Sports Nutrition Market Summary

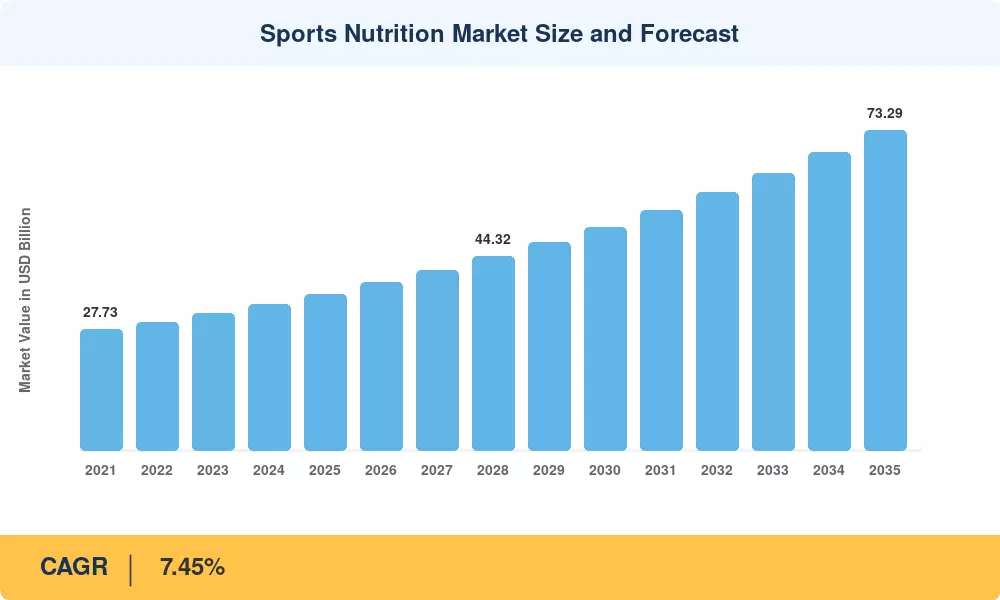

The Sports Nutrition Market stood at USD 35.67 Billion in 2025 and is projected to reach USD 38.39 Billion in 2026 before climbing to USD 73.29 Billion by 2035, expanding at a 7.45% CAGR during the 2026–2035 forecast period. Rising health consciousness worldwide, combined with government-backed physical fitness initiatives—such as the WHO Global Action Plan on Physical Activity targeting a 15% reduction in inactivity by 2030—has created a durable demand foundation [1]. Gym membership penetration across developed economies surpassed 22% in 2024, channeling millions of new consumers toward performance-focused nutrition products.

Product innovation is reshaping the Sports Nutrition Market from the inside out. Legacy formulations built around basic protein concentrates are giving way to precision-engineered functional blends featuring adaptogens, nootropics, and microbiome-supporting ingredients. Private-label investment in clean-label sports nutrition exceeded USD 2.4 billion globally in 2024, reflecting retailer confidence in sustained consumer demand. The shift toward plant-derived and allergen-free formulations is accelerating faster than any prior product cycle in this category.

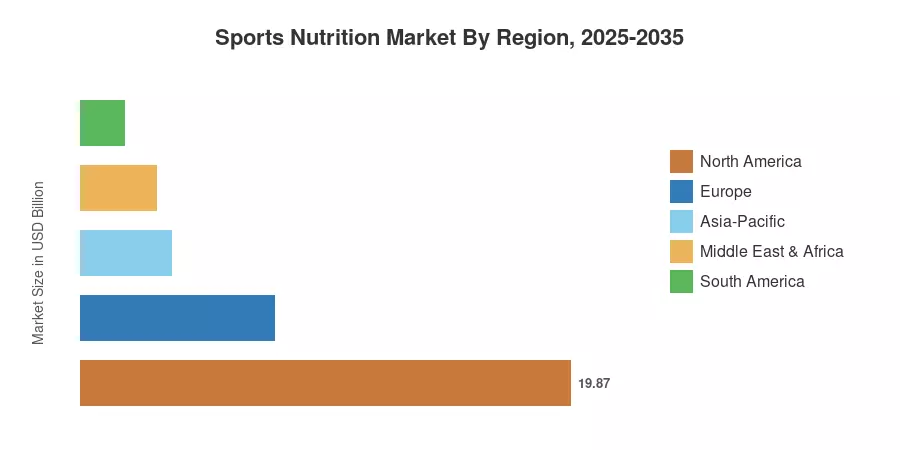

North America commands roughly 55.7% of global Sports Nutrition Market revenue, underpinned by deep retail penetration and a mature supplement culture. Asia-Pacific is the fastest-growing region at a projected 10.3% CAGR through 2035, fueled by urbanization and expanding middle-class fitness participation in China, India, and Southeast Asia. Europe holds the second-largest share at approximately 22%, with demand driven by regulatory harmonization under the EU Novel Food framework. The decade ahead points toward continued geographic diversification and product sophistication across the Sports Nutrition Market.

Key Report Takeaways

• By Product Type

- Sports Protein Products captured 87.3% of the Sports Nutrition Market in 2025, reflecting the category's dominance across retail and direct-to-consumer channels.

- Sports Non-Protein Products are forecast to register the fastest segment CAGR of 9.1% through 2035, driven by demand for functional energy and recovery formulations.

• By Source

- Animal-Based products held a 67.3% share of the Sports Nutrition Market in 2025, led by whey and casein derivatives.

- Plant-Based offerings are projected to grow at a 10.1% CAGR as vegan and flexitarian consumer segments expand globally.

• By Distribution Channel

- Online Retail Stores secured a 41.5% share and remain the fastest-growing channel at an 11.0% CAGR, outpacing brick-and-mortar formats.

• By Region

- North America led global revenue in the Sports Nutrition Market in 2025, while Asia-Pacific is set to grow fastest through 2035.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining primary interviews with manufacturers, distributors, and retailers alongside secondary data from trade associations and regulatory filings. Historical figures reflect actual reported sales, while forecast values apply the calibrated 7.45% CAGR with adjustments for macroeconomic cycles and category-specific demand shifts.

.webp?v=1783681832)