Software Defined Networking 市場の概要

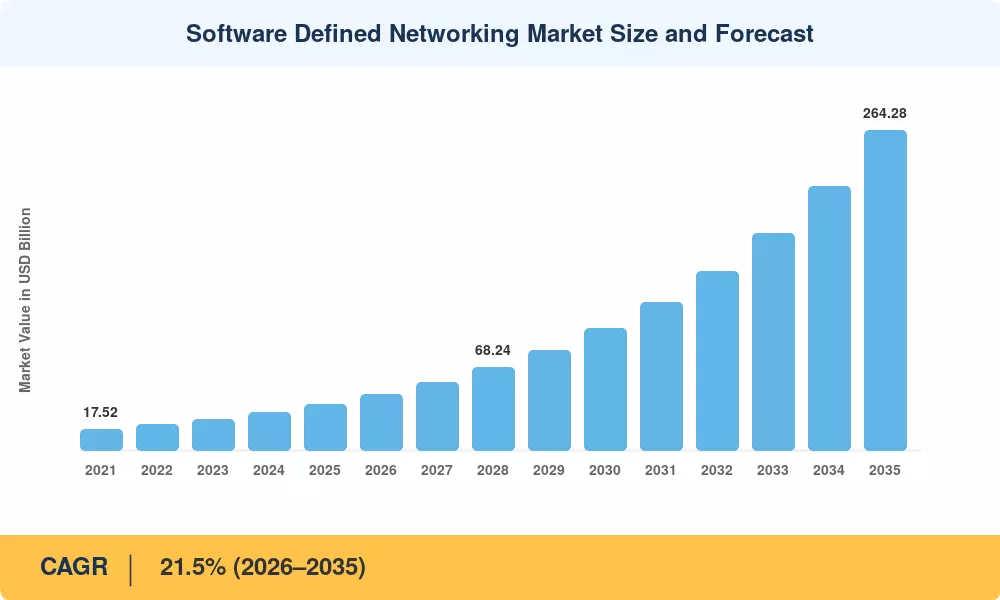

Software Defined Networking 市場は、2025 年に推定 382 億米ドルに達し、2026 年には 458 億米ドルに達し、その後 2026 ~ 2035 年の年平均成長率 21.5% で 2035 年までに 2,642 億 8000 万米ドルに拡大すると予測されています。この勢いの中心には 2 つの触媒があります。1 つは 5G スタンドアロン コア仮想化への世界的なラッシュで、通信事業者は年間 280 億米ドル以上をプログラマブル トランスポート ファブリックに振り向けています。[2]—そして、企業を独自のロックインではなくオープンソースのSDNコントローラープラットフォームに向けて推進する、EU、インド、ブラジルにわたるデジタル主権法の強化[3]。ソフトウェア デファインド ネットワーク市場は、かつてキャンパスやネットワークを支配していた手動の CLI 主導のプロビジョニング ワークフローを集中ネットワーク管理に置き換えるため、両方のトレンドから直接恩恵を受けています。データセンター環境。

これは段階的な変更ではありません。それは構造的なものです。企業やクラウド事業者は、固定機能のシャーシ スイッチを廃止し、ネットワーク プログラマビリティ ツールと OpenFlow SDN プロトコルによって制御されるマーチャント シリコン ホワイトボックス ハードウェアに移行しています。米国エネルギー省によるデータセンター効率に関する 2024 年の調査では、プログラム可能なネットワーク オーバーレイにより、ハイパースケール施設における東西トラフィックのエネルギー使用量が 18% 削減されることが示されました。[4]。インテントベースのオーケストレーションと合わせた効率性の向上により、仮想ネットワーク オーバーレイ設計への資本支出は 14 か月未満で利益が得られると CFO が確信しています。[5]。したがって、Software Defined Networking 市場は、アーリーアダプターの領域から主流のエンタープライズ調達サイクルに移行しつつあります。

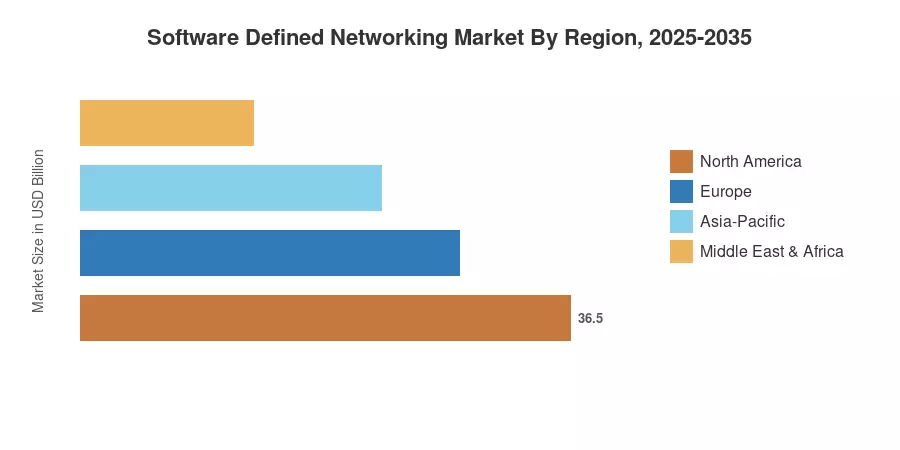

ハイパースケーラーの設備投資と政府のゼロトラスト ルールにより、北米の Software Defined Networking 市場は 2025 年に約 39.5% に上昇[6]。アジア太平洋地域は、インドの BharatNet フェーズ III ファイバー導入と中国の「東データ西コンピューティング」プログラムによって牽引され、2035 年までの CAGR 22.8% で最も急成長している地域です。[7]。ヨーロッパは第 2 位のプレーヤーであり、市場シェアは約 26.0% です。 EUチップ法とGAIA-XプログラムによりソブリンSDNコントローラープラットフォームへの投資が行われています[8]。 Software Defined Networking 市場は、加速するクラウド移行と AI 主導のテレメトリにより、予測期間中に急速に成長すると予想されます。

レポートの重要なポイント

• コンポーネント別

- SDN インフラストラクチャは、ハイパースケール データセンター全体でのヘビー ホワイト ボックス スイッチの採用を反映して、2025 年の Software Defined Networking 市場の約 48.0% を獲得しました。

- 企業が集中ネットワーク管理をマネージド サービス プロバイダーにアウトソーシングするため、サービスとサポートは 2035 年まで 22.5% の CAGR で拡大しています。

• 導入モード別

- オンプレミスのインストールは、2025 年の Software Defined Networking 市場の約 57.5% を維持し、データ常駐コンプライアンスを必要とする規制業界に好まれています。

- クラウド導入は、マルチクラウド オーケストレーションの需要と仮想ネットワーク オーバーレイの採用により、2035 年まで 24.1% の CAGR で加速しています。

• 地域別

- 連邦政府のゼロトラスト調達義務に支えられ、北米が 2025 年の収益シェア 39.5% で首位を獲得しました。

- アジア太平洋地域は、5G の展開スケジュールにより、全地域の中で最速となる 22.8% の CAGR で成長すると予測されています。

- ヨーロッパの Software Defined Networking 市場は、GAIA-X およびオープンソース SDN コントローラー プラットフォームによって牽引され、世界収益の 26.0% を占めました。

市場規模と予測 (2021 ~ 2035 年)

Market Research Future (MRFR) マーケット サイジングでは、ボトムアップの収益モデル (ベンダーの出荷、サブスクリプションの請求、プロフェッショナル サービスの予約) と、および[9]。歴史上の人物 (2021 ~ 2024 年) は実績です。 2025 年は基準年に基づく推定値です。 2026 年から 2035 年は 21.5% の CAGR に基づく予測です。

ドライバーの影響分析

| ドライバ |

CAGR に対する ~% の影響 |

地理的な関連性 |

影響のタイムライン |

参照 |

| 5G コアの仮想化とネットワーク スライシング |

~4.2% |

グローバル |

短期(2年以内) |

[2] |

| マルチクラウドおよびハイブリッドクラウドの移行 |

~3.8% |

北米、ヨーロッパ |

短期(2年以内) |

[9] |

| ゼロトラストとマイクロセグメンテーションの義務 |

~3.1% |

北米 |

中期(2~4年) |

[6] |

| AI/ML 主導のネットワーク テレメトリ |

~2.9% |

グローバル |

中期(2~4年) |

[12] |

| データセンターのエネルギー効率規制 |

~2.5% |

ヨーロッパ、アジア太平洋 |

長期(4年以上) |

[4] |

| デジタル主権とオープンソースのポリシー |

~2.4% |

ヨーロッパ、アジア太平洋 |

長期(4年以上) |

[3] |

| エッジ コンピューティングと IoT トラフィックの爆発的増加 |

~2.1% |

アジア太平洋地域 |

中期(2~4年) |

[15] |

5G コアの仮想化とネットワーク スライシング

世界中の通信事業者はスタンドアロンを優先しています5Gコア高度なサービスを可能にする展開。最新のグリーンフィールド 5G コアは、SDN ベースのプラットフォームを介した集中ネットワーク管理に依存して、動的なネットワーク スライシングを調整します。スライスのライフサイクル管理にプログラム可能な SDN プロトコルを使用すると、運用効率が大幅に向上し、手動の従来の構成方法と比較してプロビジョニング時間が大幅に短縮されます。このサービス作成サイクルの圧縮により、Software Defined Networking が 5G の競争力の基本要件として位置付けられます。

マルチクラウド オーケストレーションの需要

Flexera の 2024 年のクラウド現状レポートによると、企業の 89% が 2 つ以上のパブリック クラウドで運用されており、基盤となるトランスポートの違いを抽象化する仮想ネットワーク オーバーレイ ファブリックに対する深刻な需要が生じていることがわかりました。[10]。 AWS、Azure、GCP 環境全体でポリシーの適用を統合するネットワーク プログラマビリティ ツールが、断片化されたクラウドごとの VPN 構成を置き換え、中堅企業の運用コストを年間平均 120 万米ドル節約しています。[9].

ゼロトラスト ネットワーク アクセスの義務

米国管理予算局の M-22-09 覚書では、すべての連邦政府機関が 2024 年度末までにゼロトラスト アーキテクチャを実装することを義務付けており、SDN コントローラー プラットフォーム上に構築されたマイクロセグメンテーション ソリューションに 35 億米ドル以上が投入されています。[6]。この連邦政府の支出は防衛産業基地の請負業者や州レベルの機関に波及し、公共部門における注目すべきSoftware Defined Networking市場を拡大している。

AI 主導のネットワーク テレメトリ

AI 推論とネットワーク プログラマビリティの融合により、運用が再構築されています。大企業では、集中管理プレーンからストリーミング テレメトリを取り込み、異常検出とトラブルシューティングを自動化する AIOps プラットフォームの導入が増えています。ハイブリッドおよびマルチクラウド アーキテクチャにより IT インフラストラクチャが複雑になるにつれて、これらの AI 主導のプラットフォームは、運用チームがパフォーマンスを維持し、ネットワーク容量をプロアクティブに計画するために不可欠なツールになりつつあります。

拘束影響分析

| 拘束 |

CAGR に対する ~% のマイナスの影響 |

地理的な関連性 |

影響のタイムライン |

参照 |

| レガシーネットワーク機器のロックイン |

~–1.8% |

グローバル |

短期(2年以内) |

[9] |

| 熟練したSDN人材の不足 |

~–1.5% |

北米、ヨーロッパ |

中期(2~4年) |

[17] |

| 相互運用性と標準の断片化 |

~–1.3% |

グローバル |

中期(2~4年) |

[11] |

| 集中型コントローラーに関するセキュリティ上の懸念 |

~–1.0% |

グローバル |

長期(4年以上) |

[18] |

| 中小企業にとっては初期移行コストが高い |

~–0.9% |

アジア太平洋、南米 |

短期(2年以内) |

|

レガシー機器のロックイン

多くの企業は依然として、既存ベンダーの独自のシャーシ スイッチで複数年の減価償却サイクルを運用しています。 2024 年のキャンパス ネットワークの 47% は 3 年以上前のファームウェアを実行しており、OpenFlow SDN プロトコルへのフォークリフト アップグレードは経済的に負担が大きいと推定されています[9]。リース サイクルが期限切れになるまで、これらのブラウンフィールド環境は、Software Defined Networking 市場が新しい導入を吸収できるペースを制限します。

熟練したSDN人材の不足

Linux Foundation やその他の人材アナリストからのさまざまなレポートを含む業界調査では、クラウド ネイティブ ネットワーキングとネットワーク プログラマビリティは需要が高く、満たすのが難しいスキル セットであることが一貫して特定されています。従来の CLI ベースのネットワーク管理とは異なり、集中型 SDN コントローラーを操作するために必要な専門知識は依然として不足しています。その結果、多くの企業が採用スケジュールの延長を報告しており、これが移行プロジェクトの実質的なボトルネックとなっています。

相互運用性と標準の断片化

OpenFlow SDN プロトコルが元の基礎を築きましたが、競合するサウスバウンド インターフェイス (P4、gNMI、gRPC) が断片化されたコントロール プレーン エコシステムを作成しました。[11]。異なるベンダーの SDN コントローラー プラットフォームを共存させる必要がある場合、統合に摩擦が生じ、総所有コストが上昇し、調達の意思決定が遅くなることが購入者から報告されています。

ソフトウェア・デファインド・ネットワーキングの市場機会

ソブリンおよびオープンソースの SDN プラットフォーム

EU (GAIA-X)、インド (MeitY クラウド指令)、ブラジル (LGPD 隣接インフラストラクチャ規則) のデジタル主権法は、ONOS や OpenDaylight などのオープンソース SDN コントローラー プラットフォームに対して明確な市場のくさびを生み出しています。[3]。これらのコントローラーを商用サポートおよびコンプライアンス認定とともにパッケージ化するベンダーは、独自のスタックではアクセスできない政府および重要インフラの予算を獲得できます。

SD-WAN と SASE の統合

SD-WAN とセキュア アクセス サービス エッジを単一のクラウド提供サービスに急速に融合させることで、Software Defined Networking 市場内に高成長レーンが開かれています。 SASE への支出は 2028 年までに 250 億米ドルを超えると予測されており、あらゆる SASE 導入は以下に依存しています。仮想ネットワーク集中ネットワーク管理コンソールを通じて管理されるオーバーレイ トンネル[10].

新興市場の電気通信の近代化

アフリカと東南アジアは、通信事業者が接続を拡張するためにプログラム可能な輸送インフラを優先している重要なグリーンフィールド領域です。 ASEAN スマート シティ ネットワークなどの地域の取り組みでは、将来性のある展開を保証するためにプログラム可能なネットワーク要件を指定することが増えています。これにより、Software Defined Networking 市場は、レガシー インフラストラクチャの負担のない地域での継続的な導入が可能になります。

Network-as-a-Service の収益モデル

NaaS サブスクリプションは、先行投資費用を定期的な運用費用に変換し、中小企業の障壁を下げます。通信事業者は、SDN コントローラー プラットフォーム、仮想ネットワーク オーバーレイ プロビジョニング、AI テレメトリを使用量ベースのバンドルにパッケージ化し、新たな収益化ストリームを開拓しています。したがって、NaaS の収益は 2024 年に世界で 120 億米ドルに達すると推定されています。[15].

AIネイティブのクローズドループオートメーション

AI と機械学習をネットワーク プログラマビリティ ツールに統合することで、人間の介入を最小限に抑えながら、ネットワークが自動的に障害を検出、診断、解決する「閉ループ修復」が可能になります。具体的なパフォーマンスの向上は展開によって異なりますが、初期導入者は平均修理時間 (MTTR) の大幅な改善を一貫して報告しており、これはプロバイダーが強化されたサービス レベル アグリーメント (SLA) を通じてサービス提供を差別化するのに役立ちます。

Software Defined Networking市場の将来展望

AI による自律的なネットワーク運用

2030 年までに、ますます多くの Tier-1 サービス プロバイダーが高度に自律的なネットワーク運用を採用すると予想されます。このモデルでは、AI エンジンが集中管理レイヤーからリアルタイム テレメトリを取り込み、人間の介入を最小限に抑えてネットワーク修復を実行します。その結果、Software Defined Networking (SDN) 市場は、スタンドアロン コントローラーの販売から、AI 推論をネットワーク ファブリックに直接組み込むインテリジェントな統合プラットフォームの販売へと移行しています。

プラットフォームの経済性とサービスとしてのネットワーク

サブスクリプションエコノミーはベンダー経済を根本的に再構築しています。主要なネットワーク既存企業は、ポートフォリオを年間経常収益 (ARR) モデルに積極的に移行しています。仮想ネットワーク オーバーレイ プロビジョニングと使用量ベースの課金をバンドルした NaaS プラットフォームは、資本支出を削減し、運用の俊敏性を向上させたい中堅企業にとって、ますます好まれる調達モデルになりつつあります。

持続可能性とネットワークエネルギーの最適化

EU エネルギー効率指令 (EED) の改定により、500 kW を超えるデータセンターは 2025 年から電力使用効率を報告することが義務付けられ、未使用のスイッチ ポートの電源を動的にオフにするプログラム可能なトラフィック エンジニアリングが奨励されています。[4]。総合的なエネルギー最適化のためにビル管理システムと統合するネットワーク プログラマビリティ ツールは、Software Defined Networking 市場で急速に出現している価値提案を表しています。

6G 対応のプログラマブル ファブリック

2028 年までに完成すると予想される ITU-R の IMT-2030 フレームワークには、SDN ネイティブ アーキテクチャのみが提供できる決定論的ネットワーキングとミリ秒未満のジッター保証が組み込まれています。[14]。韓国、フィンランド、日本の初期の 6G テストベッド プログラムでは、すでに OpenFlow SDN プロトコルと P4 プログラム可能なパイプラインが指定されており、Software Defined Networking 市場が次世代無線トランスポートの基盤となることを示しています。

地域市場シェア分析

| 地域 |

主要な指標 |

主な投資テーマ |

| 北米 |

収益シェア 39.5% (2025 年) |

ゼロトラストの義務。ハイパースケーラーの設備投資 |

| ヨーロッパ |

USD 9.93 billion (2025) |

ガイアX;エネルギー効率の高いデータセンター |

| アジア太平洋地域 |

22.8% の CAGR (2026 ~ 2035 年) |

5G SA の展開。ソブリンクラウドプログラム |

| 南アメリカ |

USD 1.91 billion (2025) |

電気通信の近代化。フィンテックの成長 |

| 中東とアフリカ |

23.5% の CAGR (2026 ~ 2035 年) |

スマートシティへの取り組み。海底ケーブル着地 |

| 合計 |

USD 38.20 billion (2025) |

— |

Software Defined Networking 市場は、クラウド導入の成熟度、規制の枠組み、通信投資サイクルの違いによって顕著な地域差が見られます。

北米

| 国 |

主要な指標 |

キードライバー |

| 私たち |

地域シェア78.2% |

連邦政府のゼロトラスト支出 |

| カナダ |

USD 1.58 billion (2025) |

テレコムオープンRANパイロット |

| メキシコ |

20.8% の CAGR (2026 ~ 2035 年) |

ニアショアリングのデータセンター構築 |

米国が北米の Software Defined Networking 市場を独占しているのは、Amazon、Microsoft、Google のハイパースケーラーが 2024 年にデータセンターの設備投資に合計 1,400 億ドル以上を割り当て、すべての新しいビルドにネットワーク プログラマビリティ ツールが組み込まれているためです。[9]。カナダの CRTC ブロードバンド基金は、サービス提供要件として集中ネットワーク管理を指定するオープンアクセス ファイバー ネットワークに資金を提供しています。一方、メキシコのニアショアリング ブームは、初日から仮想ネットワーク オーバーレイ アーキテクチャを導入する Tier-III データセンター事業者を惹きつけています。[7].

ヨーロッパ

| 国 |

主要な指標 |

キードライバー |

| ドイツ |

地域シェアの22.5% |

インダストリー 4.0 キャンパス SDN |

| イギリス |

USD 1.85 billion (2025) |

金融サービスネットワークの自動化 |

| フランス |

21.8% の CAGR (2026 ~ 2035 年) |

ソブリンクラウド入札 |

| イタリア |

USD 0.72 billion (2025) |

5G 固定無線アクセス |

| スペイン |

20.9% の CAGR (2026 ~ 2035 年) |

観光部門の Wi-Fi モダナイゼーション |

| 北欧諸国 |

USD 0.88 billion (2025) |

グリーン データセンター クラスター |

| ロシア |

19.2% の CAGR (2026 ~ 2035 年) |

インポート代替 SDN プラットフォーム |

| ヨーロッパの残りの部分 |

USD 1.45 billion (2025) |

EU 結束基金のデジタル化 |

欧州の Software Defined Networking 市場は、公共部門の契約にサービスを提供するクラウド プロバイダーがオープン標準の SDN コントローラー プラットフォームをサポートする必要があるという EU の義務の恩恵を受けています。[3]。ドイツの Industrie 4.0 プログラムにより、キャンパスファブリック SDN がスマートファクトリー接続の標準となりました。また、英国の FCA 主導のネットワーク復元ルールにより、金融機関は自動フェイルオーバー用の OpenFlow SDN プロトコルの採用を余儀なくされています。[8].

アジア太平洋地域

| 国 |

主要な指標 |

キードライバー |

| 中国 |

地域シェア36.8% |

東-データ-西-コンピューティング プログラム |

| インド |

24.5% の CAGR (2026 ~ 2035 年) |

BharatNet フェーズ III ファイバー拡張 |

| 日本 |

USD 1.42 billion (2025) |

エンタープライズDX(デジタルトランスフォーメーション) |

| 韓国 |

23.1% の CAGR (2026 ~ 2035 年) |

5G-Advanced ネットワーク スライシング |

| アセアン |

USD 1.15 billion (2025) |

スマートシティとフィンテックインフラストラクチャ |

| 残りのアジア太平洋地域 |

21.8% の CAGR (2026 ~ 2035 年) |

海底ケーブル陸揚げ局 |

アジア太平洋地域は、Software Defined Networking 市場で最も急速に成長している地域であり、2027 年までに国営通信事業者がすべてのメトロおよびバックボーン ノードにわたって集中ネットワーク管理を展開するという中国の命令によって推進されています。[7]。インドの電気通信規制当局 TRAI は、すべての新しいブロードバンド ライセンスに、ネットワーク プログラマビリティ ツールへの準拠を証明することを要求しています。これは、グリーンフィールド ビルドを SDN ネイティブ アーキテクチャと仮想ネットワーク オーバーレイ ファブリックに向けて集中させる規則です。[15].

南アメリカ

| 国 |

主要な指標 |

キードライバー |

| ブラジル |

地域シェア58.2% |

フィンテックとオープンバンキングのトラフィックの増加 |

| アルゼンチン |

21.0% の CAGR (2026 ~ 2035 年) |

通信民営化の波 |

| 南アメリカの残りの地域 |

USD 0.42 billion (2025) |

海底ケーブルプロジェクト |

取引量で世界第 3 位のブラジルの急成長するフィンテック エコシステムは、SDN コントローラー プラットフォーム上に構築されたプログラマブルで低遅延のデータセンター ファブリックを需要しており、この地域におけるソフトウェア デファインド ネットワーク市場は 2 桁の力強い成長を遂げることができます。[15].

中東とアフリカ

| 国 |

主要な指標 |

キードライバー |

| サウジアラビア |

地域シェア35.0% |

NEOM スマートシティ構築 |

| アラブ首長国連邦 |

USD 0.35 billion (2025) |

金融ハブのデータセンター拡張 |

| 南アフリカ |

22.0% の CAGR (2026 ~ 2035 年) |

通信事業者の最新化 |

| エジプト |

21.5% の CAGR (2026 ~ 2035 年) |

新たな行政資本ICTバックボーン |

| MEAの残りの部分 |

USD 0.38 billion (2025) |

AfDBデジタル基金プロジェクト |

サウジアラビアのビジョン 2030 では、デジタル インフラストラクチャに 64 億米ドル以上が割り当てられており、NEOM の完全にプログラム可能な都市バックボーンは、トランスポート標準として OpenFlow SDN プロトコルを指定しています。[7]。 2Africa と Equiano の新しい海底ケーブルが、グリーンフィールド事業者が集中ネットワーク管理プラットフォームを通じて管理する帯域幅を提供するため、アフリカの Software Defined Networking 市場は加速しています。

Software Defined Networking 市場セグメンテーション

コンポーネント別

| セグメント |

主要な指標 |

主な需要要因 |

| SDNインフラストラクチャ |

シェア48.0%(2025年) |

ハイパースケール DC でのホワイトボックス スイッチの導入 |

| SDN ソフトウェア / コントローラー |

USD 13.75 billion (2025) |

インテントベースのポリシーオーケストレーション |

| サービスとサポート |

22.5% の CAGR (2026 ~ 2035 年) |

マネージド集中ネットワーク管理アウトソーシング |

SDN インフラストラクチャが Software Defined Networking 市場をリードしているのは、ハイパースケールおよび Tier-1 コロケーション事業者が Broadcom と Marvell のマーチャント シリコン ハードウェアに投資を続けているためです。リーフ スパイン ホワイト ボックス スイッチの大量購入により、ソフトウェア ライセンスの絶対額を上回る大規模なハードウェア収益基盤が生まれますが、ソフトウェア マージンは 3 ~ 5 倍になります。サービスとサポートは、社内に専門知識を持たない中堅企業がネットワーク プログラマビリティ ツールを契約したり、システム インテグレーターからマネージド サービスを提供したりする中で、最も急速に成長しているコンポーネントです。

導入モード別

| セグメント |

主要な指標 |

主な需要要因 |

| オンプレミス |

シェア57.5%(2025年) |

規制上のデータ常駐義務 |

| 雲 |

24.1% の CAGR (2026 ~ 2035 年) |

マルチクラウド仮想ネットワークオーバーレイの自動化 |

銀行、防衛、ヘルスケアのバイヤーが SDN コントローラー プラットフォームのローカル制御を主張しているため、オンプレミス展開が今日の Software Defined Networking 市場を支配しています。ただし、SaaS で提供されるコントローラーによって中小企業の障壁が低くなり、地理的に分散したブランチ オフィス全体でネットワークの一元管理が可能になるため、クラウド ベースの SDN 管理はますます複雑化しています。

組織規模別

| セグメント |

主要な指標 |

主な需要要因 |

| 大企業 |

シェア66.0%(2025年) |

複雑なマルチサイトのキャンパス ファブリック |

| 中小企業 |

23.4% CAGR (2026 ~ 2035 年) |

NaaSサブスクリプションモデル |

用途別

| セグメント |

主要な指標 |

主な需要要因 |

| データセンターとクラウド |

シェア55.0%(2025年) |

東西トラフィックの最適化 |

| エンタープライズキャンパス |

USD 7.26 billion (2025) |

Wi-Fi 6E/7 ファブリックの統合 |

| SD-WAN |

23.8% の CAGR (2026 ~ 2035 年) |

ブランチからクラウドへの SASE コンバージェンス |

データセンターおよびクラウド アプリケーション セグメントは、プログラマブルでロスレス イーサネット ファブリックを必要とする AI トレーニング ワークロードの急激な増加により、ソフトウェア デファインド ネットワーク市場の最大の部分を占めています。企業が仮想ネットワーク オーバーレイ トンネルを通じて WAN の最適化とセキュリティを融合するにつれて、SD-WAN アプリケーションは最も急激な成長を記録しています。

エンドユーザー別

| セグメント |

主要な指標 |

主な需要要因 |

| 通信およびクラウド サービス プロバイダー |

シェア34.5%(2025年) |

5G SA コアとネットワーク スライシング |

| BFSI |

USD 5.35 billion (2025) |

規制のマイクロセグメンテーション |

| 製造業 |

22.5% の CAGR (2026 ~ 2035 年) |

SDN を介した OT/IT の融合 |

| 政府 |

21.8% の CAGR (2026 ~ 2035 年) |

ゼロトラスト義務の遵守 |

| 健康管理 |

USD 2.10 billion (2025) |

HIPAA 準拠のネットワーク セグメンテーション |

すべての 5G スタンドアロン コア導入では、仮想ネットワーク機能を管理するために OpenFlow SDN プロトコルまたは同等のサウスバウンド API が必要となるため、通信プロバイダーとクラウド サービス プロバイダーが Software Defined Networking 市場で最大のエンドユーザー シェアを占めています。製造業は最も急速に成長しているエンドユーザー分野であり、インダストリー 4.0 の工場では集中ネットワーク管理を導入し、単一のプログラム可能なファブリックで運用テクノロジーと IT ネットワークを統合しています。

競争力のあるベンチマーク

Software Defined Networking 市場は適度に集中しており、上位 5 社が世界収益の 38 ~ 46% を占めると予想されています。ハーフィンダール・ハーシュマン指数は 600 ~ 900 であり、競争力はあるが断片化されていない構造を示唆しています。ホワイトボックスの代替品がASPを侵食する中、既存企業はマージンを守るために、ハードウェアポートフォリオとSDNコントローラプラットフォーム、サブスクリプションソフトウェア、プロフェッショナルサービスを積極的にバンドルしている。

| 会社 |

EST(東部基準時。収益分配範囲 |

Software Defined Networking 市場向けの主な製品 |

戦略的なポジショニング |

| シスコシステムズ |

~12~15% |

ACI、Catalyst SD-WAN、DNA センター |

フルスタック キャンパス + DC SDN。サブスクリプションピボット |

| ヴイエムウェア (ブロードコム) |

~8~11% |

NSX、VeloCloud SD-WAN |

仮想ネットワーク オーバーレイ リーダー。マルチクラウドファブリック |

| ジュニパーネットワークス (HPE) |

~6~9% |

アプストラ、コントレイル、ミストAI |

インテントベースの DC ファブリック。 AI ネイティブの運用 |

| ファーウェイ・テクノロジーズ |

~5~8% |

CloudFabric、アジャイルコントローラー |

価格競争力がある。 APAC/MEAでの強い存在感 |

| ノキア |

~4~7% |

ニュアージュネットワークスVSP、NSP |

通信中心の SDN コントローラー プラットフォーム |

| アリスタネットワークス |

~3~5% |

CloudVision、DANZ モニタリング ファブリック |

ハイパースケーラー DC スイッチング。テレメトリーファースト |

| デル・テクノロジーズ |

~3~5% |

SmartFabric OS10、VxRail SDN 統合 |

統合インフラ。オープンネットワーキングエコシステム |

| マイクロソフト |

~2~4% |

Azure仮想WAN、SONiC |

オープンソースのスイッチ OS。クラウドネイティブのSDN |

| IBM |

~2~4% |

ネットワーク自動化のためのクラウドパック |

AI 運用の統合。ハイブリッドクラウドに焦点を当てる |

| エクストリームネットワークス |

~1~3% |

ExtremeCloud IQ、ファブリック コネクト |

中規模市場のキャンパス SDN。クラウド管理型 |

最近のニュースと開発

-

シスコシステムズ(2024 年 8 月): ハイパースケールの AI トレーニング展開をターゲットとして、集中ネットワーク管理と GPU クラスター スケジューリングを統合する、AI に最適化されたデータセンター SDN プラットフォームである Nexus HyperFabric を発売[19].

- VMware / Broadcom (2024 年 7 月): 分散ファイアウォールの機能強化とネイティブ仮想ネットワーク オーバーレイ暗号化を備えた NSX 4.2 をリリースし、買収後のエンタープライズ マイクロセグメンテーション要件に対応[20].

-

ジュニパーネットワークス/ HPE (2025 年 7 月): 140 億米ドルによるジュニパーネットワークスの買収を完了し、HPE の Aruba キャンパス ポートフォリオとジュニパーの Apstra インテントベース SDN コントローラー プラットフォームを組み合わせました。[21].

- 欧州委員会 (2024 年 3 月): 500,000 ユーロを超える公共部門のネットワーク調達に互換性のある規則を実施する EU 相互運用可能欧州法を発行[3].

- Huawei Technologies (2024 年 9 月): ネットワーク プログラマビリティ ツールを使用して 5G トランスポート層をアップグレードする APAC 通信事業者を対象とした、AI 主導の予測的障害分離機能を備えた CloudFabric 3.0 を発表[22].

- Arista Networks (2025 年 3 月): ソフトウェア デファインド ネットワーク市場全体の閉ループ修復のために AI 推論エンジンにデータを供給するテレメトリ プラットフォームである CloudVision Universal Network Observability を導入しました。[23].

よくある質問

Q1. OpenFlow と P4 は、SDN サウスバウンド インターフェイスとしてどのように比較されますか?

OpenFlow は固定のマッチアクション テーブルを定義しますが、P4 ではオペレータがシリコン レベルでデータプレーン パイプラインをプログラムできるようになります。ほとんどの企業は、レガシー スイッチ用の OpenFlow SDN プロトコルと、新しいプログラマブル ASIC 用の P4 の両方を組み合わせています。[11].

Q2. MPLS から SD-WAN に移行する場合、購入者はどれくらいの回収期間を想定する必要がありますか?

一般的な MPLS から SD-WAN への移行では、回線コストの削減と集中ネットワーク管理の自動化により、10 ~ 14 か月以内に投資回収が可能です。換算されたブランチ サイトの数に応じた節約規模[5].

Q3.マルチベンダーの相互運用性を最もよくサポートする SDN コントローラー プラットフォームはどれですか?

OpenDaylight と ONOS は最も広範なベンダー中立のプラグイン エコシステムを提供し、Cisco ACI と VMware NSX は単一ベンダーに最適化された環境をリードします。購入者の選択は、既存の仮想ネットワーク オーバーレイのコミットメントに依存します[11].

Q4. Software Defined Networking 市場はデータセンターのエネルギー削減目標にどのように取り組んでいますか?

SDN コントローラ プラットフォームは、少数のアクティブなスイッチ パスを介してトラフィックを動的にルーティングし、未使用のポートが低電力状態になることを可能にします。 DOE の試験では、プログラム可能な交通エンジニアリングにより 18% のエネルギー節約が実証されました[4].

Q5.ネットワーク プログラマビリティ ツールは 5G ネットワーク スライシングにおいてどのような役割を果たしますか?

これらは、スライスの作成、帯域幅の割り当て、共有物理インフラストラクチャ全体の SLA モニタリングを自動化します。プログラム可能なツールがなければ、オペレーターは顧客が要求する 5 分未満の時間枠内でスライスをプロビジョニングすることができません。[2].

Q6. Software Defined Networking 市場は、米国と中国の技術輸出規制によってどのような影響を受けますか?

輸出規制により、ファーウェイによる高度な商用シリコンへのアクセスが制限され、規制市場でのシェアはシスコやアリスタに移っている。中国の通信事業者は代替手段として国内のSDNコントローラープラットフォームを加速させている[22].

Q7. SDN をブラウンフィールド キャンパス ネットワークにオーバーレイする場合、統合にはどのような課題が生じますか?

レガシー スイッチには OpenFlow SDN プロトコルのサポートがないことが多く、移行シムとしてポリシーベースのルーティングを使用したハイブリッド モードが強制されます。スパインでの仮想ネットワーク オーバーレイから開始する段階的な移行により、中断を最小限に抑えます[17].

Software Defined Networking市場レポートの範囲

| パラメータ |

詳細 |

| 市場範囲 |

世界のソフトウェア・デファインド・ネットワーキング市場 — ハードウェア、ソフトウェア、サービス |

| 学習期間 |

2021 ~ 2035 年 |

| CAGR (予測) |

21.5% (2026 ~ 2035 年) |

| 基準年の市場規模 |

USD 38.20 billion (2025) |

| 2026 年の予測開始 |

USD 45.80 billion |

| 2035 年の予測エンドポイント |

USD 264.28 billion |

| 最も急成長しているセグメント |

クラウド展開 (CAGR 24.1%); SD-WAN アプリケーション (23.8% CAGR) |

| 紹介された企業 |

Cisco、VMware (Broadcom)、ジュニパー (HPE)、Huawei、Nokia、Arista、Dell、Microsoft、IBM、Extreme Networks |

| 評価通貨 |

USD billion |