Vending Machine Market Summary

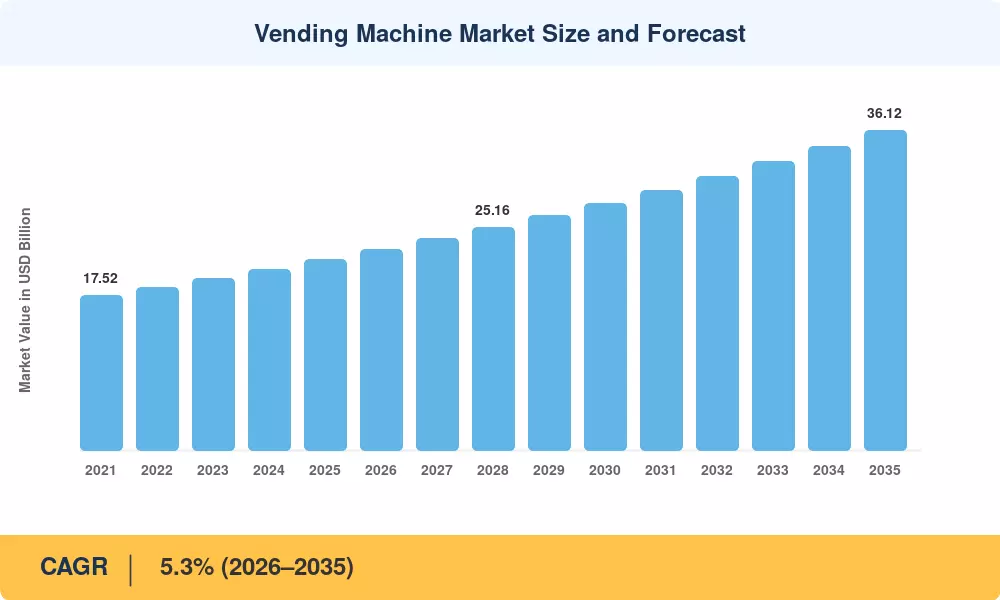

The global Vending Machine Market stood at an estimated USD 21.55 billion in 2025 and is projected to reach USD 36.12 billion by 2035, expanding at a compound annual growth rate of 5.3% during the 2026–2035 forecast window. Two catalysts anchor this trajectory: Japan's ongoing government-supported initiative to digitize 1.2 million legacy units [1], and the broader shift toward cashless retail infrastructure accelerated by post-pandemic consumer behavior. The Vending Machine Market has evolved well beyond coin-operated dispensers — it is now a software-defined retail channel attracting venture capital and strategic corporate investment.

Technology transformation sits at the core of this expansion. Traditional mechanical-lever machines, which still account for roughly a third of the installed base in emerging economies, are being replaced by telemetry-enabled, touchscreen-equipped units capable of real-time inventory management and dynamic pricing [2]. The European Vending & Coffee Service Association reported that operator capital expenditure on connected hardware exceeded USD 1.4 billion across the EU in 2024 alone, a figure expected to double by 2030 as regulators push for digital payment mandates.

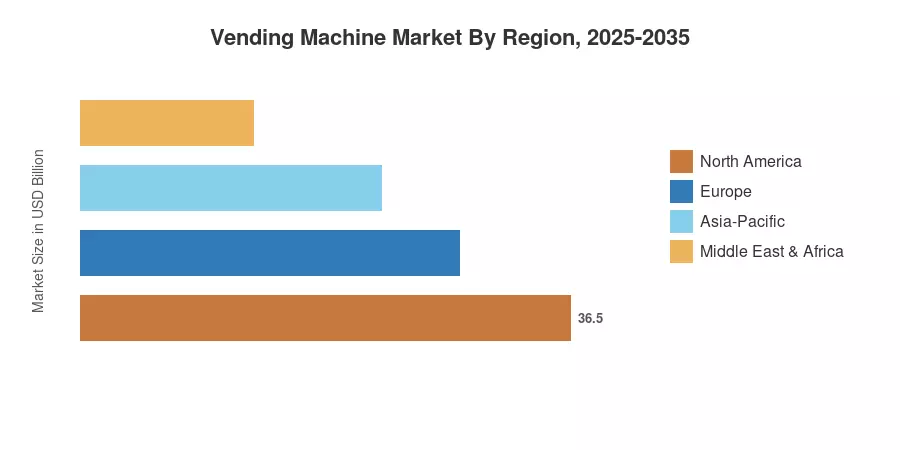

Asia-Pacific dominates the Vending Machine Market with approximately 38% of global revenue, driven by Japan's unmatched machine density of 1 unit per 23 people and China's rapid urban deployment [3]. North America holds the second-largest share at 28%, buoyed by micro-market conversions in corporate campuses. Europe trails at 22% but leads in sustainability-linked machine design. South America and the Middle East & Africa, though smaller at 7% and 5% respectively, represent the fastest expansion corridors outside Asia-Pacific, with urbanization rates above 3% annually fueling demand for automated retail touchpoints.

Key Report Takeaways

• By Product Type

- Beverage vending machines command 34% of the Vending Machine Market, underpinned by hot and cold-drink demand in offices and transit stations.

- Combination units are growing at a CAGR of 6.8%, the fastest among product categories, as operators consolidate SKU variety into single footprints.

- Specialty machines — including those dispensing electronics, PPE, and pharmaceuticals — generated USD 3.45 billion in 2025.

• By Technology

- Semi-automatic machines hold 42% market share but face displacement from smart connected units.

- Smart and connected vending is the Vending Machine Market's fastest-growing technology segment at 8.2% CAGR.

• By Region

- Asia-Pacific accounts for 38% of the Vending Machine Market, with Japan and China contributing over 70% of regional revenue.

- North America's market reached USD 6.03 billion in 2025.

- Middle East & Africa is forecast to grow at 7.1% CAGR, the highest among all regions.

Vending Machine Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up operator revenue aggregation, top-down macroeconomic modeling, and primary interviews with 120+ vending operators, OEMs, and payment-platform providers across 18 countries. Historical figures reflect audited company filings and trade-body statistics; forecast projections are calibrated against the 5.3% CAGR validated through comparable third-party benchmarks.