Transformer Oil Market Summary

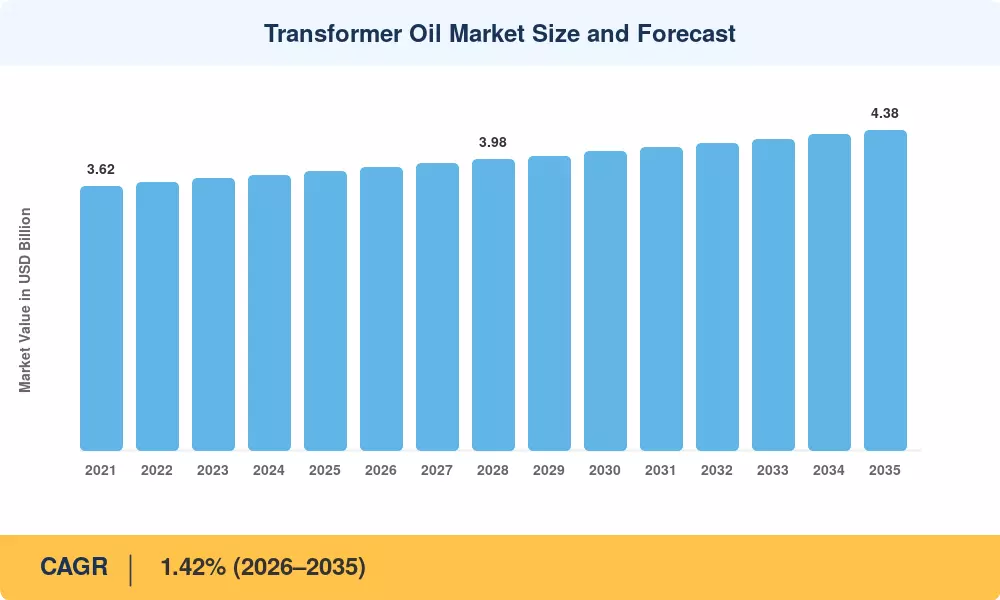

The Transformer Oil Market reached an estimated USD 3.82 Billion in 2025 and is projected to grow from USD 3.87 Billion in 2026 to USD 4.38 Billion by 2035, registering a CAGR of 1.42% during the forecast period (2026–2035). This steady expansion is anchored by grid-reinforcement programs across Asia-Pacific and mandated replacement of aging transformer fleets in North America and Europe. Governments in India and China alone have committed over USD 85 billion in transmission infrastructure upgrades through 2030, driving sustained demand for insulating oil and dielectric fluids [2][3].

A quiet but consequential shift is reshaping the Transformer Oil Market from the inside. While mineral insulating oil still accounts for the vast majority of global consumption, tightening Group-I base-oil supplies and rising disposal costs are eroding its traditional price advantage. Bio-based esters — backed by fire-safety codes, biodegradability mandates, and the growing footprint of urban substations and data centers — are carving out a meaningful share. The IEC 62770 standard for natural ester fluids has accelerated adoption in environmentally sensitive zones, and several European utilities now specify bio-based electrical transformer fluids for all new indoor installations [4][5].

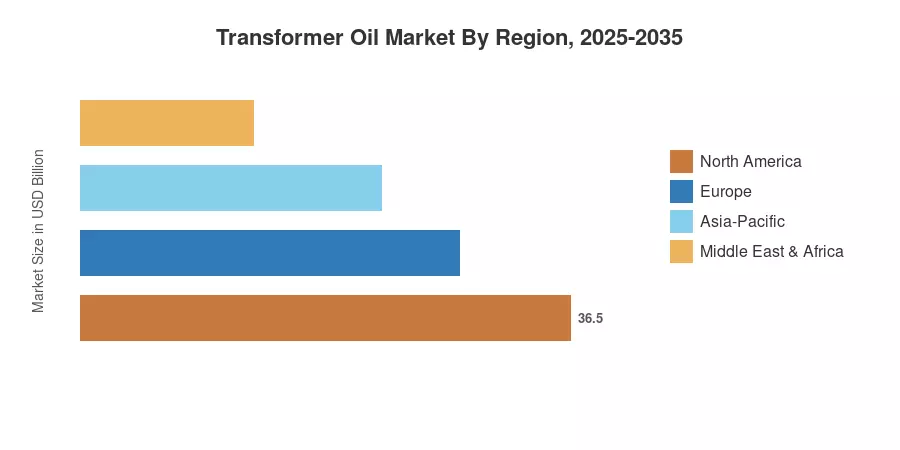

Asia-Pacific commands the largest regional share at roughly 51% of the global Transformer Oil Market, propelled by massive electrification in India and grid modernization in China. North America follows with approximately 22% share, where utility transformer fluids replacement cycles drive recurring demand. Europe is the fastest-maturing region for bio-based cooling oils for transformers, supported by EU sustainability directives. The next decade will see rising procurement from offshore-wind converter platforms and HVDC corridors, pushing the Transformer Oil Market into new technical territory

Key Report Takeaways

• By Type

- Mineral-based insulating oil held the dominant position with approximately 95% of volume consumed in 2025, reflecting legacy fleet inertia and cost familiarity

- Bio-based esters are projected to grow at a CAGR of 8.5% during 2026–2035, the fastest among all types in the Transformer Oil Market

- Silicone-based dielectric fluids maintain a niche but stable share, primarily in high-temperature specialty applications

• By Application

- Transformers accounted for approximately 78% of total volume in 2025, reinforcing their role as the primary consumption driver in the Transformer Oil Market

- Switchgear and circuit breaker applications are expanding steadily as utilities replace aging high voltage insulation oil in distribution networks

• By Region

- Asia-Pacific captured a CAGR of 1.95% — the fastest among all regions — driven by India's Revamped Distribution Sector Scheme and China's State Grid investments

- North America contributed approximately USD 0.84 Billion in 2025, sustained by transformer maintenance oil demand across aging utility infrastructure

- Europe is pioneering regulatory-driven adoption of bio-based electrical insulation fluids in urban substations

Market Size and Forecast (2021–2035)

The market sizing combines bottom-up volume tracking from transformer OEM shipment data, utility procurement records, and refinery output for naphthenic and paraffinic base oils, triangulated against top-down demand models anchored to installed transformer capacity and replacement cycles. Historical data (2021–2024) is derived from trade statistics, customs data, and annual reports from major power transformer oil suppliers. Forecast projections (2026–2035) apply the calibrated 1.42% CAGR with adjustments for policy-driven demand surges.