Sternal Closure Systems Market Summary

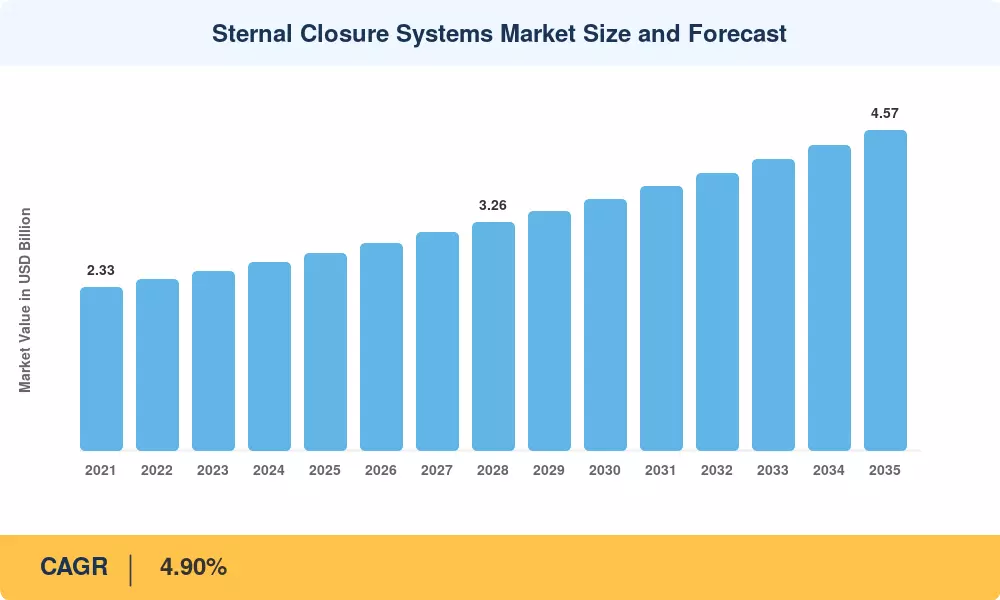

The Global Sternal Closure Systems Market size was valued at USD 2.82 Billion in 2025, and the market is projected to grow from USD 2.97 Billion in 2026 to USD 4.57 Billion by 2035, registering a CAGR of 4.90% during the forecast period 2026–2035. Two forces drive this trajectory: a global cardiac surgery caseload that continues to expand as populations age past 75, and a decisive shift in hospital procurement under value-based reimbursement, where readmission penalties push administrators toward closure technologies with documented complication-reduction profiles [1].

Generations are changing in the technology landscape. Multi-center registry data released in 2024 show rigid plate-and-screw fixation techniques lower rates of sternal dehiscence by 40–60% in high-risk cohorts, superseding legacy wire-based structures that have been the default for almost four decades [2]. The U.S. Centers for Medicare & Medicaid Services (CMS) bundled-payment expansion for cardiac events authorized in early 2025 has hastened this conversion as hospitals bear the full cost of 90-day problems, making the upfront premium for strict fixation economically rational [3].

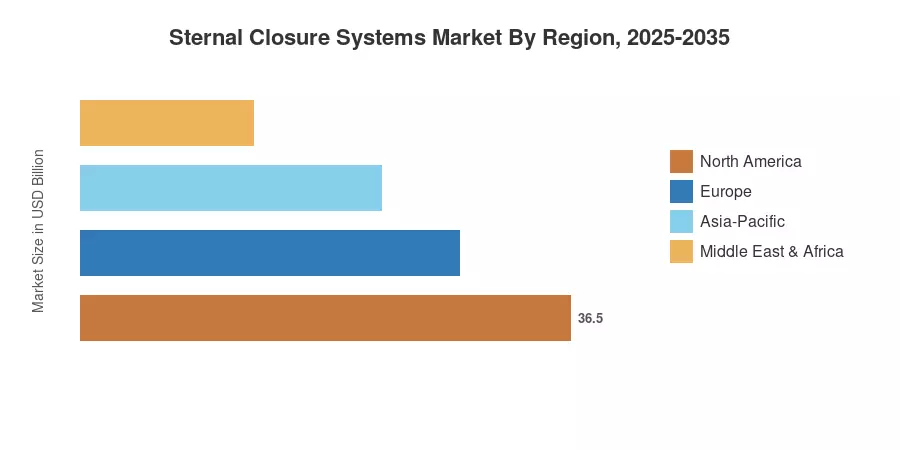

North America holds the largest share of the Sternal Closure Systems Market revenue, at almost 38.5%, owing to the presence of a dense cardiac surgery infrastructure and payer incentives. Asia-Pacific is the fastest growing region, with a CAGR of 10.4% through 2035, driven by new cardiac facilities in India, China and Southeast Asia. Europe has the second-highest share at ~29%, driven by national cardiovascular programs in Germany, the UK and France. The next decade will be defined by how fast emerging nations embrace improved closure technologies as procedure volumes rise.

Key Report Takeaways

• By Product Type

- Wires accounted for approximately 48% of the Sternal Closure Systems Market in 2025, sustained by low unit cost and surgeon familiarity.

- Plates and screws are forecast to register the fastest segment CAGR of 8.5% through 2035, reflecting growing clinical evidence for rigid fixation in obese and diabetic patients.

- Bone cement applications remain a niche but expanding category, primarily for revision sternotomies.

• By Procedure

- Median sternotomy represented roughly 72% of the Sternal Closure Systems Market share in 2025.

- Bilateral thoracosternotomy is expected to post a 10.5% CAGR through 2035, driven by complex congenital and oncology resections.

• By Geography

- North America contributed 38.5% of global revenue in 2025.

- Asia-Pacific is projected to expand at a 10.4% CAGR, the highest among all regions, fueled by government cardiac-care investment programs.

Sternal Closure Systems Market Size and Forecast (2021–2035)

The market size is calculated from primary interviews with cardiovascular surgeons, procurement directors and device distributors in 22 countries, triangulated against business filings, surgical registry databases and regulatory approval records. Historical numbers (2021–2024) are taken from audited shipment data; projection values are based on a calibrated compound-growth model, adjusted for demographic, reimbursement, and technology-adoption variables.