Zero Liquid Discharge Market Summary

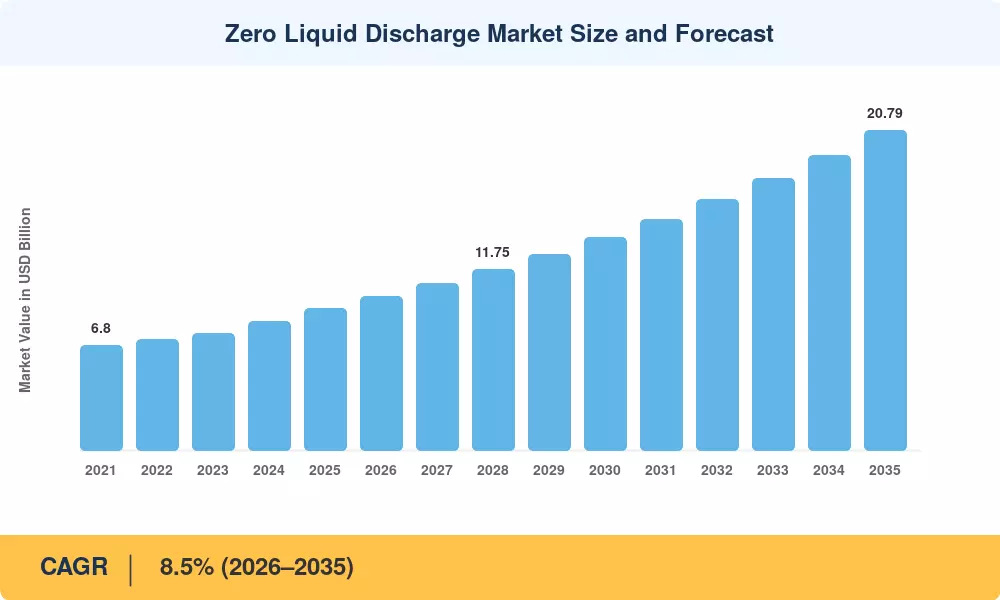

The Zero Liquid Discharge Market reached an estimated USD 9.20 billion in 2025 and is projected to grow from USD 9.98 billion in 2026 to USD 20.79 billion by 2035, registering a CAGR of 8.5% during the forecast period (2026–2035). This expansion is anchored in tightening effluent discharge regulations across both developed and developing economies. The U.S. EPA's 2024 revisions to the Effluent Limitations Guidelines for the Steam Electric Power Generating category, which impose stricter limits on flue gas desulfurization wastewater, have pushed utilities toward full-scale ZLD adoption [1]. Concurrently, China's 14th Five-Year Plan earmarked over USD 12 billion for industrial water recycling infrastructure, creating a significant demand corridor for ZLD systems across coal-fired power plants and chemical parks [2].

The Zero Liquid Discharge Technology movement in the market is changing. Traditional thermal-only treatment trains (brine concentrators, forced-circulation crystallizers) are being replaced by hybrid architectures combining high-recovery reverse osmosis with tiny thermal back-ends. This change reduces energy usage by 40-60% per cubic meter of treated effluent, making ZLD economically viable for mid-sized plants that had relied on conventional evaporation ponds [3]. Membrane distillation and forward osmosis pilot efforts, in part supported through a USD 45 million DOE Water Security Grand Challenge, are speeding this shift [4].

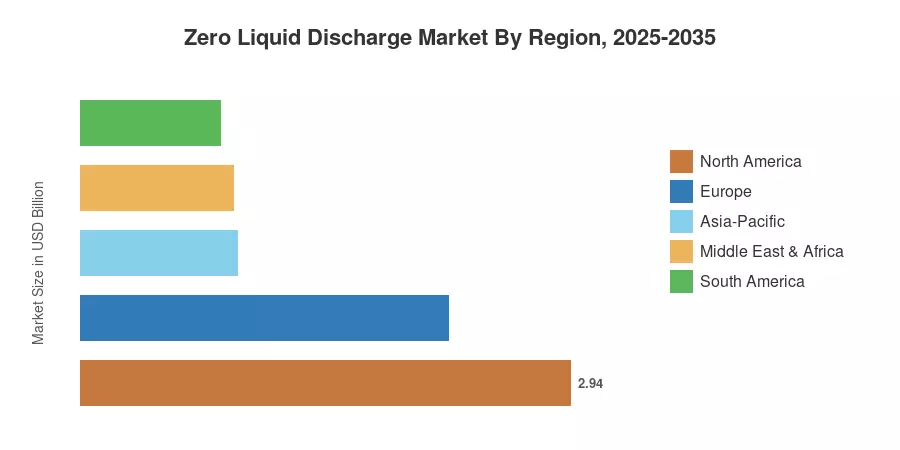

North America holds the greatest part of the Zero Liquid Discharge Market, accounting for almost 32% of 2025 revenue, driven by tough regulations in the power industry and compliance schedules for aging coal plants. Asia-Pacific is the fastest developing market with a predicted CAGR of 10.2%, driven by requirements from India’s Central Pollution Control Board and the proliferation of zero-discharge industrial parks in China. Europe follows with about 24%, driven by changes in the pharmaceutical and chemical sectors under the EU Industrial Emissions Directive [5]. “As water scarcity increases globally, the Zero Liquid Discharge Market is expected to continue to grow in double digits across various industrial verticals by 2035.

Key Report Takeaways

• By Technology

- Thermal-based systems (evaporators and crystallizers) account for approximately 55% of the Zero Liquid Discharge Market, benefiting from proven reliability in high-salinity applications.

- Membrane-based ZLD technologies are growing at a CAGR of 11.3%, driven by energy-efficiency gains and falling membrane costs.

- Hybrid systems combining membrane pre-concentration with thermal polishing generated approximately USD 1.38 billion in 2025.

• By End-Use Industry

- Power generation represents the dominant end-use sector with a 28% share of the Zero Liquid Discharge Market, largely driven by coal-plant wastewater compliance mandates.

- The textile industry is the fastest-growing end-use vertical at a CAGR of 10.8%, led by India's Common Effluent Treatment Plant mandates.

- Chemical and petrochemical facilities collectively contributed USD 2.02 billion in 2025 revenue.

• By Geography

- North America held the leading share of 32% of the Zero Liquid Discharge Market in 2025.

- Asia-Pacific is forecast to grow at a CAGR of 10.2% through 2035, the fastest among all regions.

- Europe's Zero Liquid Discharge Market is anchored by pharmaceutical and chemical sector compliance requirements.

Zero Liquid Discharge Market Size and Forecast (2021–2035)

The market sizing model uses bottom-up project-level data from over 200 ZLD installations internationally, cross-validated with top-down industry capacity reports, regulatory compliance timeframes and published capital expenditure disclosures from key EPC contractors. Historical numbers are based on actual market activity (2021-2024), with 2025 as the base year based on validated pipeline analysis. The 8.5% CAGR is held constant in forecast estimates (2026-2035) with adjustments for anticipated regulatory acceleration in key geographies.