White Box Server Market Summary

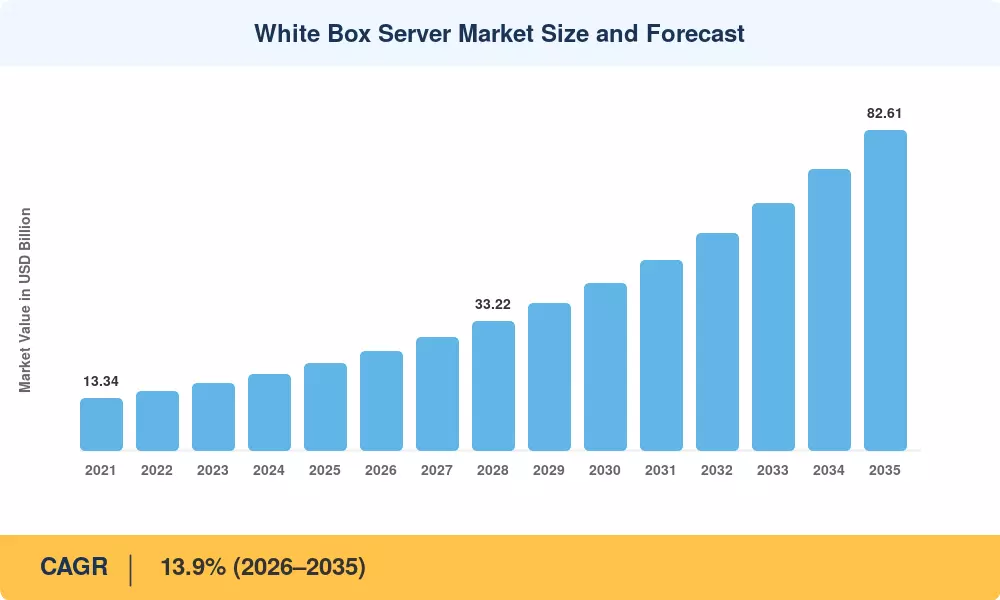

The White Box Server Market reached a valuation of USD 22.48 Billion in 2025 and is projected to grow from USD 25.61 Billion in 2026 to USD 82.61 Billion by 2035, registering a CAGR of 13.9% across the forecast window. Two catalysts are accelerating this trajectory: hyperscale cloud operators — led by Meta, Microsoft, and Google — are aggressively shifting procurement toward original design manufacturers (ODMs) to shave 20–30% off per-unit costs [1], while the explosion of GPU-dense AI training clusters is creating demand for purpose-built rack architectures that traditional OEMs struggle to deliver at speed [2].

A generational hardware shift is underway. Legacy branded servers, once the default for enterprise data centers, are giving way to modular, specification-driven platforms designed under the Open Compute Project (OCP) framework. The OCP ecosystem — encompassing over 300 contributing members and 400+ accepted designs — has standardized everything from power shelves to liquid-cooling manifolds, slashing integration timelines from months to weeks [3]. Global investment in data-center capacity exceeded USD 350 Billion in 2024 alone, with a substantial share allocated to bare-metal server hardware procurement [4].

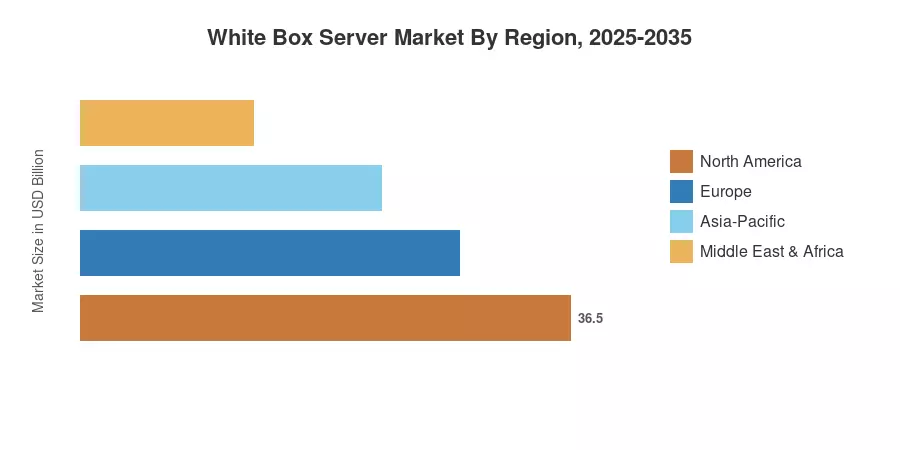

North America commands approximately 32.4% of the White Box Server Market, anchored by U.S. hyperscaler capital expenditure. Asia-Pacific is the fastest-growing region at an estimated CAGR of 16.3%, driven by Taiwan's ODM cluster and expanding cloud build-outs across India and Southeast Asia. Europe holds the second-largest share at roughly 24.8%, buoyed by EU digital-sovereignty mandates and growing colocation demand. As sovereign-cloud policies tighten and AI workloads diversify, the White Box Server Market is positioned for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Server Type

- Rack-mounted servers accounted for 38.6% of the White Box Server Market in 2025, reflecting their dominance in hyperscale and colocation deployments.

- GPU servers are forecast to register the fastest segment CAGR of 15.5% through 2035, propelled by generative-AI training and inference infrastructure.

• By Processor & Organization

- x86 architectures retained 85.2% of processor-type revenue in the White Box Server Market during 2025.

- Small and medium enterprises are expanding adoption at an estimated CAGR of 14.8%, narrowing the gap with large-enterprise buyers.

• By Region

- North America led the White Box Server Market with 32.4% share in 2025, driven by sustained hyperscaler CapEx.

- Asia-Pacific is projected to post the fastest regional CAGR of 16.3% through 2035.

White Box Server Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up ODM shipment tracking with top-down cloud CapEx modeling, triangulated against publicly disclosed hyperscaler procurement data and OCP contribution filings. Historical values (2021–2024) draw from audited financial disclosures of leading Taiwanese ODMs — Quanta Computer, Wistron/Wiwynn, and Inventec — while the forecast incorporates planned data-center build-outs announced by major cloud operators through 2035 [5].