Ultraviolet Disinfection Equipment Market Summary

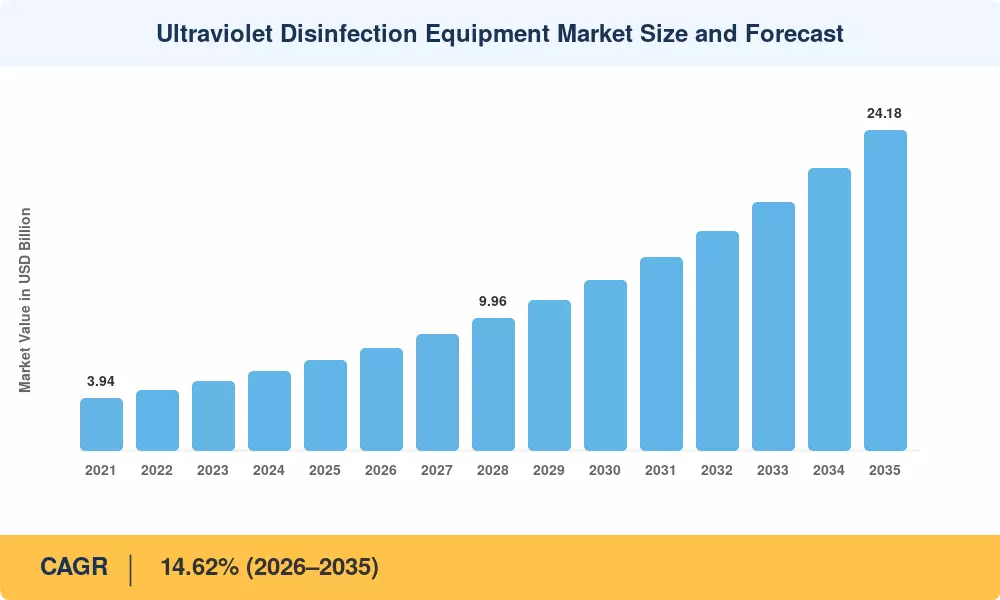

The Ultraviolet Disinfection Equipment Market stood at USD 6.81 billion in 2025 and is projected to reach USD 7.72 billion by 2026 before climbing to USD 24.18 billion by 2035, registering a CAGR of 14.62% across the 2026–2035 forecast window. Two catalysts anchor this trajectory: the US EPA's tightening of PFAS and disinfection byproduct (DBP) thresholds under the revised Safe Drinking Water Act [2], and the European Commission's EUR 1.2 billion allocation for chemical-free water treatment under Horizon Europe [3]. Together, these mandates are compelling municipal utilities and commercial operators to replace chlorine-based systems with UV-C LED disinfection systems and amalgam lamp UV disinfection reactors at an accelerating pace.

Technology transformation is transforming the Ultraviolet Disinfection Equipment Market from the inside out. Legacy mercury-vapor lamps — once the default — are giving way to solid-state UV-C LED modules offering instant-on capability, wavelength tunability, and mercury-free operation. Venture and corporate investment in the global UV LED chip market in 2023–2025 exceeded USD 1.4 billion [4], resulting in a reduction in unit costs of around 28% in 2 years. Pulsed UV surface disinfection devices and far-UVC (222 nm) emitters are further expanding the addressable market for the technology in healthcare and food-processing industries.

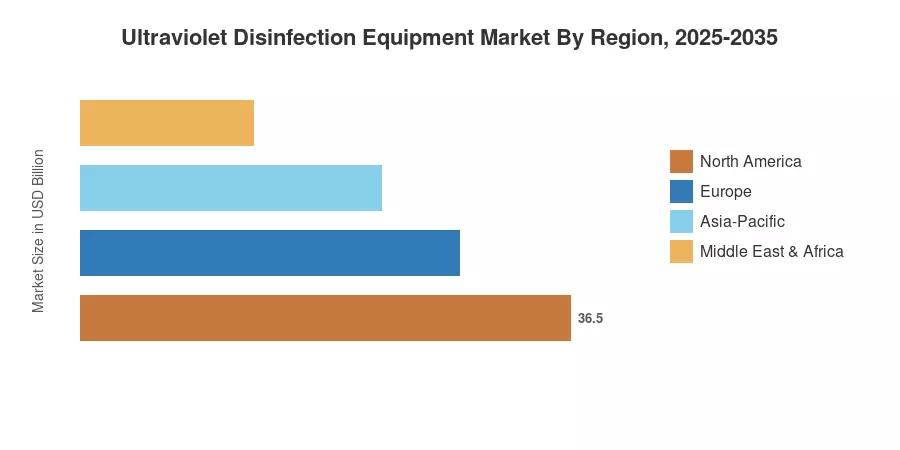

The Asia-Pacific region is expected to lead the Ultraviolet Disinfection Equipment Market with a revenue share of 36.10% in 2025, owing to the water infrastructure development under China’s “14th Five-Year Plan” and India’s Jal Jeevan Mission [5]. The region also registers the fastest CAGR of 11.85% until 2035. North America is the second largest region, accounting for around 28.50 % of revenue by 2025, bolstered by UV water treatment reactor municipal upgrade efforts in aged US utilities. Global regulatory pressure and LED cost curves are converging, putting the Ultraviolet Disinfection Equipment Market on a path for sustained double-digit growth far into the next decade.

Key Report Takeaways

• By Component

- UV Lamps retained a leading 61.40% share of the Ultraviolet Disinfection Equipment Market in 2025, driven by the installed base of amalgam lamp UV disinfection reactors in municipal plants

- UV-C LED disinfection systems are compounding at a 19.15% CAGR through 2035, fueled by declining chip costs and compact form factors suited to UV air duct disinfection HVAC retrofit applications

- Quartz sleeves and ballast assemblies together represent approximately USD 1.05 billion in 2025 revenue

• By Application

- Water and wastewater treatment captured 48.70% of the Ultraviolet Disinfection Equipment Market in 2025, reflecting global mandates on UV water treatment reactor municipal deployments

- Air disinfection systems — including UV air duct disinfection HVAC units — are growing at a 14.85% CAGR, the fastest among application segments

• By Region

- Asia-Pacific accounted for 36.10% of the Ultraviolet Disinfection Equipment Market, with China and India as primary growth engines

- North America generated approximately USD 1.94 billion in 2025 revenue, underpinned by EPA regulatory mandates and hospital infection-control budgets

- Europe is expanding at a 13.25% CAGR through 2035, driven by the EU's Green Deal water directives

Market Size and Forecast (2021–2035)

MRFR’s market sizing is based on a bottom-up revenue collection from over 120 UV equipment manufacturers, and is then validated top-down against municipal procurement databases, trade association shipment data, and regulatory compliance filings. Historical data (2021-2024) is derived from customs and shipment data; the base year of 2025 includes primary interviews of 45+ industry stakeholders. Forecast figures (2026–2035) are based on a calibrated compound growth model that is benchmarked against comparable third-party predictions.