医療エステ市場の概要

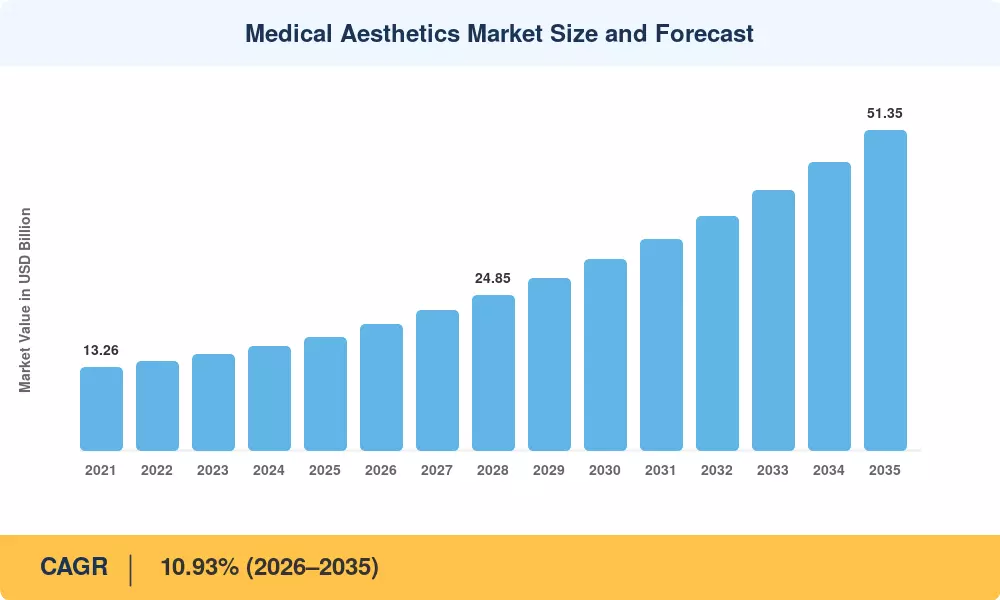

医療エステティック市場は2025年に182億米ドルに達し、2026年の201億9000万米ドルから2035年までに513億5000万米ドルに成長すると予測されており、予測期間(2026年から2035年)中に10.93%のCAGRを記録します。低侵襲のボディスカルプティングおよび肌の若返り処置に対する需要の高まりと、米国 FDA および欧州の CE マーキングの枠組みによる規制の合理化が相まって、永続的な成長滑走路が生まれました。アジアのいくつかの経済圏における政府の健康保険の拡大により、選択的治療への患者のアクセスがさらに拡大しています。

テクノロジーの変革により、医療美容市場はその中核から再構築されています。従来の単機能レーザー プラットフォームは、高周波、高密度焦点式超音波 (HIFU)、およびパルス光モダリティを 1 台のコンソールで組み合わせたマルチモーダル エネルギー システムに取って代わられています。アッヴィだけでも、2023年から2025年にかけて推定12億米ドルを美学の研究開発に注ぎ込み、AI誘導の治療計画ソフトウェアにより、医師はエネルギー供給プロトコルをリアルタイムでカスタマイズできるようになりました。[2]。これらの変化により、処置時間が短縮され、対象となる患者集団が従来の人口統計を超えて拡大しています。

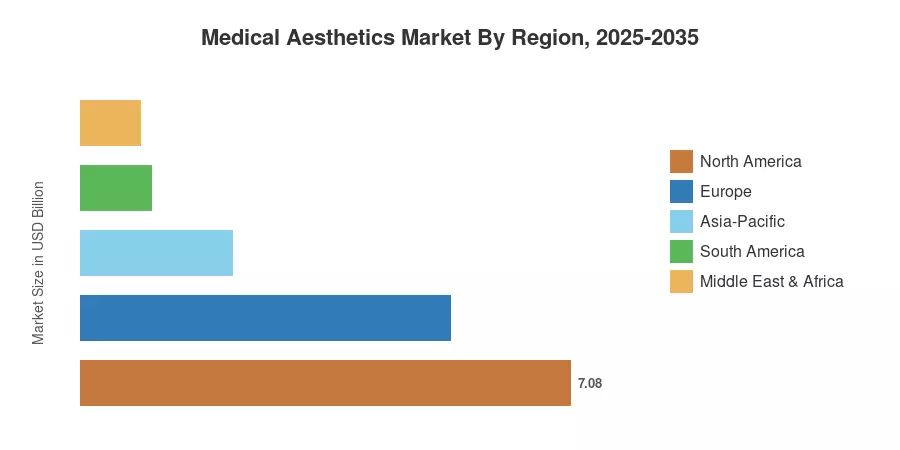

北米は、選択的処置と成熟した償還経路に対する一人当たりの高い支出に支えられ、2025年に世界の医療美容市場の収益の約38.9%を占めました。アジア太平洋地域は最も急速に成長している地域であり、中国とインドにおける中間層人口の拡大により、2035 年まで 12.01% の CAGR で成長すると予測されています。ヨーロッパは、強力な臨床基準と国境を越えた医療ツーリズムに支えられ、約 29.4% で 2 番目に大きなシェアを占めました。デバイスの革新、規制の調和、予防的な美学に対する消費者の態度の変化が融合し、この市場は今後 10 年間にわたって継続的に 2 桁の拡大を遂げる見通しです。

レポートの重要なポイント

• デバイスタイプ別

- エネルギーベースの美容機器は、2025 年の医療美容市場の収益の 48.5% を占め、これは臨床現場におけるレーザー、高周波、超音波プラットフォームの優位性を反映しています。

- 注射剤やインプラント システムを含む非エネルギー ベースのデバイスは、次世代生物製剤の勢いが増すにつれて、2035 年までに 13.24% の CAGR で成長すると予想されており、エネルギー ベースのセグメントを上回ります。

• 手続きの種類別

- 2025 年には非外科的かつ低侵襲治療が支出の 51.2% を占め、回復期間が短い治療法を消費者が好むことが明らかになりました。

- 脂肪移植技術とハイブリッド手術エネルギーワークフローの革新により、外科手術は 2035 年まで 13.55% CAGR で拡大すると予測されています。

• アプリケーション別

- フェイシャルエステティックは、2025 年の医療エステティック市場の収益の 25.4% を占め、依然として世界最大のアプリケーションセグメントです。

- ボディ輪郭加工は、2035 年までに 14.35% の CAGR を達成すると予測されており、これはアプリケーションのサブセグメントの中で最高です。

• エンドユーザーによる

- クリニックと皮膚科は、2025 年に医療美容市場で 42.8% のシェアを占め、エネルギーベースの治療と注射による治療の両方の主要なケアポイントとして機能しました。

- 医療スパは、美的健康の主流化に後押しされて、2035 年まで 14.41% の CAGR で拡大すると予想されています。

• 地域別

- 2025 年には北米が世界収益の 38.9% を占めて首位となり、アジア太平洋地域は 2035 年までに 12.01% の CAGR が見込まれています。

医療エステティック市場規模と予測(2021年~2035年)

Market Research Future の推定値は、機器メーカー、診療所運営者、規制当局への一次インタビューに基づいて導き出され、販売代理店のセルスルー データおよび公的に提出された財務結果と照らし合わせて三角測量されています。過去の値 (2021 ~ 2024 年) は報告された市場パフォーマンスを反映しています。 2025 年が基準年です。 2026 ~ 2035 年の値は、CAGR 10.93% での将来予測です。

ドライバーの影響分析

| ドライバ |

CAGR に対する ~% の影響 |

地理的な関連性 |

影響のタイムライン |

参照 |

| 先進国における人口動態の高齢化 |

~18% |

北米、ヨーロッパ |

長期(4年以上) |

[3] |

| ソーシャルメディアによる手順の認識 |

~16% |

グローバル |

短期(2年以内) |

[5] |

| デバイスにおける AI とロボティクスの統合 |

~15% |

北米、アジア太平洋 |

中期(2~4年) |

[6] |

| アジア太平洋地域における可処分所得の増加 |

~14% |

中国、インド、ASEAN |

長期(4年以上) |

[7] |

| 低侵襲デバイスの規制の迅速な追跡 |

~13% |

米国、欧州 |

短期(2年以内) |

[4] |

| メディカルスパおよびウェルネスチャネルの拡大 |

~12% |

グローバル |

中期(2~4年) |

[10] |

| 生体刺激および再生注射剤のイノベーション |

~12% |

北米、ヨーロッパ |

中期(2~4年) |

[8] |

先進国における人口動態の高齢化

国連は、60歳以上の成人が2050年までに世界で21億人を超えると予測しており、最も急激に増加するのは北米、西ヨーロッパ、北東アジアに集中するという。[3]。この人口動態の変化は、しわの軽減、肌の引き締め、ボリュームの回復などの処置に対する需要を直接的に増加させます。米国だけでも、米国形成外科医協会は、2024 年に 2,600 万件以上の美容処置が行われたと報告しており、これは前年比 12% 増加で、45 ~ 65 歳の層に集中しています。[4]。持続的な人口高齢化傾向により、これが医療美容市場の唯一の最も耐久性のある構造的推進力となっています。

ソーシャルメディアを活用した手続きの認識

Instagram や TikTok などのプラットフォームは、歴史的に治療を先延ばしにしていた 25 ~ 40 歳の消費者の間で審美的な手順を標準化しました。 ASAPS の調査では、2024 年の初診患者の 72% が主な情報源としてソーシャル メディア コンテンツを挙げていることが判明しました。[5]。この可視化効果により意思決定サイクルが短縮され、数カ月ではなく数週間以内に認知度が予約に変わり、スマートフォンの普及率が高い地域の医療美容市場に不釣り合いな利益をもたらします。

デバイスにおける AI とロボティクスの統合

AI ガイドによる治療プロトコルにより、医師はリアルタイムで組織密度をマッピングし、エネルギー出力を動的に調整して熱損傷を最小限に抑え、コラーゲンのリモデリングを最大化できるようになりました。 Canfield Scientific の AI 画像プラットフォームは、2025 年までに 4,000 の診療所で採用され、治療計画にかかる時間を推定 35% 短縮しました[6]。ロボットマイクロニードルシステムと自動注射ガイドモジュールは市場前レビューに入っており、医療美容市場の対象人口を拡大できる精密ガイド付き美容への移行を示唆しています。

アジア太平洋地域における可処分所得の増加

中国の都市部世帯の可処分所得は、2021年から2025年の間に年間6.8%の伸び率で増加し、美容処置への支出はその約2倍に増加した[7]。インドの急成長する医療観光インフラと韓国の確立されたK-ビューティーエコシステムがその効果をさらに高め、アジア太平洋地域が医療エステティック市場への最も急速に成長する貢献国となっています。インドのアユシュマン・バーラト計画などの政府の取り組みは、基本的なケアに主に焦点を当てている一方で、選択的処置をサポートする民間クリニックのインフラを間接的に拡大している。[7].

拘束影響分析

以下の抑制の影響は、市場の成長を鈍化させる逆風の方向性を推定したものです。これらは CAGR から直接差し引かれるものではありませんが、対処しないと勢いが鈍化する可能性がある領域を示しています。

| 拘束 |

CAGR の ~% のドラッグ |

地理的な関連性 |

影響のタイムライン |

参照 |

| 規制の複雑さとデバイスの承認スケジュール |

~−8% |

EU、アジア太平洋 |

中期(2~4年) |

[9] |

| マルチモーダル プラットフォームの高額な初期資本コスト |

~−7% |

新興市場 |

長期(4年以上) |

[13] |

| 有害事象のリスクと責任に関する懸念 |

~−6% |

北米 |

短期(2年以内) |

[14] |

| 選択的処置の償還制限 |

~−5% |

グローバル |

長期(4年以上) |

[15] |

| 熟練した施術者が不足している |

~−4% |

MEA、南アメリカ |

中期(2~4年) |

[16] |

規制の複雑さとデバイスの承認スケジュール

2024 年から完全施行された EU 医療機器規制 (MDR 2017/745) により、中小規模の機器メーカーの認証コストが 40 ~ 60% 増加し、いくつかのカテゴリーで製品の発売が 12 ~ 18 か月遅れました。[9]。企業は現在、継続的な市販後臨床追跡調査(PMCF)研究を維持する必要があり、定期的なコンプライアンス費用が追加され、利益率が圧縮されています。医療美容市場にとって、これにより、米国の認可を受けたデバイスが EU 認定の同等のデバイスよりも何年も早くクリニックに届くという 2 つのスピードの世界が生まれます。

高額な初期資本コスト

完全に構築されたマルチモーダル エネルギー プラットフォームのコストは 150,000 ~ 300,000 米ドルであり、低所得市場の独立開業医にとっては手頃な価格ではありません。[13]。リースや手続きごとの支払いモデルが登場していますが、同じように利用できるわけではありません。メディカルエステティック市場への浸透は、資金調達ソリューションが開発されるまで、ラテンアメリカ、東南アジア、中東の一部における資本集中によって引き続き制約されるだろう。

有害事象のリスクと責任の懸念

2024 年に、FDA はヒアルロン酸フィラーの誤った注射に関連する組織壊死に関する最新の安全性通知を発表し、その結果、開業医の賠償責任保険費用が 15 ~ 20% 増加すると予測されました。[14]。統計的には、安全性に関するイベントはまだまれですが、メディアの誇張された注目は影響を受けた国での消費者の受け入れを遅らせ、医療エステティック市場の成長軌道に摩擦を加える可能性があります。

医療美容市場の機会

AI を活用した治療のパーソナライゼーション

現在では、何百万もの手術結果に基づいてトレーニングされた機械学習アルゴリズムにより、各肌タイプに最適なエネルギー設定、注入深さ、製品の組み合わせを提供できるようになりました。早期導入者は、患者満足度スコアが 20 ~ 25% 向上し、再治療率が低下したと報告しており、医療美容市場内にプレミアム サービス層を生み出しています。[6].

再生美学と生物学的製剤

エキソソームと多血小板血漿 (PRP) 補助療法の応用は、実験段階から商業段階に移行しています。 2025 年には、世界の再生医療パイプラインでは 1,400 以上の研究が活発に行われており、美容用途が急速に成長している分野となっています。[12]。生物製剤送達モジュールを現在のプラットフォームに組み込んだデバイスメーカーは、この隣接する成長領域で先行者利益を得ることができます。

新興市場のクリニックインフラ

インドとブラジルを合わせると、都市化と意欲的な支出の増加により、2026年から2030年の間に認可された美容クリニックが12,000以上追加されると見込まれています。[7]。機器リース モデルと販売代理店との融資提携により参入障壁が低くなり、医療エステティック市場での量的拡大を目指す中堅デバイス OEM にとってこれらの市場へのアクセスが可能になります。

接続されたデバイスによるデータの収益化

クラウドに接続されたエステティック プラットフォームは、臨床トレーニング プラットフォーム、保険引受会社、製薬研究開発チームにとって商業的価値を持つ匿名化された処置結果データセットを生成します。サブスクリプションベースのデータ分析サービスは、2030 年までに年間 8 億~12 億米ドルの経常収益に貢献する可能性があります[17].

男性のエステティック手順

2025年には世界のすべての美容処置のうち男性が占める割合は推定14%となり、2020年の9%から増加すると予想されています。[5]。体の輪郭を整える治療や顎のラインを整える治療がこの変化を主導しています。男性患者を対象としたマーケティング プログラムや治療プロトコルを開発するデバイス メーカーは、医療審美市場での増加量を開拓できます。

エステティック医療市場の将来展望

AI 自律型治療エコシステム

2030 年までに、完全自律型の治療計画システムが、患者吸入イメージングからエネルギー供給校正、処置後のモニタリングに至るまで、エンドツーエンドのワークフローを管理し、医師の意思決定の疲労を軽減し、診療所あたりのスループットの向上を可能にすることが期待されています。 AI を活用した臨床ワークフローにより、医療美容市場全体で処置ごとのコストが 20 ~ 30% 削減され、より幅広い層がプレミアムな治療を受けられるようになる可能性があると推定されています。[6].

プラットフォームの経済性とサブスクリプション モデル

デバイス メーカーは、1 回限りの資本販売から、ハードウェア、消耗品、ソフトウェア アップデート、トレーニングを定期収益型のサブスクリプションにバンドルしたサービスとしてのプラットフォーム モデルに移行しています。この変化はエンタープライズ テクノロジーにおける SaaS の移行を反映しており、医療美容市場におけるクリニック導入の障壁を下げながら、メーカーの粗利益を 8 ~ 12 パーセント ポイント引き上げると予測されています。[17].

長寿医療の融合

代謝の最適化、再生療法、美的保存を統合した新たな長寿医療パラダイムは、アンチエイジングクリニックと美容医療の間に相互紹介経路を生み出しています。 Global Wellness Institute は、長寿経済が 2025 年に 1.8 兆米ドルに達すると評価しており、美的処置は消費者にとって重要な要素となります。[10]。この収束により、医療美容市場の対象人口の合計は、10年間で15〜20%拡大する可能性があります。

デバイス製造におけるサステナビリティと ESG

使い捨て消耗品や包装廃棄物に対する環境監視は強化されています。大手 OEM は、Cynosure と InMode がリサイクル可能なハンドピース プログラムを試験的に実施し、2030 年までに処置ごとのプラスチック廃棄物を 40 ~ 50% 削減することを約束しています。[18]。病院システムにおけるESGに沿った調達政策は、文書化された持続可能性ロードマップを持つメーカーにますます有利になり、医療美容市場内の競争力学を再形成することになる。

地域市場シェア分析

| 地域 |

主要な指標 |

主な投資テーマ |

| 北米 |

シェア38.9%(2025年) |

プレミアムデバイスの交換、AI の統合 |

| ヨーロッパ |

シェア29.4%(2025年) |

MDRコンプライアンス、医療ツーリズム |

| アジア太平洋地域 |

12.01% CAGR (2026 ~ 2035 年) |

クリニックの拡大、K-ビューティーの影響 |

| 南アメリカ |

USD 1.02 Billion (2025) |

ディストリビューターファイナンス、ボディコントゥアリング |

| 中東とアフリカ |

USD 0.87 Billion (2025) |

医療観光拠点、贅沢なウェルネス |

| 合計 |

USD 18.20 Billion (2025) |

— |

メディカルエステティック市場は、独特の地域力学を示しており、成熟した欧米市場は高級機器のアップグレードを優先する一方、新興国はクリニックネットワークの拡大に重点を置いています。

北米

| 国 |

主要な指標 |

キードライバー |

| 米国 |

地域収入の 82.3% |

世界最大の手続き量 |

| カナダ |

地域収入の 11.5% |

州のクリニックライセンスの拡大 |

| メキシコ |

地域収入の6.2% |

米国患者による医療ツーリズム |

米国は、FDAの有利な経路、高い消費者購買力、および認定医の密集したネットワークによって牽引され、メディカルエステティック市場において依然として単一最大の国内市場となっています。カナダの美容市場は、FDAの認可と調和した国境を越えた機器の承認から恩恵を受けている一方、米国国境沿いのメキシコの医療観光回廊は、認定された治療を求める価格重視の患者を惹きつけ続けている。[4].

ヨーロッパ

| 国 |

主要な指標 |

キードライバー |

| ドイツ |

10.41% CAGR |

高度な臨床インフラ |

| イギリス |

地域シェア23.8% |

有料の美容クリニック |

| フランス |

地域シェア17.2% |

医薬品注射剤の歴史 |

| イタリア |

USD 0.81 Billion (2025) |

医療ツーリズムの流入 |

| スペイン |

9.95% CAGR |

成長するウェルネスツーリズム |

| 北欧諸国 |

USD 0.42 Billion (2025) |

一人当たりの高い手術率 |

| ロシア |

8.2% CAGR |

国内デバイス製造 |

| ヨーロッパの残りの部分 |

USD 0.58 Billion (2025) |

EU MDR 調和効果 |

ヨーロッパの医療審美市場は、大規模で資本の充実したデバイス OEM を優遇する厳しい EU MDR 要件によって形成されています。英国の EU 離脱後の規制枠組みにより、独立した承認経路が確立され、EU のスケジュールと比較して特定のデバイスの導入が加速されています。[9].

アジア太平洋地域

| 国 |

主要な指標 |

キードライバー |

| 中国 |

地域シェア34.6% |

都市部の消費支出の伸び |

| インド |

14.62% CAGR |

クリニックインフラの拡張 |

| 日本 |

USD 0.72 Billion (2025) |

高齢化に伴う需要 |

| 韓国 |

地域シェア21.8% |

K-ビューティーエコシステムのリーダーシップ |

| アセアン |

13.40% CAGR |

医療観光拠点 |

| 残りのアジア太平洋地域 |

USD 0.31 Billion (2025) |

初期段階の市場開発 |

アジア太平洋地域は医療美容市場で最も急速に成長している地域であり、韓国は注射技術と併用療法の世界的なイノベーションハブとしての役割を果たしています。デジタル予約プラットフォームとインフルエンサー主導の需要に支えられ、中国の美容施術件数は2024年に年間2,000万件を突破[7].

南アメリカ

| 国 |

主要な指標 |

キードライバー |

| ブラジル |

地域シェア62.4% |

手術件数は世界で2番目に多い |

| アルゼンチン |

12.85% CAGR |

為替調整後の機器輸入 |

| 南アメリカの残りの地域 |

USD 0.24 Billion (2025) |

段階的な規制の最新化 |

ブラジルは美容施術の総件数で世界トップ 3 国の中にランクされており、ボディ コントゥアリングや注射による施術が需要をリードしています。南米の医療エステティック市場は、輸入機器の価格に影響を与える為替変動の逆風に直面しているが、ガルデルマとアッヴィによる現地組立事業がこの課題を部分的に相殺している[13].

中東とアフリカ

| 国 |

主要な指標 |

キードライバー |

| サウジアラビア |

地域シェア28.3% |

ビジョン 2030 のヘルスケア投資 |

| アラブ首長国連邦 |

13.71% CAGR |

ドバイとアブダビの医療ツーリズム |

| 南アフリカ |

USD 0.14 Billion (2025) |

民間医療インフラ |

| エジプト |

12.50% CAGR |

都市部の中産階級の成長 |

| MEAの残りの部分 |

USD 0.21 Billion (2025) |

初期段階の市場開発 |

贅沢なウェルネスの目的地としての UAE の位置付けにより、ドバイは医療美学市場の地域拠点となり、GCC 全域および南アジアから患者を惹きつけています。サウジアラビアのビジョン2030プログラムは医療投資を民間クリニックのライセンスに振り向け、選択的美容処置へのアクセスを拡大している[16].

医療美容市場セグメンテーション

デバイスの種類別

| セグメント |

主要な指標 |

主な需要要因 |

| エネルギーを利用した美容機器 |

シェア48.5%(2025年) |

マルチモーダルプラットフォームの採用 |

| 非エネルギーベースの美容機器 |

13.24% CAGR (2026 ~ 2035 年) |

生体刺激注射による増殖 |

レーザー、高周波、HIFU、強力パルス光(IPL)などのエネルギーベースのデバイスは、皮膚のリサーフェシング、脱毛、血管治療にわたる多用途性によって牽引され、依然として医療エステティック市場の収益の柱となっています。単一のプラットフォーム上で 2 つ以上のエネルギー方式を組み合わせたマルチモーダル コンソールが、従来の単機能ユニットに取って代わりつつあり、成熟市場では交換サイクルが平均 4 ~ 5 年になります。[2].

次世代ヒアルロン酸製剤やポリ-L-乳酸生体刺激物質が、エネルギーベースの治療結果よりも段階的で自然な結果を好む患者を惹きつけているため、注射可能な送達システム、マイクロダーマブレーションユニット、インプラントポートフォリオを含む非エネルギーベースのデバイスの割合が急速に成長しています。[8].

手続きの種類別

| セグメント |

主要な指標 |

主な需要要因 |

| 非外科的 / 低侵襲 |

シェア51.2%(2025年) |

ダウンタイムを最小限に抑えたいという消費者の好み |

| 外科的 |

13.55% CAGR (2026 ~ 2035 年) |

ハイブリッド手術エネルギー技術 |

注射可能な神経毒、フィラー、エネルギーベースの皮膚治療などの非外科的治療は、即日回復と低リスクプロファイルを提供するため、メディカルエステティック市場を支配しています。外科的処置は、脂肪移植技術や低侵襲脂肪吸引のバリエーションにより、外科的カテゴリーと非外科的カテゴリーの境界線があいまいになっているため、収益シェアは小さいものの急速に成長しています。[14].

用途別

| セグメント |

主要な指標 |

主な需要要因 |

| フェイシャルエステ |

シェア25.4%(2025年) |

神経毒とフィラーの需要 |

| ボディコントゥアリング |

14.35% CAGR (2026 ~ 2035 年) |

非侵襲的な脂肪減少技術 |

| 肌のリサーフェシングと引き締め |

USD 3.82 Billion (2025) |

高齢化に伴うコラーゲンの回復 |

| 脱毛 |

USD 2.10 Billion (2025) |

レーザー技術の小型化 |

| その他の用途 |

9.8% CAGR (2026 ~ 2035 年) |

傷跡修正と血管治療 |

フェイシャルエステティックは、神経毒(ボツリヌス毒素)およびヒアルロン酸フィラー処置の世界的な優位性によって、メディカルエステティック市場内で最大のアプリケーションシェアを占めています。しかし、クリオリポリシス、高周波脂肪分解、HIFU脂肪破壊プラットフォームが消費者の信頼と臨床的証拠を獲得するにつれて、ボディコントゥアリングは最速の速度で進歩しています。[12].

エンドユーザー別

| セグメント |

主要な指標 |

主な需要要因 |

| クリニックと皮膚科 |

シェア42.8%(2025年) |

専門実践者の集中力 |

| メディカルスパ |

14.41% CAGR (2026 ~ 2035 年) |

ウェルネスと美学の融合 |

| 病院 |

USD 3.05 Billion (2025) |

再建および術後の美しさ |

| 家庭用デバイス |

11.20% CAGR (2026 ~ 2035 年) |

家庭でのメンテナンスに対する消費者の需要 |

クリニックと皮膚科のオフィスは、医療美容市場の臨床インフラを支えており、注射やエネルギーベースの処置の大部分を扱っています。メディカル スパは、リラクゼーション指向のウェルネス サービスと臨床グレードのエステティック トリートメントを 1 つの屋根の下で融合させた、最も急速に成長しているエンドユーザー チャネルの代表です。[10].

競争力のあるベンチマーク

医療エステティック市場は中程度の集中を示しており、上位 5 社は合計で推定 42 ~ 48% の収益シェアを占めています。ハーフィンダール・ハーシュマン指数 (HHI) は 800 ~ 1,200 の範囲にあり、研究開発、規制に関する専門知識、流通ネットワークにおける規模の優位性がリーダーとニッチプレーヤーを分ける、競争的ではあるが断片化されていない状況を反映しています。 2022 年以降、統合の動きが激化し、いくつかの大型買収によりポートフォリオの幅が再形成されました。

| 会社 |

EST(東部基準時。収益分配範囲 |

主な製品 |

戦略的なポジショニング |

| アッヴィ(アラガン・エステティックス) |

~12~16% |

ボトックス、ジュビダーム、クールスカルプティング |

注射剤とデバイスを組み合わせた最も広範なポートフォリオ |

| ガルデルマ |

~8~11% |

レスティレーン、スカルプトラ、アズールア |

世界的なフィラーおよび生体刺激装置のリーダー |

| メルツ製薬 |

~6~9% |

ゼオミン、レディエッセ、ベロテロ |

差別化された神経毒と CaHA プラットフォーム |

| サイノシュア(ホロジック) |

~5~8% |

スカルプシュア、ピコシュア、テンプシュア |

エネルギーベースのデバイスの幅広さ |

| インモード |

~4~7% |

Morpheus8、BodyTite、FaceTite |

低侵襲性の RF 支援プラットフォーム |

| シネロン・カンデラ |

~4~6% |

ジェントルマックス プロ、ベラシェイプ |

確立されたマルチアプリケーションレーザーシステム |

| キュートラ |

~3~5% |

truSculpt、excel V+、AviClear |

ニキビと体の輪郭を整えるイノベーション |

| アルマレーザー |

~3~5% |

ソプラノ、アクセントプライム、ハーモニーXL |

価格競争力のあるグローバル流通 |

| ルーメニス |

~2~4% |

スプレンダー X、NuEra、レジェンド プロ+ |

IPL と RF の革新 |

| バウシュ ヘルス (ソルタ メディカル) |

~2~4% |

サーマクール FLX、フラクセル、クリア + ブリリアント |

プレミアムな肌の引き締めと表面の再生 |

最近のニュースと開発

- ガルデルマ (2024 年): スイス SIX 取引所で IPO を完了し、注入可能なパイプラインの拡張と新興市場の流通強化に資金を提供するために約 23 億米ドルを調達[19].

- Merz Pharmaceuticals (2021 ): 韓国のバイオテクノロジー Hugel の過半数株式を 19 億米ドルで取得し、バイオシミラーのボツリヌス毒素生産能力へのアクセスを獲得[21].

- 欧州委員会 (2024 年 1 月): クラス IIb 美容機器の MDR 移行期限を 2028 年 12 月まで延長し、中堅メーカーに対するコンプライアンスの圧力を緩和[9].

- Cutera (2022 年 3 月): FDA の認可を受けた初のエネルギーベースのニキビ治療装置である AviClear の 510(k) 認可を確保し、医療審美市場内で推定 6 億ドルの対応可能な機会を開拓[23].

医療美容市場レポートの範囲

| パラメータ |

詳細 |

| 市場範囲 |

世界の医療美容市場 — デバイス、注射剤、および関連消耗品 |

| 学習期間 |

2021 ~ 2035 年 |

| CAGR (予測期間) |

10.93% (2026 ~ 2035 年) |

| 市場規模(2025年) |

USD 18.20 Billion |

| 市場規模(2035年) |

USD 51.35 Billion |

| 最も急成長しているセグメント |

体の輪郭を整える (アプリケーションによる);メディカルスパ (エンドユーザーによる) |

| 紹介された企業 |

主要プレーヤー 10 社 (AbbVie、Galderma、Merz、Cynosure、InMode、Syneron Candela、Cutera、Alma Lasers、Lumenis、Bausch Health) |

| 評価通貨 |

USD Billion |