Wind Turbine Rotor Blade Market Summary

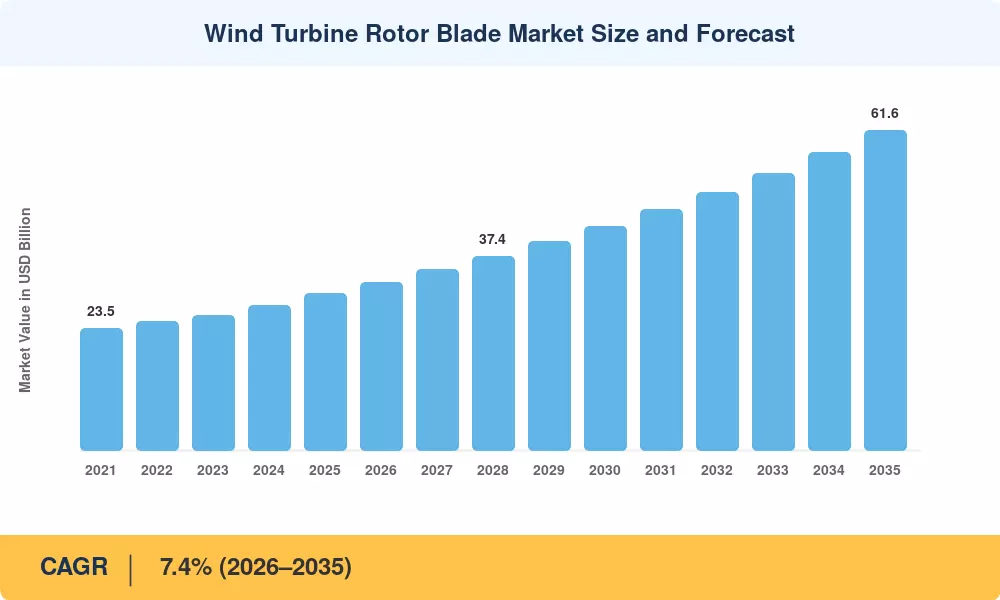

The global Wind Turbine Rotor Blade Market reached an estimated USD 30.2 billion in 2025 and is projected to grow from USD 32.4 billion in 2026 to USD 61.6 billion by 2035, registering a CAGR of 7.4% during the forecast period (2026–2035). This trajectory is anchored by aggressive national renewable energy targets — the European Union's binding commitment to 42.5% renewable energy by 2030 and China's pledge to install 1,200 GW of combined wind and solar capacity by the same year are funneling tens of billions into turbine procurement pipelines [1][2].

A generational shift in blade engineering is reshaping the supply chain. Turbines rated below 3 MW dominated onshore installations a decade ago; today, 6–8 MW platforms are standard onshore, and offshore machines exceeding 15 MW demand blades stretching beyond 115 meters. This scale-up is driving capital-intensive investments in new manufacturing tooling, automated layup systems, and thermoplastic resin research. Siemens Gamesa's RecyclableBlade program and LM Wind Power's commitment to zero-waste blade production by 2030 reflect an industry recalibrating around circular-economy principles [3][4].

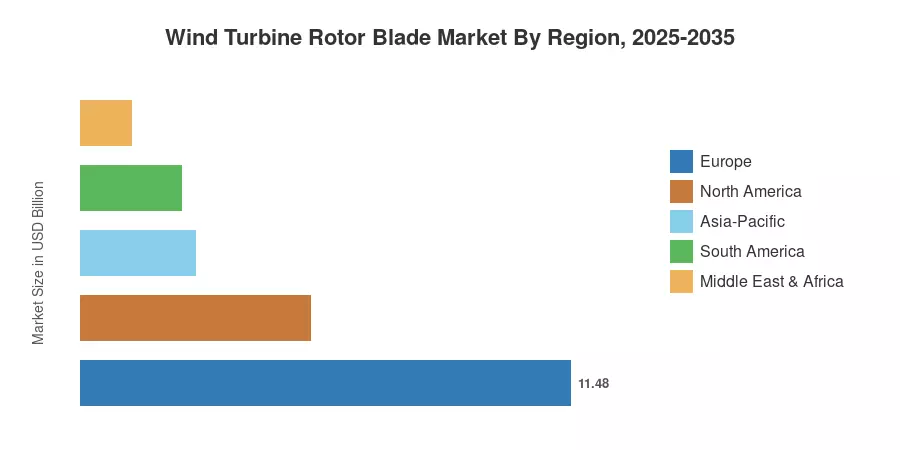

Europe commands the largest share of the Wind Turbine Rotor Blade Market at approximately 38%, buoyed by the North Sea offshore build-out and EU Innovation Fund disbursements. Asia-Pacific is the fastest-growing region with a projected CAGR of 8.9%, propelled by Chinese domestic manufacturing capacity and India's 500 GW non-fossil target for 2030. North America holds roughly 18% of global revenue, with the U.S. Inflation Reduction Act's production tax credits sustaining demand through the early 2030s [5][6]. The decade ahead will test whether blade supply chains can keep pace with turbine OEM order books that already extend three to four years out.

Key Report Takeaways

• By Material Type

- Glass fiber composites account for an estimated 62% of the Wind Turbine Rotor Blade Market by value, reflecting their cost-effectiveness for onshore applications under 80 meters.

- Carbon fiber composite blades are expanding at an estimated CAGR of 9.8%, driven by demand for stiffer, lighter structures in offshore turbines exceeding 12 MW.

- Hybrid fiber blades using selective carbon spar caps generated approximately USD 3.6 billion in 2025, balancing performance with material cost.

• By Application

- Onshore wind blades represent roughly 58% share of the Wind Turbine Rotor Blade Market, though growth is moderating as land-constrained markets saturate.

- Offshore wind blade demand is forecast to grow at a CAGR of 10.2%, supported by floating wind demonstration projects scaling toward commercial arrays.

• By Region

- Europe generated approximately USD 11.5 billion in blade revenue in 2025, maintaining the dominant regional position.

- Asia-Pacific is projected at a CAGR of 8.9% through 2035, the fastest among all regions.

- North America contributed roughly USD 5.4 billion in 2025, with production tax credits underpinning domestic blade manufacturing expansion.

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining turbine OEM shipment data, blade-per-turbine ratios by rated capacity, and average selling prices per meter of blade length. Historical figures (2021–2024) reflect confirmed installations reported by GWEC and national grid operators, while the 2025 base-year estimate incorporates Q1–Q3 actuals and Q4 order-book projections. Forecast values apply a 7.4% compound annual growth rate informed by announced pipeline capacity, policy visibility, and manufacturing expansion timelines.