Thin Film Solar Cell Market Summary

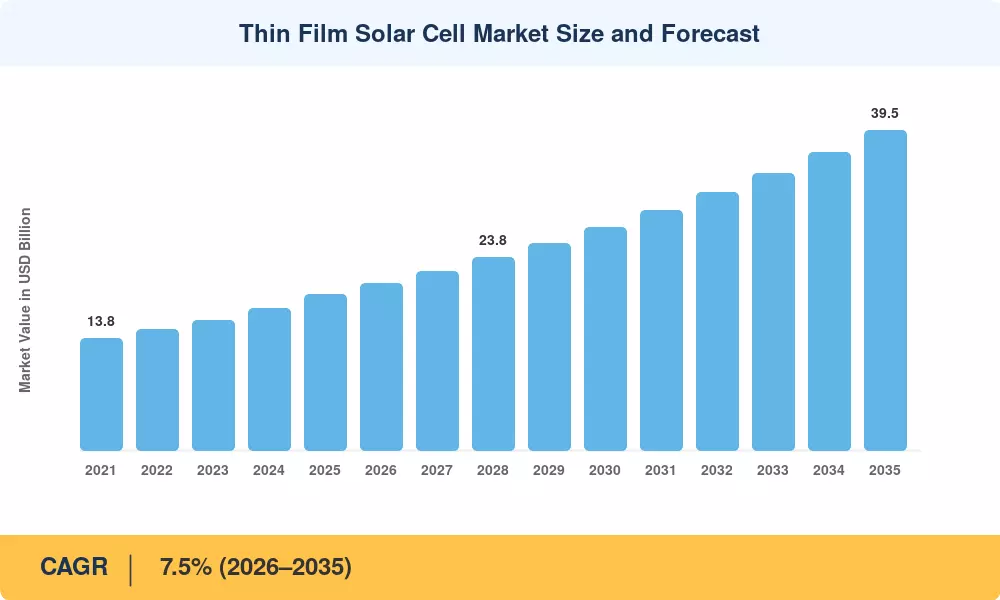

The global Thin Film Solar Cell Market reached an estimated USD 19.2 billion in 2025 and is projected to grow from USD 20.6 billion in 2026 to USD 39.5 billion by 2035, registering a compound annual growth rate of 7.5% across the forecast period. This expansion is anchored in two powerful catalysts: the U.S. Inflation Reduction Act's extension of manufacturing tax credits through 2032, which has unlocked over USD 8 billion in domestic thin film production capacity commitments [1], and the European Union's revised Renewable Energy Directive targeting 42.5% renewable electricity by 2030 [2].

The thin-film solar cell market's technological environment is drastically changing. Copper indium gallium selenide (CIGS) panels, which have raised laboratory efficiencies beyond 23.6%, now pose a serious threat to cadmium telluride (CdTe) modules, which have long dominated the market due to their cost-per-watt advantage [3]. The next commercial frontier for thin-film photovoltaics is perovskite-silicon tandem designs, which have surpassed 33% efficiency limits in laboratory conditions [4]. Installations of legacy amorphous silicon (a-Si) are still declining as manufacturers reallocate funds to chemistries with higher yields.

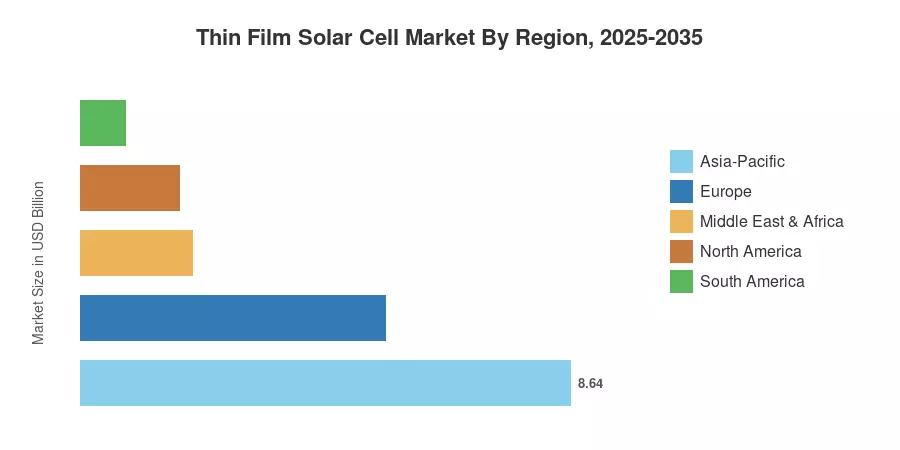

Due to India's aggressive solar capacity ambitions under the PM-KUSUM plan and China's industrial dominance, the Asia-Pacific holds around 45% of the Thin Film Solar Cell Market [5]. With a CAGR of 9.1%, North America is the fastest-growing area thanks to utility-scale project pipelines and reshoring incentives. Due to building-integrated PV mandates in Germany, France, and the Netherlands, Europe accounts for about 28% of global income [6]. The thin-film solar cell market is expected to grow steadily by double digits in a few regions through the early 2030s as grid-parity economics improve throughout emerging markets.

Key Report Takeaways

• By Technology

- CdTe technology commands roughly 52% of the Thin Film Solar Cell Market revenue, reflecting First Solar's vertically integrated manufacturing scale and module cost leadership.

- CIGS technology is expanding at a CAGR of 9.3% through 2035, driven by efficiency gains and growing demand for flexible substrates in commercial rooftop applications.

- Emerging organic and perovskite-based thin film cells account for approximately USD 1.5 billion in 2025, with rapid R&D commercialization expected by 2028.

• By Application

- Utility-scale solar farms represent the largest application, valued at approximately USD 9.2 billion in 2025.

- Building-integrated photovoltaic (BIPV) installations are growing at 11.2% CAGR, the fastest among all application segments in the Thin Film Solar Cell Market.

• By Region

- Asia-Pacific holds a dominant share at 45%, led by Chinese CdTe and CIGS module production.

- North America is accelerating at 9.1% CAGR, driven by IRA manufacturing incentives and domestic content requirements.

- Europe generates roughly USD 5.4 billion in 2025 Thin Film Solar Cell Market revenue, anchored by aggressive decarbonization mandates.

Thin Film Solar Cell Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up module shipment data from manufacturer filings, import-export trade databases, and top-down cross-referencing against IRENA and IEA capacity addition reports. All figures are denominated in constant 2025 USD to eliminate currency distortion. Historical values reflect actual installations and module sales; forecast figures apply technology-specific adoption curves calibrated to policy visibility and manufacturing capacity announcements [7].