Wound Care Biologics Market Summary

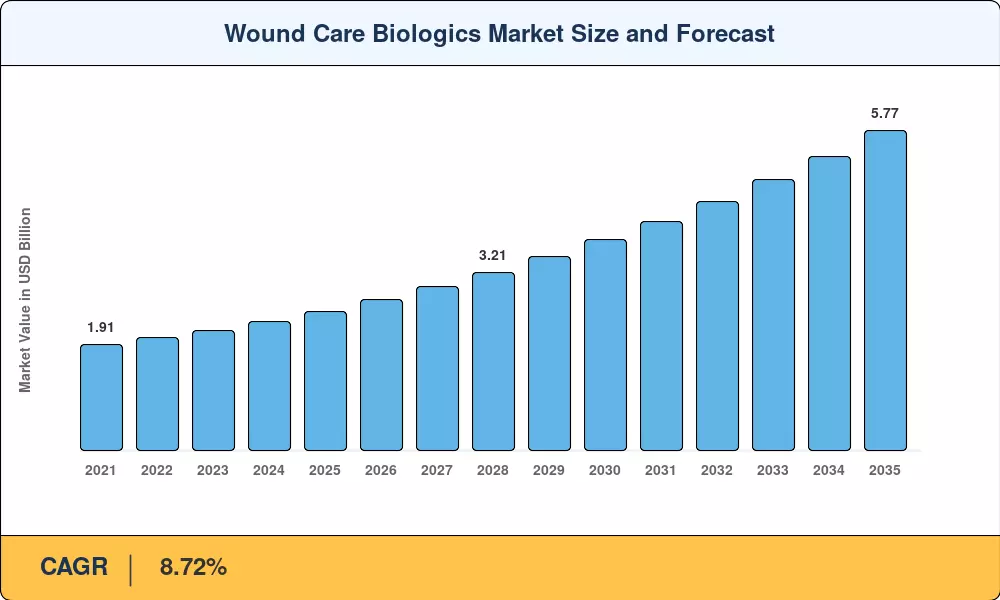

The Global Wound Care Biologics Market size was valued at USD 2.50 Billion in 2025, and the market is projected to grow from USD 2.72 Billion in 2026 to USD 5.77 Billion by 2035, registering a CAGR of 8.72% during the forecast period 2026–2035. Two policy catalysts anchor this trajectory: the Centers for Medicare & Medicaid Services (CMS) mandatory Local Coverage Determinations (LCDs) effective April 2025—requiring documented 50% wound-area reduction within four weeks before reimbursement approval—and the U.S. Department of Defense's USD 1.66 Billion Chemical and Biological Defense Program budget, which is accelerating trauma-biologic translation from battlefield to bedside [1][2].

The market for wound care biologics is undergoing a significant technological transition. Growth-factor-impregnated platforms, xenograft scaffolds, and biologic matrices are replacing traditional gauze-and-foam dressings because they have been shown to reduce the risk of secondary infection and speed up recovery. Manufacturers are being forced to incorporate resistance-mitigation capabilities into next-generation products due to the FDA's impending reclassification of antimicrobial dressings into more stringent device classes, which will increase R&D expenditures and performance standards [3].

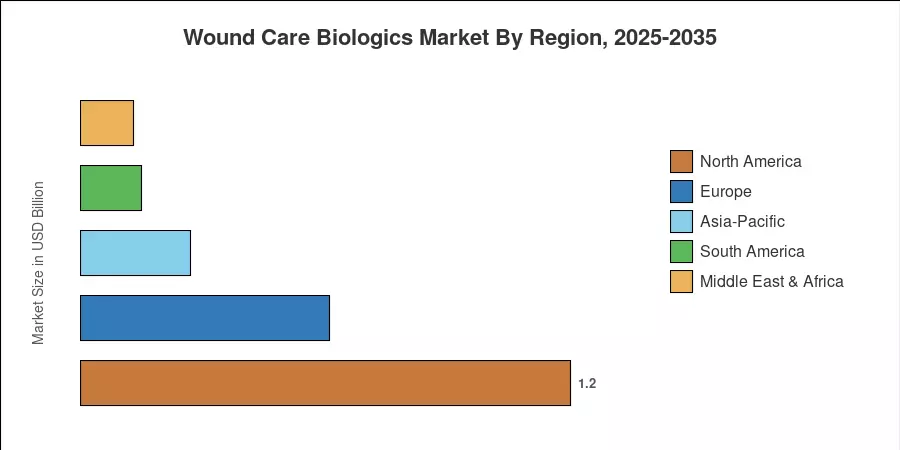

Due to high per-capita spending on wound care and widespread payer acceptance of biological wound healing therapies, North America accounted for approximately 47.9% of worldwide sales in 2025. The fastest-growing region is Asia-Pacific, which is expected to grow at a 10.63% CAGR through 2035 as surgery volumes and diabetes prevalence rise in China and India. Due to aging populations and advantageous CE-mark paths, Europe has the second-largest percentage, at about 24.5%. The global adoption of outcomes-based reimbursement models is expected to boost the wound care biologics market.

Key Report Takeaways

• By Product

- Biological skin substitutes—anchored by acellular dermal matrices—captured approximately 40.1% of the Wound Care Biologics Market share in 2025.

- Xenograft-based products are forecast to register a 11.05% CAGR through 2035, driven by expanded burn and diabetic-ulcer indications.

• By Wound Type

- Ulcers accounted for roughly 67.1% of total revenue in 2025, reflecting the global diabetes epidemic.

- Burn-related biologics are projected to grow at a 9.97% CAGR through 2035 as trauma-care protocols adopt biologic dressings.

• By End User & Distribution

- Hospitals and clinics represented approximately 69.4% of the Wound Care Biologics Market in 2025.

- Online distribution channels are expanding at a 10.36% CAGR, reshaping procurement for ambulatory surgical centers.

• By Region

- North America dominated with a 47.9% revenue share in 2025.

- Asia-Pacific is advancing at a 10.63% CAGR, the highest among all regions.

Market Size and Forecast (2021–2035)

Market sizing integrates bottom-up revenue analysis from product-line disclosures, payer reimbursement databases, and hospital procurement records, cross-validated against top-down macroeconomic indicators including chronic-wound prevalence rates and surgical-procedure volumes. Historical data covers 2021–2024; 2025 is the base year; 2026–2035 is the forecast window.

.webp?v=1782120130)