Syringe Needle Market Summary

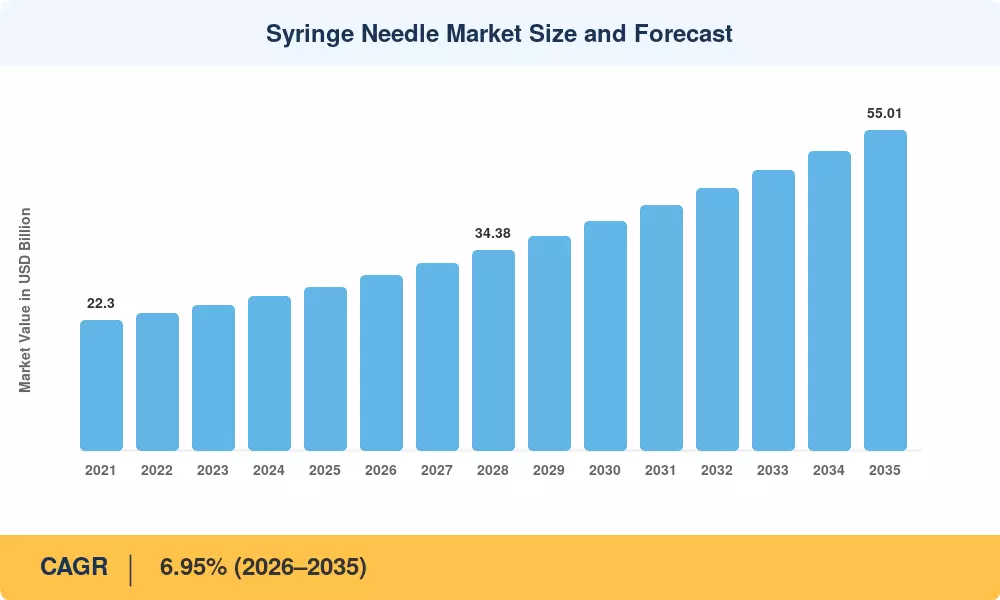

The Syringe and Needle Market size was valued at USD 28.10 Billion in 2025, and the market is projected to grow from USD 30.05 Billion in 2026 to USD 55.01 Billion by 2035, registering a CAGR of 6.95% during the forecast period 2026–2035. This expansion is being fueled by rising global immunization campaigns — the WHO's Immunization Agenda 2030 targets a 50% reduction in vaccine-preventable diseases by the end of the decade — and a rapid scale-up of GLP-1 receptor agonist therapies that require weekly or daily subcutaneous injections [1]. Government procurement commitments, particularly across Gavi-supported low- and middle-income countries, continue to generate sustained volume demand for the Syringe and Needle Market.

A structural transformation is reshaping how injectable therapies are delivered. Traditional glass-barrel reusable devices are giving way to single-use, auto-disable syringes mandated by WHO guidelines, while prefilled syringes are capturing share in biologics delivery pipelines. The U.S. Needlestick Safety and Prevention Act and the EU Medical Device Regulation (MDR 2017/745) have accelerated adoption of safety-engineered devices, with an estimated USD 3.2 billion invested globally in retractable and shielded needle technologies between 2022 and 2025 [2].

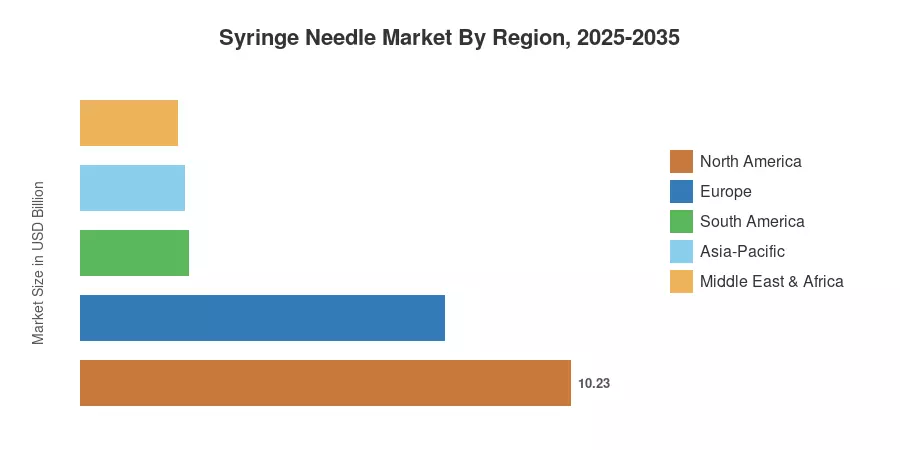

North America commands roughly 36.4% of global Syringe and Needle Market revenue, anchored by high per-capita healthcare spending and stringent occupational safety mandates. Asia-Pacific represents the fastest-growing region at a projected 7.75% CAGR, propelled by universal health coverage expansions in India and China's centralized procurement reforms. Europe holds the second-largest share at approximately 27%, with Germany and France leading demand through hospital automation and chronic disease management programs. The next decade will be defined by self-administration platforms and connected injection devices that generate real-time adherence data.

Key Report Takeaways

• By Product Category

- Syringes held an estimated 70.2% revenue share of the Syringe and Needle Market in 2025, driven by single-use and auto-disable formats mandated across immunization programs.

- Needles are advancing at approximately 7.45% CAGR through 2035, reflecting rising demand from blood collection, biopsy, and point-of-care diagnostics.

• By Material

- Plastic-based devices captured 48.4% of the Syringe and Needle Market share in 2025, supported by cost advantages and lightweight design.

- Stainless-steel components are expanding at a 7.35% CAGR, underpinned by precision-engineering requirements in specialty needles.

• By Application

- Insulin administration accounted for 32.6% of total Syringe and Needle Market revenue in 2025, correlating with the 537 million adults living with diabetes globally.

- Blood collection is the fastest-growing application at a 7.60% CAGR through 2035.

• By End User

- Hospitals and clinics represented 49.1% of Syringe and Needle Market demand in 2025.

- Home-healthcare settings post the strongest end-user CAGR at 7.65%, reflecting chronic disease self-management trends.

• By Region

- North America led the Syringe and Needle Market with a 36.4% revenue share in 2025.

- Asia-Pacific is projected to grow at 7.75% CAGR during 2026–2035.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from import/export trade databases, manufacturer revenue disclosures, hospital procurement records, and WHO/UNICEF supply division data. Forecast projections incorporate epidemiological trend models, regulatory pipeline analysis, and macroeconomic healthcare expenditure assumptions across 45 countries.