Ureteral Stents Market Summary

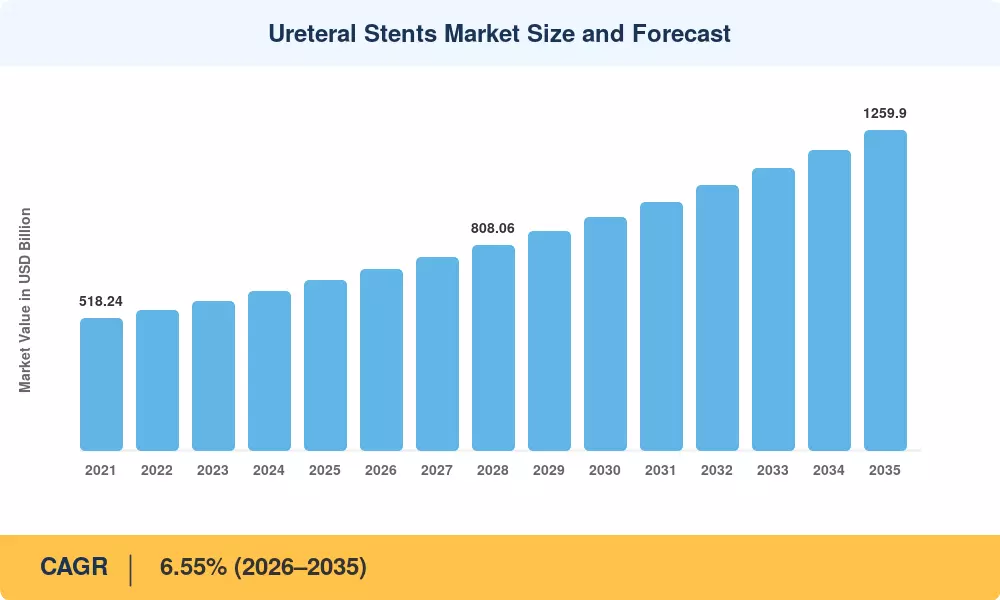

The Global Ureteral Stents Market size was valued at USD 668.0 Million in 2025, and the market is projected to grow from USD 711.8 Million in 2026 to USD 1,259.9 Million by 2035, registering a CAGR of 6.55% during the forecast period 2026–2035. Rising kidney stone prevalence—now affecting roughly 10% of US adults according to recent epidemiological data [1]—drives procedure volumes higher each year, while aging populations across developed economies amplify demand for less invasive drainage interventions. FDA clearances for next-generation biodegradable designs are accelerating product turnover cycles and reshaping how urologists approach post-procedural stent management [2].

Material science is transforming this space at its foundation. Legacy polyurethane and silicone stents still dominate operating theaters, but anti-encrustation nano-coatings and radiopaque biodegradable polymers are redefining performance benchmarks. Manufacturers invested over USD 280 million in urology-specific R&D during 2024 alone, with a significant portion directed toward drug-eluting platforms and AI-guided placement technologies [14]. These innovations target the persistent clinical challenge of encrustation-related complications that affect up to 58% of indwelling stents beyond 12 weeks [17].

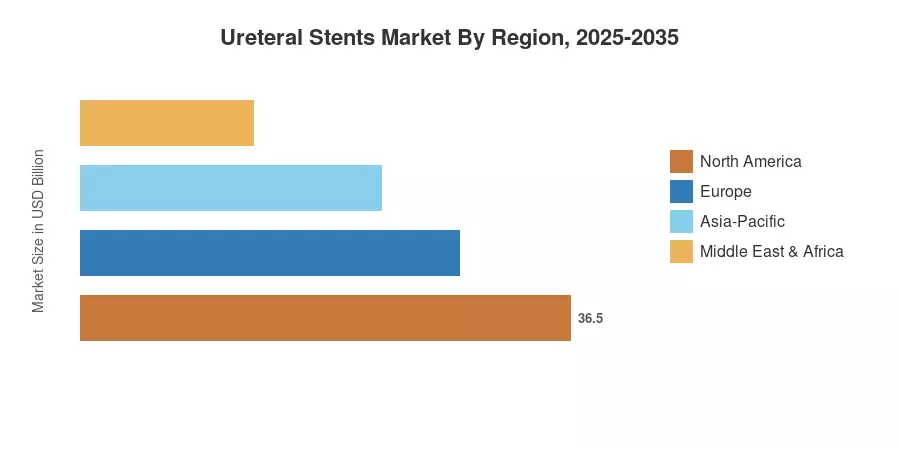

North America commands roughly 38.5% of the Ureteral Stents Market, underpinned by high procedural volumes and favorable reimbursement structures. Asia-Pacific is the fastest-growing region, projected to expand at an 8.15% CAGR through 2035, propelled by rising healthcare expenditure in China and India [21]. Europe holds the second-largest share at approximately 27.2%, with Germany and the UK leading adoption of double-J stent devices in ambulatory settings. The decade ahead will reward companies that balance biocompatibility innovation with cost containment across diverse healthcare systems.

Key Report Takeaways

• By Product Type

- Double pigtail stents captured approximately 42.1% of the Ureteral Stents Market share in 2025, reflecting their broad clinical versatility across stone management, transplant, and tumor indications

- Biodegradable stent designs are expanding at a projected 10.75% CAGR through 2035, driven by clinician demand for the elimination of secondary removal procedures

• By Material

- Polyurethane remains the dominant material category, holding approximately 44.8% of segment revenue in the base year

• By Application

- Kidney stone management represented roughly 56.8% of the Ureteral Stents Market in 2025, correlating directly with escalating global nephrolithiasis incidence

- Tumor-related ureteral obstruction procedures are forecast to grow at an 8.95% CAGR as oncology survival rates improve, and palliative stenting demand increases

• By End User

- Hospitals accounted for 63.0% of end-user demand, though ambulatory surgical centers are gaining share rapidly

• By Region

- North America led all regions by revenue in 2025, supported by mature insurance frameworks and high per-capita procedure rates

- Asia-Pacific is the fastest-growing regional segment, registering an 8.15% CAGR driven by infrastructure investment in China, India, and ASEAN nations

- Europe contributed USD 181.7 million in 2025, with Western European countries anchoring demand through established urology referral networks

Ureteral Stents Market Size and Forecast (2021–2035)

Market Research Future constructed the forecast model using a triangulated methodology combining bottom-up device shipment analysis, top-down healthcare expenditure benchmarks, and validated company revenue disclosures. Historical figures (2021–2024) draw on hospital procurement databases and regulatory filing volumes, while 2026–2035 projections apply the calibrated 6.55% CAGR alongside demographic growth adjustments and procedure rate assumptions per regional epidemiological trends.