Video Encoder Market Summary

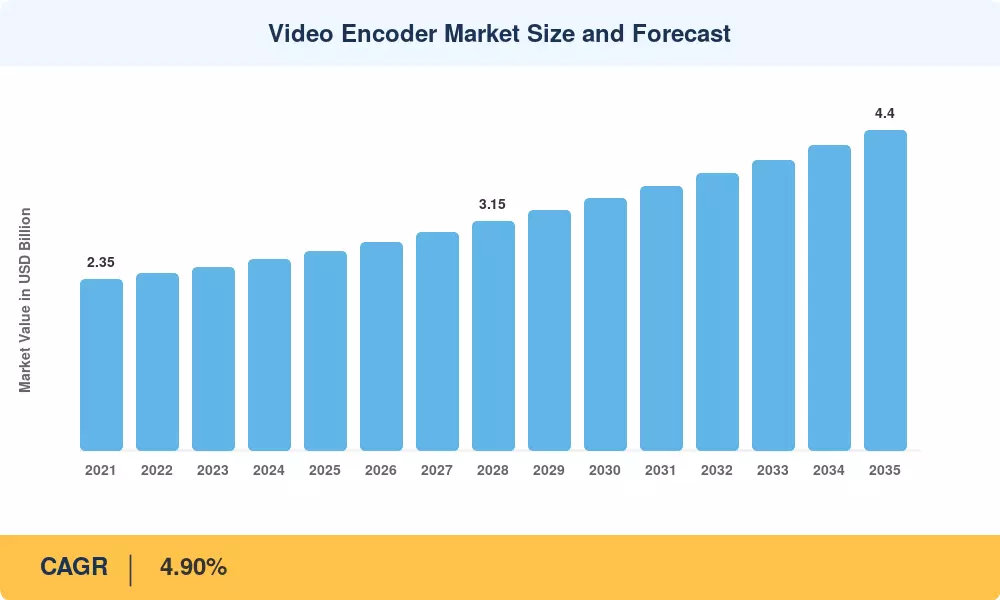

The Video Encoder Market stood at USD 2.73 billion in 2025 and is projected to reach USD 2.86 billion in 2026 before climbing to USD 4.40 billion by 2035, registering a 4.90% CAGR across the 2026–2035 forecast window. Two catalysts anchor this trajectory: the global push toward ATSC 3.0 next-generation broadcast standards and the explosion of over-the-top (OTT) video subscriptions, which surpassed 1.8 billion worldwide in 2024 [1]. Together, these forces compel operators and enterprises to upgrade encoding infrastructure on compressed timelines.

A sweeping technology transition defines the Video Encoder Market today. Legacy H.264/AVC appliances — workhorses of the 2010s — are giving way to H.265/HEVC, AV1, and emerging VVC/H.266 implementations that deliver comparable quality at 30–50% lower bitrates [2]. Cloud-native encoding platforms now attract significant venture-capital interest, with the broader cloud-video segment drawing over USD 4.2 billion in investment during 2023–2024 [3]. GPU-accelerated and FPGA-based transcoding pipelines are replacing fixed-function hardware in all but the most latency-sensitive broadcast chains.

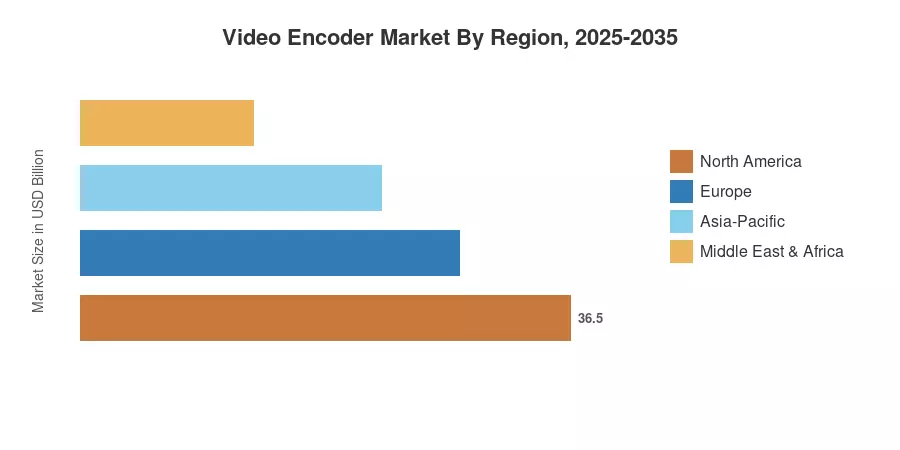

North America commands roughly 30.6% of the global Video Encoder Market revenue, anchored by the density of Tier-1 broadcasters and hyperscale cloud providers across the United States. Asia-Pacific registers the fastest regional CAGR at 5.65%, propelled by India's digital-video expansion and China's smart-city surveillance buildout. Europe holds the second-largest share at approximately 27.5%, driven by DVB-T2 migration mandates and sports-rights-driven encoding upgrades. The decade ahead will reward vendors that balance compression efficiency with deployment flexibility.

Key Report Takeaways

• By Encoder Type

- Hardware encoders held approximately 50.0% of the Video Encoder Market revenue in 2025, reflecting their entrenched role in mission-critical broadcast and contribution feeds.

- Cloud/SaaS encoding solutions are forecast to expand at a 6.35% CAGR through 2035, outpacing both hardware and on-premise software segments.

• By Encoding Standard

- H.264/AVC accounted for roughly 40.7% of the Video Encoder Market in 2025, though its share is declining as next-generation codecs mature.

- VVC/H.266 is projected to record the fastest codec-segment CAGR of 5.70% through 2035, driven by ultra-high-definition content requirements.

• By Application

- Pay-TV contributed an estimated 42.2% of Video Encoder Market application-level revenue in 2025, sustained by DTH and IPTV operator refresh cycles.

- OTT and live-streaming applications are advancing at a 5.10% CAGR, fueled by direct-to-consumer platform launches globally.

• By Region

- North America led the Video Encoder Market with 30.6% share in 2025, supported by hyperscaler infrastructure and ATSC 3.0 rollouts.

- Asia-Pacific is on track for the highest regional CAGR of 5.65% through 2035, underpinned by 5G deployments and rapid broadband penetration.

Video Encoder Market Size and Forecast (2021–2035)

Market Research Future's market-sizing model triangulates top-down revenue estimates from encoder OEM filings with bottom-up unit-shipment data across hardware, software, and cloud/SaaS categories. Historical figures (2021–2024) rely on audited annual reports and customs-trade databases; forecast values (2026–2035) incorporate demand-side modeling tied to OTT subscriber growth, broadcast-standard migration timelines, and enterprise video adoption curves.