sodium Chloride Market in 2025 and is projected to outpace all other regions through 2035

- North America contributed a 5.12% CAGR, underpinned by water softening salt mandates and highway deicing salt budgets

- Europe accounted for 17.6% of global value, with Germany and France leading adoption of industrial mineral salts compliant with REACH updates

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates bottom-up production volumes from salt mining products operators, top-down trade-flow data from UN Comtrade, and proprietary pricing models calibrated to regional contract benchmarks. Historical figures (2021–2024) rely on audited filings and customs records; forecast values (2026–2035) apply the calibrated 5.58% CAGR against the 2025 base year.