Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

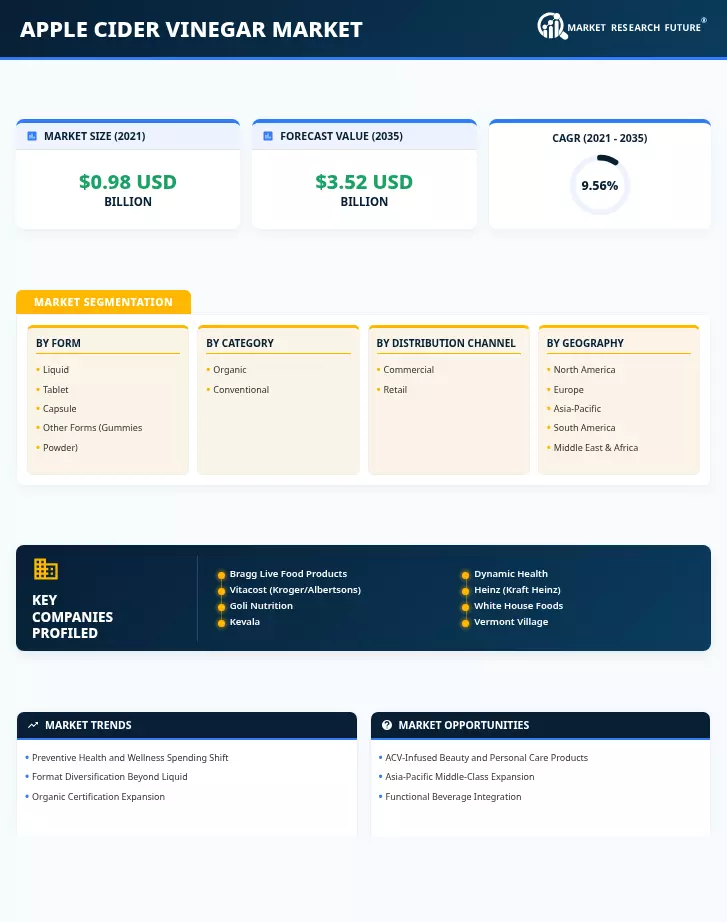

| By Form | Liquid, Tablet and Capsule; Other Forms (Gummies, Powder) | Liquid (77% share, 2025) | Tablet and Capsule (10.47% CAGR) |

| By Category | Organic; Conventional | Conventional (72% share, 2025) | Organic (10.86% CAGR) |

| By Distribution Channel | Commercial; Retail | Retail (USD 1.08 Billion, 2025) | Commercial (10.17% CAGR) |

| By Geography | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America (36% share, 2025) | Asia-Pacific (11.14% CAGR) |

Market Segmentation Overview

By Form

| Sub-Segment | Key Trend |

| Liquid | Dominant format driven by culinary versatility and raw, unfiltered ACV health rituals; premiumization via "with mother" variants |

| Tablet and Capsule | Fastest-growing format; removes taste barrier and aligns with supplement-aisle shopping behavior. |

| Other Forms (Gummies, Powder) | Rapid innovation cycle; gummy launches tripled year-over-year in 2024; appeals to younger demographics |

Liquid ACV retains the largest share due to its dual role in cooking and wellness routines. The tablet and capsule segment is attracting new consumer cohorts — particularly those purchasing apple cider vinegar supplement capsule products through pharmacy and online supplement channels — and is expected to narrow the format share gap over the forecast period.

By Category

| Sub-Segment | Key Trend |

| Conventional | Broad accessibility and private-label proliferation sustain volume leadership. |

| Organic | Accelerating adoption as USDA and EU certification incentives reduce price premiums; growing alignment with clean-label consumer expectations. |

Conventional ACV benefits from mass-market pricing and universal retail availability. Organic apple cider vinegar is the growth engine of this dimension, driven by structural policy tailwinds and consumer willingness-to-pay for certified clean-label products.

By Distribution Channel

| Sub-Segment | Key Trend |

| Retail | E-commerce penetration exceeds 31% of retail ACV sales in the US; omnichannel strategies accelerate. |

| Commercial | Expanding into foodservice, beauty contract manufacturing, and institutional cleaning applications |

Retail channels dominate revenue, but the commercial segment's higher-volume contracts and diversification into beauty and personal care applications represent the fastest-growing distribution pathway for the Apple Cider Vinegar Market through 2035.

By Region

| Sub-Segment | Key Trend |

| North America | Mature market with format innovation and D2C subscription models driving incremental growth. |

| Europe | EU organic mandates and clean-beauty crossover fuel steady expansion |

| Asia-Pacific | Fastest-growing region; middle-class demand in India and China, plus cultural alignment with fermented health traditions |

| South America | Early-stage market led by Brazil; import substitution encouraging local ACV production |

| Middle East & Africa | Halal certification and wellness tourism are creating new demand channels in the GCC. |

Asia-Pacific's rapid growth trajectory — underpinned by rising disposable incomes, e-commerce adoption, and cultural affinity for fermented foods — will progressively rebalance the Apple Cider Vinegar Market's geographic revenue mix over the next decade.