Threat Intelligence Market Summary

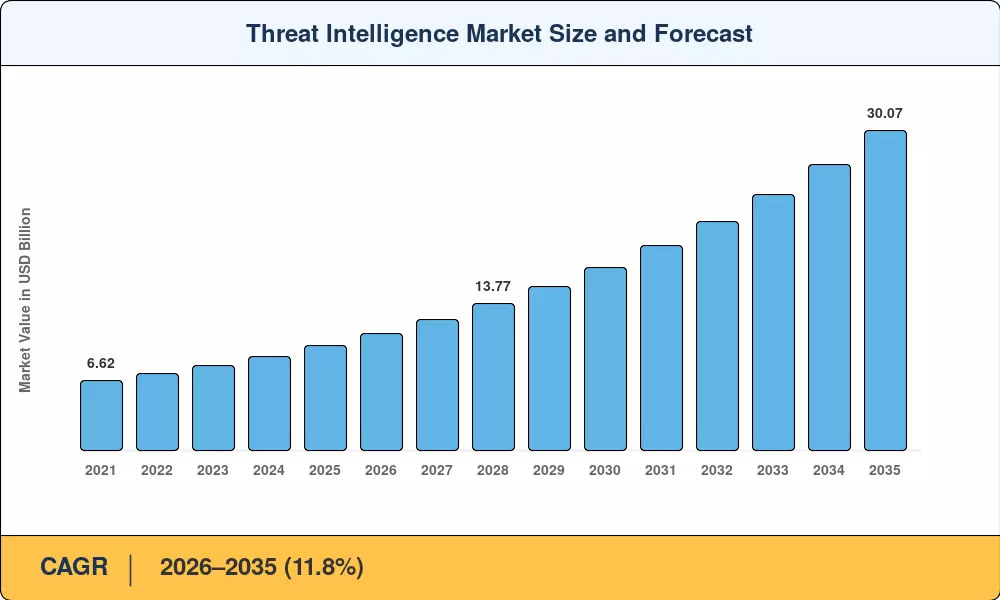

The 9 reached USD 9.86 billion in 2025 and is projected to climb to USD 30.07 billion by 2035, registering an 11.8% CAGR during 2026–2035. Two catalysts are powering this trajectory: the EU's NIS2 Directive, which compels roughly 160,000 entities across Europe to formalize intelligence-sharing programs [2], and the U.S. Securities and Exchange Commission's 2024 cyber-incident disclosure mandate, which pushed boardroom spending on proactive intelligence to record levels [7]. The Threat Intelligence Market is no longer a niche procurement line — it sits at the center of enterprise risk management.

AI-enhanced, context-aware intelligence solutions that can correlate indicators across cloud, endpoint, and operational-technology settings are replacing legacy signature-based protections. Global cybersecurity spending surpassed USD 215 billion in 2024 [12], and a growing share of that budget now flows toward intelligence functions that reduce mean-time-to-detect. Compared to peers who relied on ad hoc feeds, companies that implemented integrated intelligence platforms reduced breach costs by an average of USD 1.3 million [3].

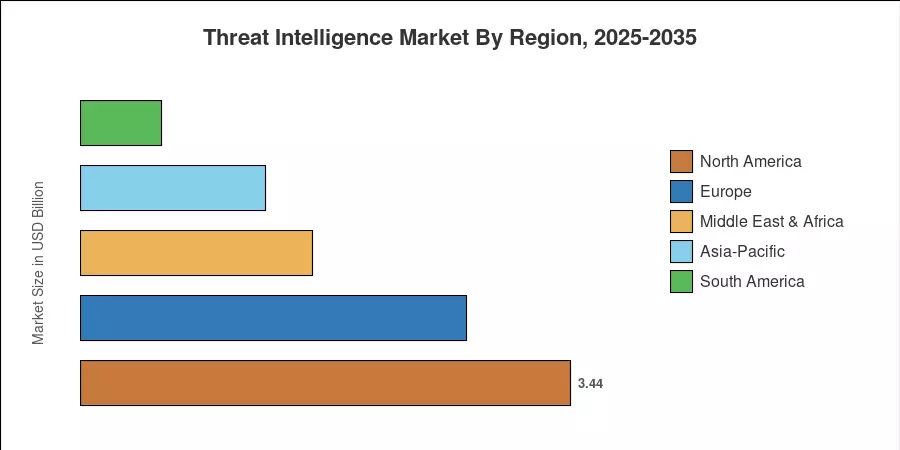

Due to a rich vendor ecosystem and federal mandates, North America has approximately 34.9% of the threat intelligence market. Due to NIS2 transposition spending, Europe comes in second at USD 2.71 billion in 2025. With a 16.5% CAGR, the Middle East and Africa area is the fastest-growing geography as Gulf states make significant investments in their own cyber-defense infrastructure. Through digital transformation initiatives in South Korea, Japan, and India, the Asia-Pacific region expands in size, indicating ten years of consistent demand.

Key Report Takeaways

• By Component & Deployment

- Solutions accounted for 59.2% of the Threat Intelligence Market in 2025, reflecting enterprise demand for unified analytics consoles and automated enrichment engines.

- Cloud deployment is expanding at a 17.5% CAGR through 2035 as organizations migrate from on-premise appliances to SaaS-delivered intelligence.

- The Services segment is on track for a 15.1% CAGR, led by managed intelligence retainers and incident-response advisory engagements.

• By End-User

- IT and Telecommunications captured 22.1% of the Threat Intelligence Market share in 2025, driven by carrier-grade visibility requirements.

- BFSI is the fastest-growing end-user vertical at a 15.8% CAGR, propelled by fraud-intelligence convergence and cyber-insurance mandates.

- Organization Size

- Large enterprises held 62.5% of the market in 2025; SME adoption is accelerating at a 13.8% CAGR as managed-service bundles lower entry barriers.

• By Geography

- North America dominated with 34.9% of global revenue in 2025.

- The Middle East & Africa region leads growth at a 16.5% CAGR, fueled by Saudi Arabia's Vision 2030 cybersecurity directives.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates vendor revenues, enterprise procurement surveys, and regulatory compliance spending trackers. Historical values (2021–2024) rely on audited annual filings and spending benchmarks [12], while the forecast period (2026–2035) applies a calibrated compound growth model validated against comparable industry assessments [19].