Sorbitol Market Summary

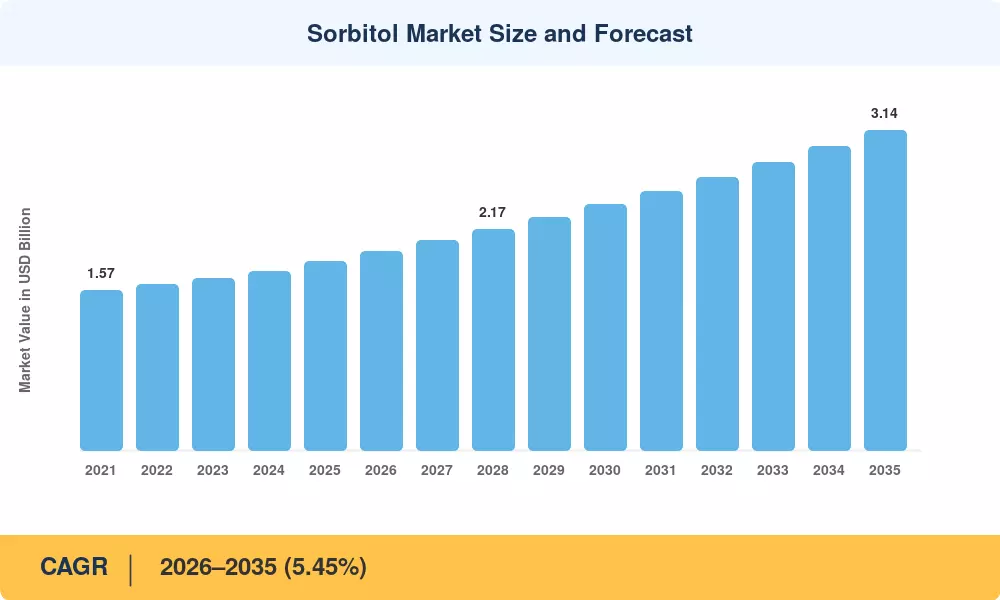

The Sorbitol Market reached USD 1.85 billion in 2025 and is projected to grow from USD 1.95 billion in 2026 to USD 3.14 billion by 2035, registering a CAGR of 5.45% during the forecast period. Two forces are accelerating this trajectory: tightening government sugar-reduction mandates across the EU, ASEAN, and Latin America, and a simultaneous wave of capital flowing into clean-label food ingredient platforms. The WHO's updated free-sugar guidelines, adopted by over 40 countries since 2023, have pushed reformulation budgets higher and made polyol-based sweetening a boardroom priority rather than an R&D footnote [1].

Sorbitol's versatility distinguishes it from single-purpose sweeteners. Legacy sucrose and high-fructose corn syrup are steadily giving ground to sugar alcohols that double as humectants, texturizers, and excipients. Global investment in continuous-crystallization sorbitol plants exceeded USD 420 million between 2022 and 2024, with major capacity additions in China, India, and Brazil targeting both food-grade and pharma-grade output [2]. Regulatory tailwinds include the European Commission's Farm to Fork strategy, which incentivizes low-glycemic ingredients, and India's FSSAI labeling reforms that reward reduced-sugar claims on front-of-pack displays [3].

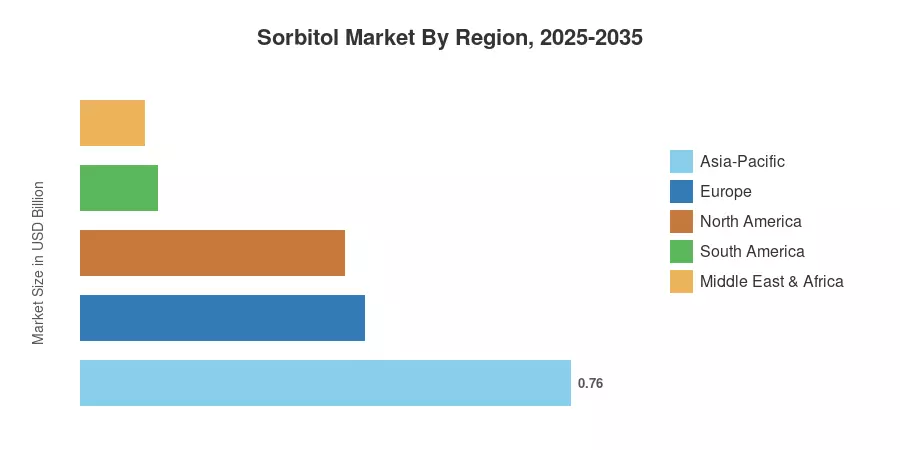

Asia-Pacific commands roughly 41% of the Sorbitol Market, anchored by China's massive corn-processing infrastructure and India's fast-growing confectionery sector. South America is the fastest-growing region at a 6.65% CAGR, driven by Brazil's expanding biorefinery ecosystem and rising domestic demand for sugar-free products. Europe holds the second-largest share at approximately 24%, buoyed by stringent EU health labeling and a mature personal-care industry. As functional-food innovation accelerates across emerging economies, the Sorbitol Market is poised to deliver steady mid-single-digit growth through 2035.

Key Report Takeaways

• By Product Type

- Liquid sorbitol accounted for roughly 70% of the Sorbitol Market in 2025, supported by cost-efficient bulk logistics and direct-pipe delivery to confectionery and oral-care manufacturers.

- Powder/crystal sorbitol is on track to register a CAGR of 6.95% through 2035, as pharmaceutical tableting and premium cosmetics demand higher-purity dry forms.

• By Application

- Food and beverage captured approximately 47% of the Sorbitol Market share in 2025, reflecting broad adoption in sugar-free confectionery, baked goods, and frozen desserts.

- Dietary supplements are projected to expand at a 7.25% CAGR through 2035, fueled by chewable-vitamin and nutraceutical gummy reformulation.

• By Region

- Asia-Pacific held the dominant position in the Sorbitol Market with a 41% share in 2025.

- South America is the fastest-growing region at a projected 6.65% CAGR, led by Brazilian sugarcane-to-sorbitol biorefineries.

- North America contributed approximately USD 0.41 billion in 2025, driven by diabetic-management and oral-care applications.

Sorbitol Market Size and Forecast (2021–2035)

Market Research Future's sizing model combines bottom-up production-capacity audits, trade-flow analysis from UN Comtrade and national customs databases, and top-down demand modeling validated against annual reports of the ten largest sorbitol producers. Historical figures (2021–2024) are reconciled actuals; the base year (2025) reflects preliminary shipment data; forecast years (2026–2035) apply a calibrated CAGR with micro-adjustments for feedstock cost cycles and regulatory phase-ins.