Wood Vinegar Market Summary

The global Wood Vinegar Market reached a valuation of USD 5.98 Billion in 2025 and is projected to grow from USD 6.31 Billion in 2026 to USD 10.20 Billion by 2035, registering a CAGR of 5.48% across the forecast period (2026–2035). Escalating demand for bio-based agricultural inputs and tightening regulations against synthetic pesticides in the EU and across ASEAN member states are the principal catalysts propelling this trajectory. The EU's Farm to Fork Strategy, which mandates a 50% reduction in chemical pesticide use by 2030 [1], has spurred commercial-scale adoption of wood vinegar across European horticulture supply chains.

A major technological transition is taking place in the wood vinegar market with the replacement of legacy batch-kiln carbonization with continuous-flow pyrolysis reactors integrated with automated condensation and distillation modules. Between 2022 and 2024, Japan’s NEDO invested almost USD 45 million in next-generation pyrolysis infrastructure, with greatly increased recovery yields and product consistency [2]. These advancements are cutting per-liter production costs and providing pharmaceutical-grade purity that older systems could not.

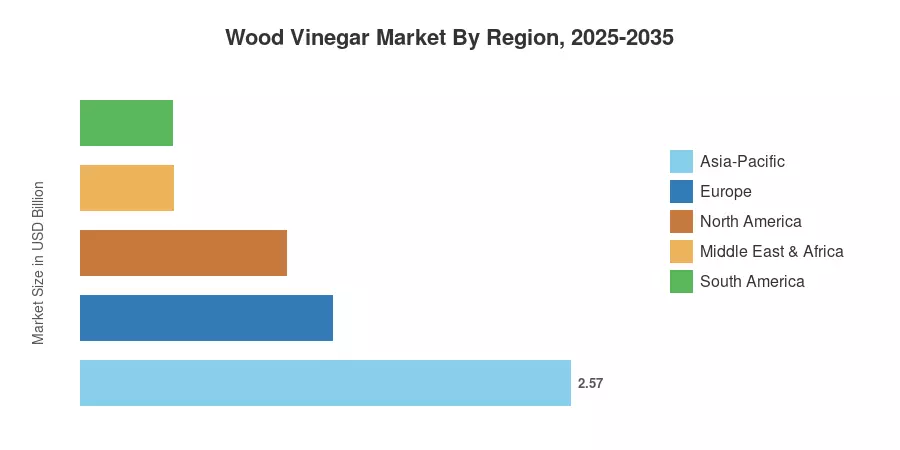

Asia-Pacific accounted for almost 43% of the worldwide Wood Vinegar Market revenue owing to well-established production clusters in China, Japan and Thailand. The Middle East & Africa is the fastest expanding region with a CAGR of 8.26% due to donor-funded sustainable-agriculture programs and soil-remediation projects. Europe has the second greatest proportion at around 22%, driven by organic farming subsidies and the adoption of precision agriculture. The Wood Vinegar Market prognosis is definitely optimistic as regulatory frameworks worldwide are increasingly favouring bio-based chemistry.

Key Report Takeaways

• By Production Method

- Slow pyrolysis held roughly 62% of the Wood Vinegar Market revenue in 2025, underpinned by its compatibility with small-scale and artisanal production facilities across Asia.

- Fast pyrolysis is forecast to expand at a 7.65% CAGR through 2035, driven by industrial-scale demand for higher throughput and consistent product quality.

• By Feedstock

- Hardwood feedstock accounted for approximately 30% of the Wood Vinegar Market in 2025, favored for its superior tar-separation characteristics.

- Coconut shell-derived wood vinegar is projected to grow at a 7.98% CAGR as tropical producers in Southeast Asia and West Africa scale capacity.

• By Application

- Agriculture commanded roughly 44% of the Wood Vinegar Market share in 2025, reflecting widespread use as a soil conditioner and pest deterrent.

- Pharmaceuticals are anticipated to register the fastest application-level growth at an 8.19% CAGR through 2035.

• By Geography

- Asia-Pacific generated approximately 43% of global Wood Vinegar Market revenues in 2025.

- The Middle East & Africa is advancing at an 8.26% CAGR, the fastest among all regions during the forecast window.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) report draws on a combination of bottom-up revenue modeling, trade-flow analysis across 42 countries, and primary interviews with more than 80 industry participants such as feedstock suppliers, pyrolysis equipment manufacturers, and end-use consumers. Historical values depend on customs data, corporate filings, and FAO trade statistics [3].