Vibration Monitoring Market Summary

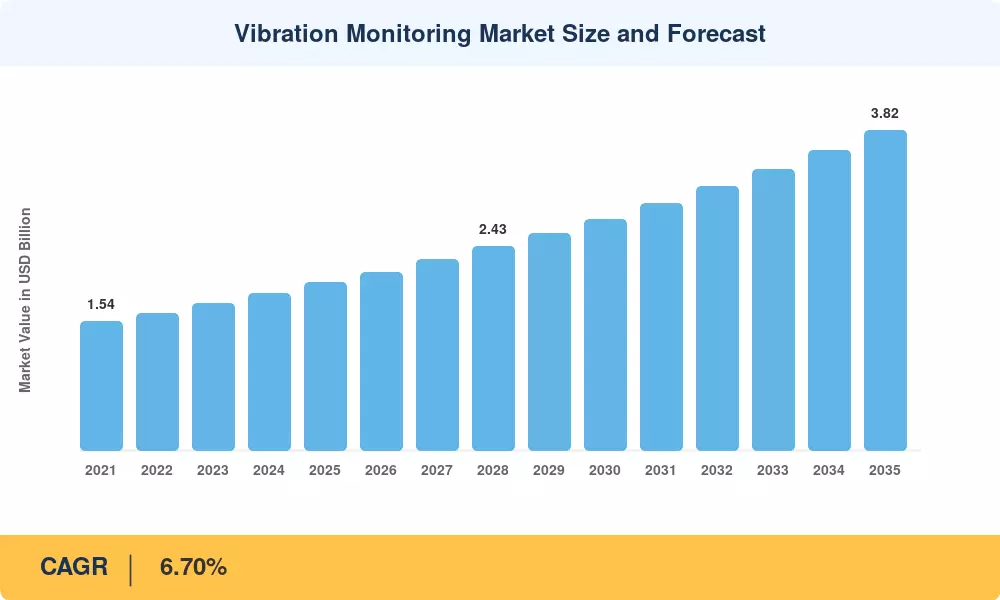

The Vibration Monitoring Market stood at USD 2.00 billion in 2025 and is projected to reach USD 2.13 billion by 2026, climbing to USD 3.82 billion by 2035 at a compound annual growth rate of 6.70% during the 2026–2035 forecast window. A decisive shift from reactive maintenance to condition-based strategies is propelling this expansion, with the U.S. Department of Energy estimating that predictive maintenance programs can reduce maintenance costs by 25–30% and eliminate 70–75% of equipment breakdowns across industrial facilities [1]. Unplanned downtime in heavy process industries now costs an estimated USD 50 billion annually worldwide, making real-time asset health intelligence a boardroom priority rather than a plant-floor luxury.

The technology backbone of the Vibration Monitoring Market is transforming rapidly. Legacy wired piezoelectric sensor networks — once the sole option for rotating-equipment diagnostics — are being supplemented and in many cases replaced by wireless IIoT sensor nodes with onboard edge analytics. Cloud-hosted platforms now ingest terabytes of vibration spectral data, run machine-learning models for anomaly detection, and push prescriptive alerts directly to mobile maintenance teams. According to the World Economic Forum, smart-factory investments exceeded USD 150 billion globally in 2024, with condition monitoring identified as a top-three deployment use case [2].

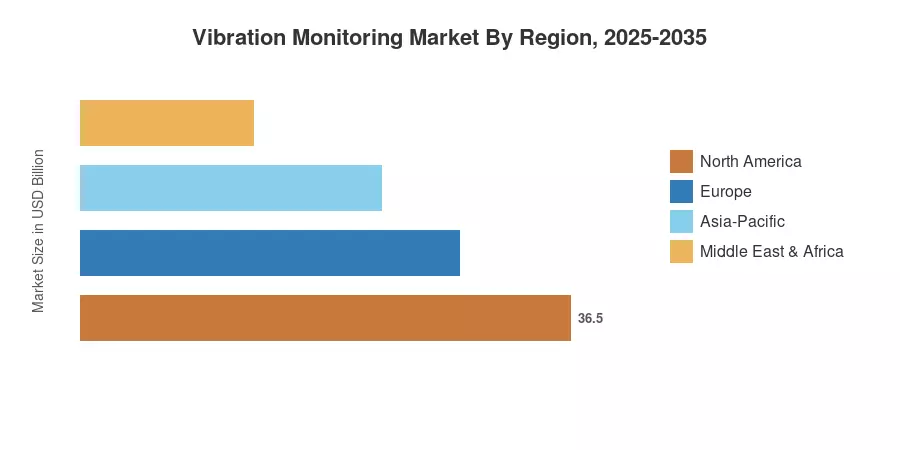

North America dominates the Vibration Monitoring Market with an estimated 39% revenue share in 2025, driven by the mature installed base in oil and gas and power generation. Asia-Pacific is the fastest-growing region at a projected 9.00% CAGR through 2035, fueled by government-backed Industry 4.0 programs in China and India. Europe holds the second-largest share at approximately 26%, supported by stringent EU Machinery Regulation compliance requirements. The next decade will reward vendors that can bridge legacy brownfield installations with scalable digital-twin ecosystems.

Key Report Takeaways

• By Component

- Hardware retained roughly 66% of the Vibration Monitoring Market share in 2025, reflecting continued demand for accelerometers, proximity probes, and velocity transducers across brownfield plants.

- Services posted the fastest segment CAGR at approximately 8.15% through 2035, as managed-monitoring contracts and remote diagnostics gain traction among asset-light operators.

• By Monitoring Process & Network Technology

- Online/continuous monitoring systems commanded an estimated 58% revenue share of the Vibration Monitoring Market in 2025, underscoring operator preference for always-on fault detection.

- Wireless network deployments are forecast to expand at a 10.95% CAGR between 2026 and 2035, narrowing the gap with entrenched wired installations.

• By Region

- North America accounted for roughly 39% of the Vibration Monitoring Market in 2025, anchored by deep oil-and-gas and power-generation spending.

- Asia-Pacific is projected to register the fastest regional CAGR of 9.00% from 2026 to 2035, driven by smart-manufacturing mandates and rapid industrialization.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates through triangulation of vendor financials, customs-trade databases, and end-user capital-expenditure disclosures. Forecast projections layer macroeconomic indicators, regulatory pipeline analysis, and technology-adoption curves validated through 45+ primary interviews with plant reliability engineers and procurement directors.