Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

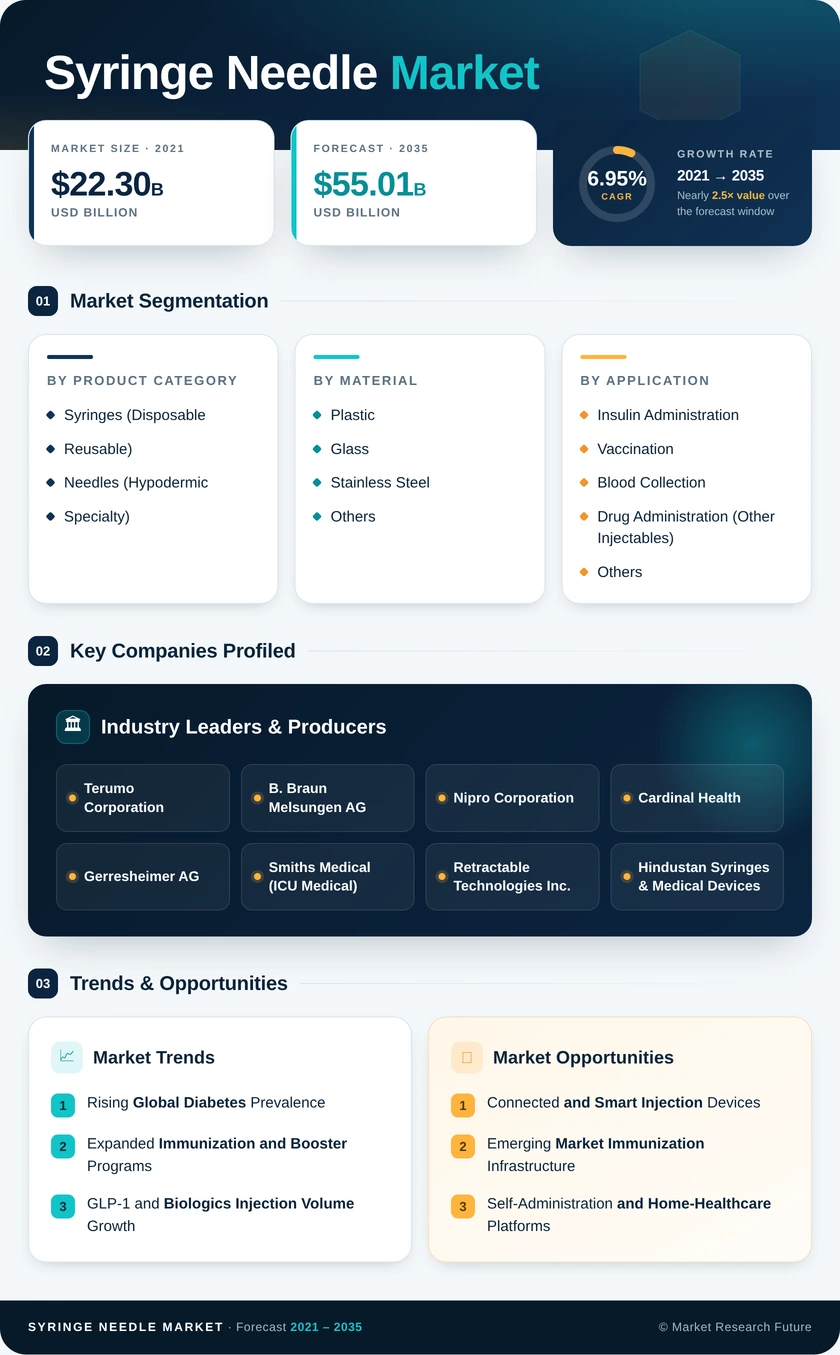

| Product Category | Syringes (Disposable, Reusable); Needles (Hypodermic, Specialty) | Syringes | Needles |

| Material | Plastic; Glass; Stainless Steel and Others | Plastic | Stainless Steel and Others |

| Application | Insulin Administration; Vaccination; Blood Collection; Drug Administration (Other Injectables); Others | Insulin Administration | Blood Collection |

| End User | Hospitals and Clinics; Home Healthcare; Ambulatory Surgery Centers; Others (Labs, Blood Banks) | Hospitals and Clinics | Home Healthcare |

Market Segmentation Overview

By Product Category

| Sub-Segment | Key Trend |

| Syringes (Disposable) | WHO auto-disable mandates drive high-volume procurement cycles globally |

| Syringes (Reusable) | Retained in veterinary, laboratory, and select anesthesia applications |

| Needles (Hypodermic) | Standard injection and blood collection workhorse across all care settings |

| Needles (Specialty) | Growing demand from biopsy, cryoablation, and interventional procedures |

Disposable syringes represent the largest volume sub-segment, underpinned by infection prevention mandates and single-use regulatory requirements across immunization programs. Specialty needles are gaining traction as minimally invasive diagnostic and therapeutic procedures expand globally.

By Material

| Sub-Segment | Key Trend |

| Plastic | Cost-effective polypropylene barrels dominate disposable syringe production |

| Glass | Type I borosilicate glass essential for prefilled biologic drug containment |

| Stainless Steel and Others | All needle cannulae require medical-grade stainless steel; polymer-coated variants emerging |

Plastic materials lead by volume due to low manufacturing cost and lightweight logistics advantages. Glass is experiencing renewed demand as the biologics pipeline accelerates and drug-container interaction testing favors inert glass surfaces for long-term stability.

By Application

| Sub-Segment | Key Trend |

| Insulin Administration | Growing diabetes patient base drives the largest application share |

| Vaccination | Routine immunization and pandemic preparedness sustain steady volumes |

| Blood Collection | Laboratory automation and expanded blood bank networks fuel growth |

| Drug Administration (Other Injectables) | Oncology, biologics, and pain management injections expanding |

| Others | Veterinary, cosmetic, and research injection applications |

Insulin administration remains the dominant application due to the chronic, recurring nature of diabetes management and the high frequency of daily injections. Blood collection is the fastest-growing application as point-of-care testing platforms proliferate and developing nations invest in blood bank infrastructure.

By End User

| Sub-Segment | Key Trend |

| Hospitals and Clinics | Bulk GPO contracts and standardized formularies anchor institutional demand |

| Home Healthcare | Chronic disease self-management shifting injection volumes to home settings |

| Ambulatory Surgery Centers | Outpatient procedure migration creates concentrated device demand |

| Others (Labs, Blood Banks) | Diagnostic testing and blood donation collection needs |

Hospitals and clinics account for the largest share of device consumption, while home healthcare is the fastest-growing channel as healthcare systems incentivize outpatient chronic disease management and patient self-injection programs.