Knowledge Management Software Market Summary

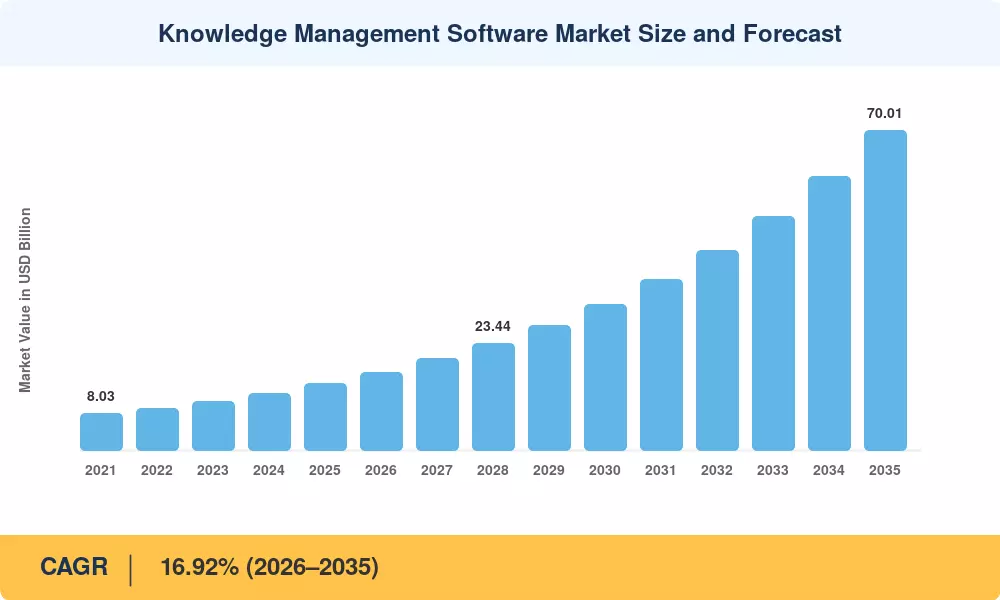

The Knowledge Management Software Market reached an estimated USD 14.56 billion in 2025 and is projected to grow from USD 17.15 billion in 2026 to USD 70.01 billion by 2035, registering a CAGR of 16.92% across the forecast period. Two forces are converging to drive this expansion: enterprise-wide mandates to retain institutional expertise amid workforce turnover, and governments tightening data governance standards — the EU's Data Governance Act and the U.S. Executive Order on AI (October 2023) both compel organizations to formalize how intellectual assets are captured, stored, and retrieved [1][2]. Combined, these catalysts are pushing annual corporate spending on knowledge infrastructure past traditional IT budget thresholds.

Legacy intranets and static document repositories are being dismantled in favor of AI-augmented platforms that integrate retrieval-augmented generation, semantic search, and automated taxonomy creation. Microsoft alone channeled over USD 13 billion into OpenAI partnerships through 2024, embedding generative capabilities directly into SharePoint and Viva [3]. IBM's watsonx platform and ServiceNow's Now Assist similarly reflect a vendor race to fuse large language models with enterprise knowledge sharing systems, converting passive content libraries into dynamic decision-support engines.

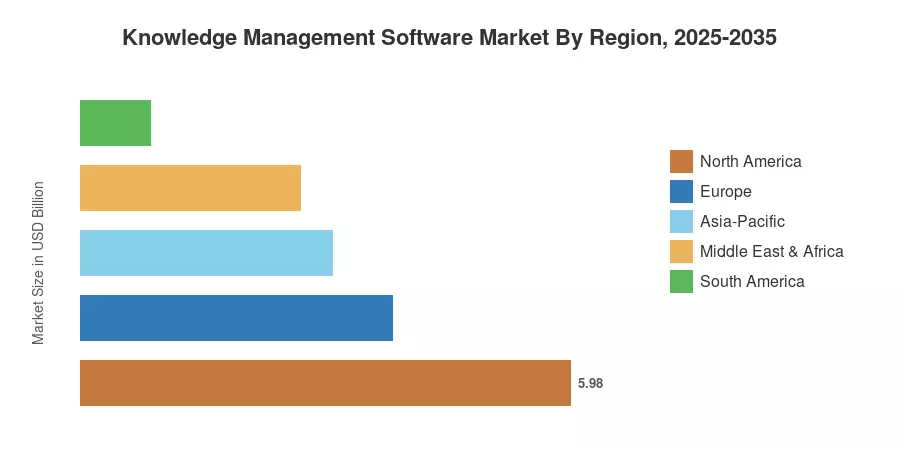

North America commands approximately 41.05% of the Knowledge Management Software Market, underpinned by early cloud adoption and a dense SaaS vendor ecosystem. Asia-Pacific is the fastest-growing region at a 21.15% CAGR, fueled by India's Digital India program and China's push for indigenous AI-driven enterprise platforms. Europe holds the second-largest share at 26.18%, driven by GDPR-adjacent compliance requirements that elevate the role of structured knowledge governance. As generative AI matures, the Knowledge Management Software Market is positioned to become a foundational layer of enterprise digital infrastructure through 2035.

Key Report Takeaways

• By Functionality

- Document management captured 35.48% of the Knowledge Management Software Market in 2025, reflecting its role as the default entry point for enterprise knowledge infrastructure.

- Intelligent chatbots and virtual agents are expanding at a 20.12% CAGR through 2035, driven by enterprises deploying conversational AI for real-time knowledge retrieval.

• By Deployment

- Cloud-based deployments dominate the Knowledge Management Software Market with an 18.10% CAGR, as organizations migrate from on-premises silos to scalable, API-driven platforms.

• By Organization Size

- SMEs are growing at a 17.50% CAGR, closing the adoption gap with large enterprises as low-code knowledge platforms reduce implementation barriers.

• By Region

- North America accounted for USD 5.98 billion in 2025, with the United States driving over three-quarters of regional revenue.

- Asia-Pacific is advancing at a 21.15% CAGR, the fastest of any region, as digital transformation programs across India, China, and ASEAN accelerate enterprise software adoption.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework combines bottom-up vendor revenue analysis with top-down macroeconomic modeling. Historical figures (2021–2024) are derived from audited financial disclosures, while forecast values (2026–2035) incorporate technology adoption curves, regulatory impact assessments, and enterprise IT spending projections sourced from national statistical agencies [4][5].