Thermoplastic Polyurethane Market Summary

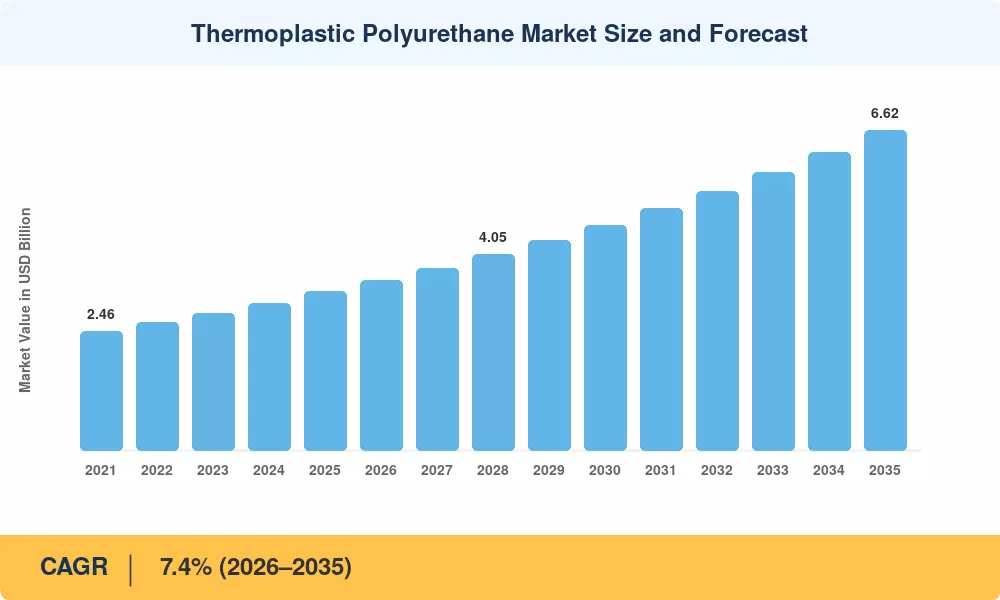

The Thermoplastic Polyurethane Market reached an estimated USD 3.28 Billion in 2025 and is projected to grow from USD 3.48 Billion in 2026 to USD 6.62 Billion by 2035, registering a CAGR of 7.4% across the forecast window. Two catalysts are reshaping demand trajectories: tightening volatile-organic-compound (VOC) emission regulations across the EU and North America are pushing manufacturers away from solvent-based adhesives toward reactive and water-borne TPU grades, while a parallel push for bio-based feedstocks — backed by over USD 1.2 billion in green-chemistry venture investments between 2022 and 2024 — is accelerating reformulation cycles [1].

The current technological transition in the thermoplastic polyurethane market is characterized by a structural shift from commodity polyester grades to specialized and performance-engineered formulations. TPU is gradually overtaking traditional rubber mixes and PVC-based flexible polymers in consumer electronics housings, medical wearables, and car interiors. An estimated 15–18% of European flexible-plastics procurement budgets have been moved toward halogen-free TPU alternatives as a result of the EU's revised REACH limits on phthalate plasticizers, which went into force in 2025 [2].

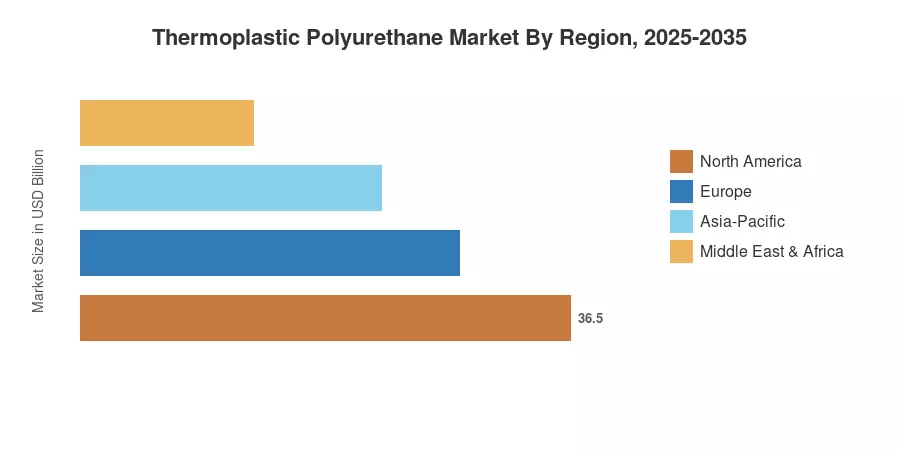

Due to China's strong converter base and India's growing footwear manufacturing industry, the Asia-Pacific region accounts for around 63% of the world's thermoplastic polyurethane market revenue. Additionally, the region has the fastest CAGR, projected to be 8.3% through 2035. North America has around 18% of the market thanks to mandates for the reshoring of medical devices and investments in the electric vehicle (EV) supply chain. Europe, which makes up around 13% of the total, favors circular economy regulations that call for single-material buildings that can be mechanically recycled. The capacity of backward-linked 1,4-butanediol (BDO), recycled-content thresholds, and the rate at which EV OEMs implement solvent-free in-mold decoration will determine the course of the next ten years.

Key Report Takeaways

• By Product Type

- Polyester TPU accounted for approximately 43.5% of global revenue in 2025, reflecting its cost-performance balance in film and sheet extrusion applications.

- Polycaprolactone TPU is set to record a CAGR of roughly 8.9% between 2026 and 2035, fueled by medical-grade demand for validated ISO 10993 biocompatible compounds.

• By Application

- Extruded products represented the largest application segment in the Thermoplastic Polyurethane Market in 2025 with an estimated 47.3% share.

- Injection-molded products are projected to expand at a CAGR near 8.6% through 2035, driven by automotive lightweighting requirements.

• By End-Use Industry

- Footwear held roughly 33% of the Thermoplastic Polyurethane Market in 2025, anchored by athletic and performance-shoe midsole adoption.

- The automotive segment is anticipated to grow at approximately 8.7% CAGR as EV platform designs specify TPU for cable sheathing and interior skins.

• By Regional

- Asia-Pacific captured an estimated 63% of the global Thermoplastic Polyurethane Market revenue in 2025.

- North America's share stood at about 18%, underpinned by medical-device and EV-related procurement.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a combination of primary interviews with resin producers and converters, trade-association shipment data, and cross-referencing with published industry benchmarks. Historical figures (2021–2024) rely on customs-level import/export reconciliation and disclosed company revenues, while forecast projections apply a calibrated compound growth model anchored to the 2025 base year.