ナレッジマネジメントソフトウェア市場 概要

MRFRの分析によると、ナレッジマネジメントソフトウェア市場の規模は2024年に301億米ドルと推定されました。ナレッジマネジメントソフトウェア業界は、2025年に335億米ドルから2035年には977.3億米ドルに成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は11.3%となる見込みです。

主要な市場動向とハイライト

知識管理ソフトウェア市場は、技術の進歩と進化するユーザーのニーズにより、堅調な成長を遂げています。

- "人工知能の統合は、知識管理システムの運用を変革し、効率性とユーザーエンゲージメントを向上させています。

- ユーザーエクスペリエンスは重要な焦点となり、企業は採用率を向上させるために直感的なインターフェースを優先しています。

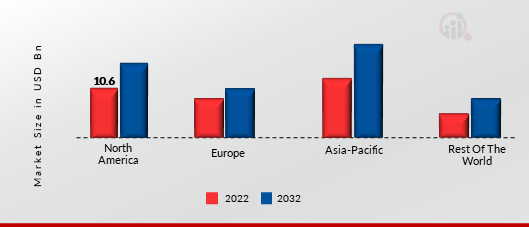

- 北米は依然として最大の市場であり、アジア太平洋地域は知識管理ソリューションの最も成長が早い地域として浮上しています。

- リモートコラボレーションの需要の増加とデータ駆動型意思決定の重要性の高まりが、市場を前進させる主要な要因です。"

市場規模と予測

| 2024 Market Size | 30.1 (USD十億) |

| 2035 Market Size | 97.73 (USD十億) |

| CAGR (2025 - 2035) | 11.3% |

主要なプレーヤー

マイクロソフト(米国)、IBM(米国)、SAP(ドイツ)、オラクル(米国)、アトラシアン(オーストラリア)、ミロ(米国)、サービスナウ(米国)、ゾーホー(インド)、コンフルエンス(米国)