Tetanus Toxoid Vaccine Market Summary

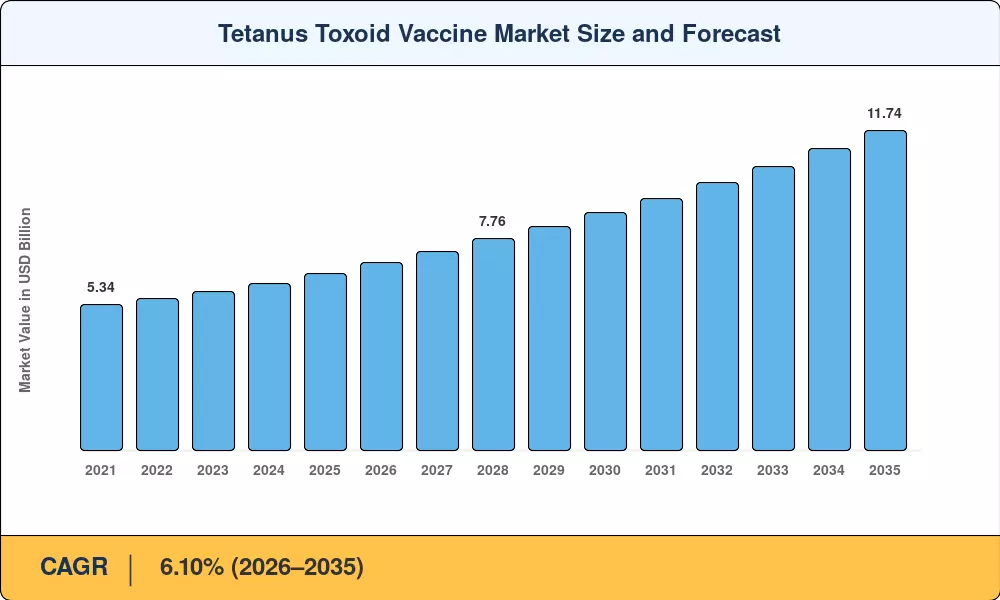

The Global Tetanus Toxoid Vaccine Market size was valued at USD 6.50 Billion in 2025, and the market is projected to grow from USD 6.89 Billion in 2026 to USD 11.74 Billion by 2035, registering a CAGR of 6.10% during the forecast period 2026–2035. Two forces are pulling investment into this space: the WHO's expanded Immunization Agenda 2030, which targets a 50% reduction in zero-dose children by the decade's end [1], and a wave of national adult booster mandates that are widening the addressable population beyond paediatric cohorts. Gavi, the Vaccine Alliance, committed over USD 1.3 billion in 2024–2025 procurement cycles for combination vaccines that include tetanus antigens, signalling sustained multilateral demand [2].

The product pipelines are shifting away from stand-alone tetanus toxoid formulations towards acellular combination treatments, primarily Tdap and DTaP, which combine diphtheria and pertussis antigens in a single injection. This move alleviates the burden of clinic visits and is aligned with life-course vaccination regimens now codified in the national schedules of the U.S., EU and India. The next turning point is thermostable vaccine technology – a Phase I trial of a fridge-free Td formulation initiated in April 2025 seeks to halve cold-chain losses across sub-Saharan Africa and South Asia [3].

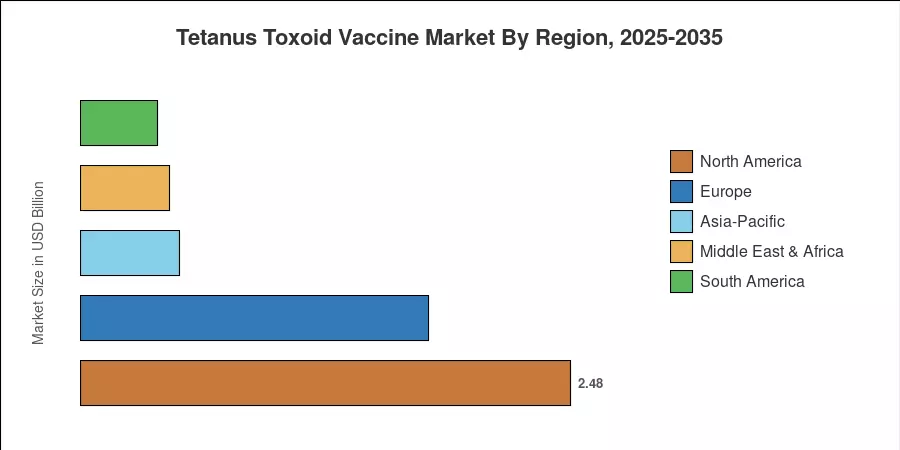

North America accounts for over 38.2% of the revenue share of the Tetanus Toxoid Vaccine Market due to the strong insurance reimbursement and universal childhood vaccination. Asia-Pacific is the fastest expanding area with a CAGR of 7.65%, mainly due to India’s Universal Immunization Programme (UIP) and China’s enhanced EPI schedule. Europe has the second greatest proportion of the total market at around 27%, supported by robust public procurement regimes. The Tetanus Toxoid Vaccine Market is undergoing a period of regulatory modernization and geographic diversification that will determine its trajectory through 2035 as manufacturer consolidation reshapes supply chains.

Key Report Takeaways

• By Vaccine Type

- DTaP held an estimated 44.2% share of the Tetanus Toxoid Vaccine Market in 2025, driven by universal paediatric immunization mandates across 130+ countries.

- Tdap formulations are forecast to expand at an 8.35% CAGR through 2035 as adult booster adoption accelerates and maternal immunization programmes scale.

- Standalone TT vaccines accounted for approximately USD 0.52 billion in 2025, though regulatory trends favour combination products.

• By End User & Distribution

- Hospitals and trauma centres captured approximately 72.0% of the Tetanus Toxoid Vaccine Market revenue in 2025

- Government procurement channels represented 66.5% of 2025 distribution volume, reflecting the dominance of public-sector purchasing.

- The private and self-pay channel is projected to register a 7.55% CAGR as out-of-pocket booster demand grows in middle-income economies.

• By Geography

- North America controlled 38.2% of the Tetanus Toxoid Vaccine Market in 2025

- Asia-Pacific is positioned as the fastest-growing region at 7.65% CAGR through 2035, fuelled by public health budget expansion across India, Indonesia, and the Philippines.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)’s estimates are based on proprietary demand models and triangulated against WHO/UNICEF procurement data, firm filings, and country immunization programme budgets. Historical numbers include reported tender volumes and ex-factory pricing. Forecast forecasts include population growth rates, planned policy expansions and pipeline readiness assessments.

.webp?v=1782120130)