Apple Cider Vinegar Market Summary

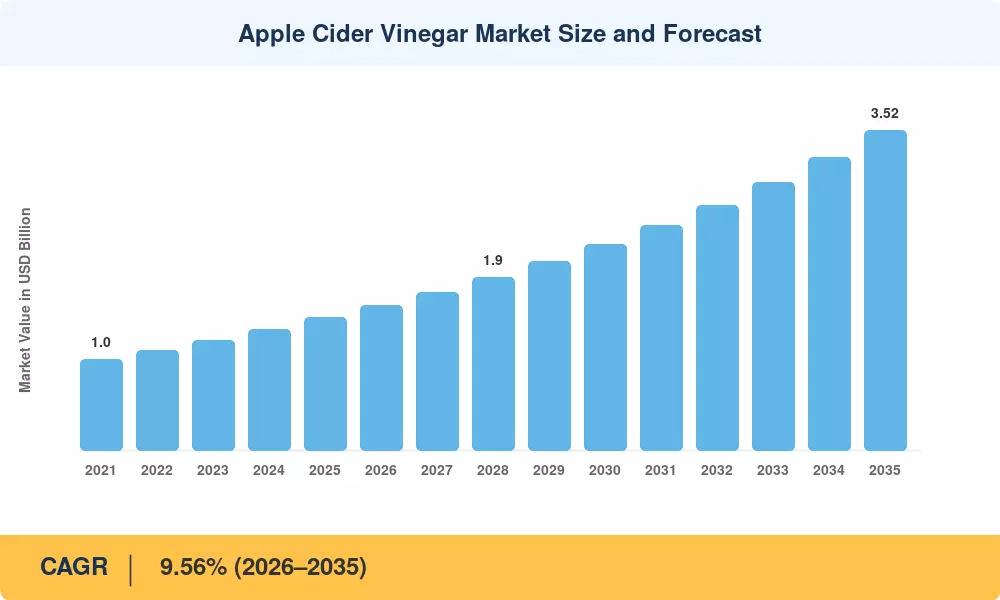

The Apple Cider Vinegar Market reached an estimated USD 1.46 billion in 2025 and is projected to grow from USD 1.60 billion in 2026 to USD 3.52 billion by 2035, registering a CAGR of 9.56% during the forecast period. This growth trajectory reflects a broader consumer pivot toward preventive health and clean-label pantry staples. USDA organic certification incentives — which expanded certified orchard acreage by 11% between 2022 and 2024 — have narrowed the retail price premium for organic apple cider vinegar to under 15%, accelerating mainstream adoption [2]. Meanwhile, functional food investment hit USD 28 billion globally in 2024, channeling capital toward raw, unfiltered ACV health products and fermented functional beverages.

Format Diversification is the fulcrum around which the Apple Cider Vinegar Market is pivoting. While the sector continues to be anchored in traditional liquid bottles, the apple cider vinegar supplement capsule segment and gummy forms are surmounting the taste barrier that has historically limited the targeted customer base. Capsule and tablet SKUs accounted for a 34% increase in shelf facings at major U.S. stores in 2024, with gummy launches tripling year-over-year. This tendency aligns with the broader nutraceutical trend, where older distribution techniques have been outperformed by convenient formats.

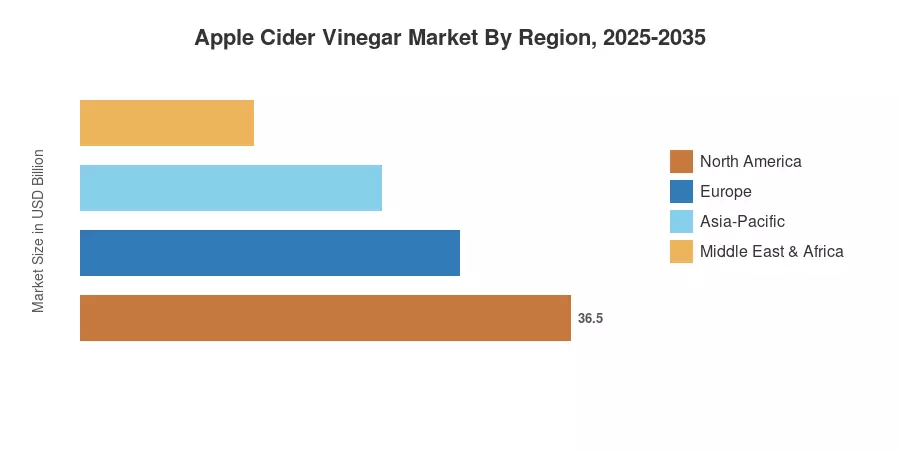

North America has over 36% of the Apple Cider Vinegar Market owing to its robust retail infrastructure and high consumer awareness of ACV weight control claims. Asia Pacific is the fastest-growing market with a projected CAGR of 11.14%, driven by increased disposable incomes in India and China and growing interest in ACV probiotic gut health applications. Europe accounts for the second greatest share at over 27%, driven by EU clean-label legislation and strong organic certification standards. The next growth chapter will be defined by geographic diversification into South America and the Middle East as the Apple Cider Vinegar Market matures in Western economies.

Key Report Takeaways

• By Form

- Liquid formats captured approximately 77% of the Apple Cider Vinegar Market revenue in 2025, reflecting entrenched consumer preference for raw, unfiltered ACV health uses in cooking and wellness routines

- The apple cider vinegar supplement capsule and tablet segment is forecast to grow at a 10.47% CAGR through 2035 — the fastest among all formats

• By Category

- Conventional products held a 72% share of the Apple Cider Vinegar Market in 2025

- Organic apple cider vinegar is expanding at a 10.86% CAGR, fueled by USDA incentive programs and narrowing price gaps

• By Distribution Channel

- Retail distribution contributed USD 1.08 billion in 2025, underscoring the dominance of supermarket and e-commerce channels

- Commercial applications — including foodservice and beauty — are growing at a 10.17% CAGR through 2035

• By Region

- North America led the Apple Cider Vinegar Market with 36% of global revenue in 2025

- Asia-Pacific is poised for an 11.14% CAGR through 2035, the fastest among all regions

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) follows a forecasting framework that includes bottom-up revenue modeling based on manufacturer shipments, validated with a top-down approach employing trade-flow data, retail scanner panel data, and proprietary distributor surveys in 42 countries. Historical numbers (2021-2024) are derived from reported revenues. 2025 is the calibrated base year. 2026-2035 values are anticipated based on segment-weighted compound growth rates adjusted for regulatory, macroeconomic and competitive considerations.