Software Defined Networking (SDN) Market Summary

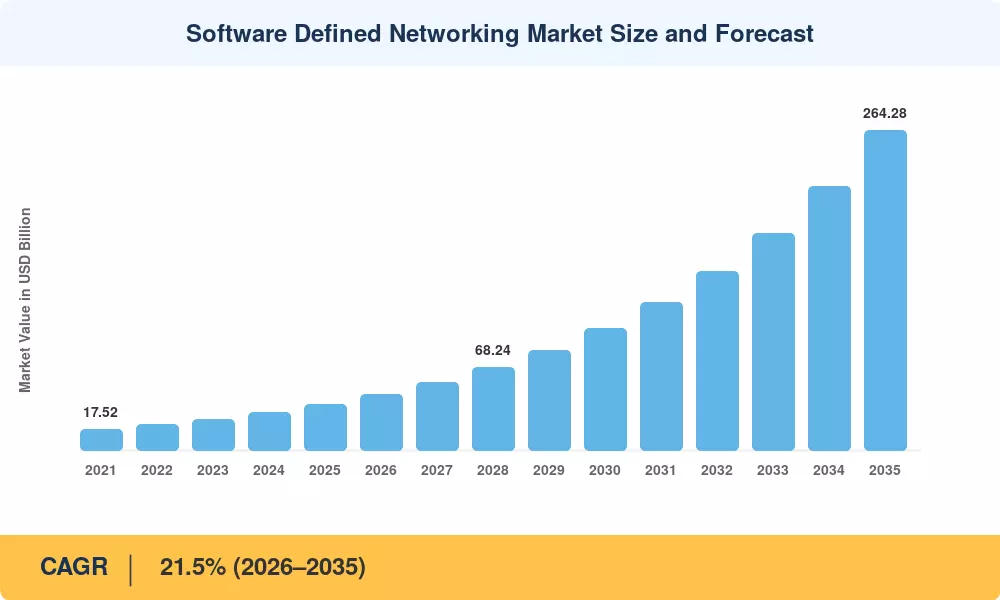

The Software Defined Networking Market reached an estimated USD 38.20 billion in 2025 and is projected to climb to USD 45.80 billion in 2026 before expanding to USD 264.28 billion by 2035 at a compound annual growth rate of 21.5% during 2026–2035. Two catalysts sit at the center of this momentum: the global rush toward 5G standalone core virtualization—where operators are redirecting upward of USD 28 billion annually into programmable transport fabrics [2]—and the tightening of digital-sovereignty legislation across the EU, India, and Brazil that pushes enterprises toward open-source SDN controller platforms rather than proprietary lock-in [3]. The Software Defined Networking Market benefits directly from both trends because centralized network management replaces the manual CLI-driven provisioning workflows that once dominated campus and data-center environments.

This isn’t an incremental change; it’s structural. Enterprises and cloud operators are retiring fixed-function chassis switches and moving to merchant-silicon white-box hardware controlled by network programmability tools and OpenFlow SDN protocols. In a 2024 research on data-center efficiency by the U.S. Department of Energy, programmable network overlays were shown to lower energy usage of east-west traffic by 18% in hyperscale facilities [4]. The efficiency dividend, along with intent-based orchestration, is persuading CFOs that the capital expenditure for virtual network overlay designs delivers returns in under 14 months [5]. So the Software Defined Networking Market is moving from early adopter territory to mainstream enterprise procurement cycles.

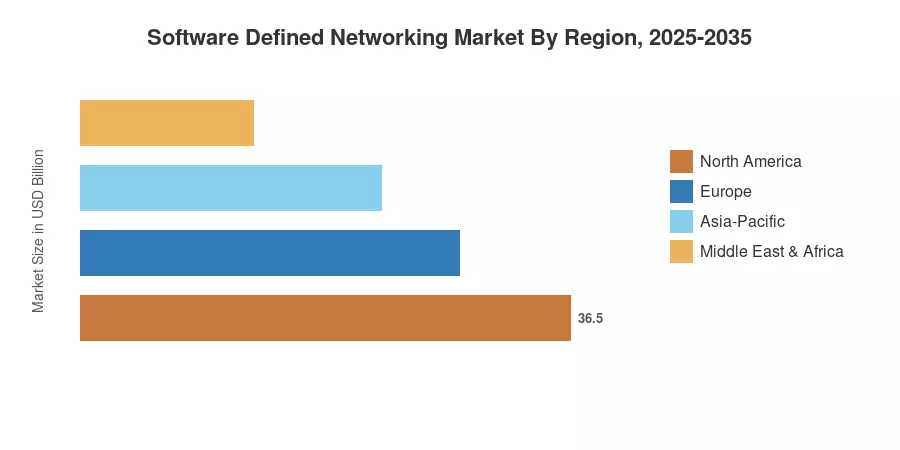

Hyperscaler capex and government zero-trust rules drove the Software Defined Networking Market in North America to around 39.5% in 2025 [6]. Asia-Pacific is the fastest-growing region with a CAGR of 22.8% through 2035, led by India’s BharatNet Phase III fiber rollouts and China’s “East-Data-West-Computing” program [7]. Europe is the second largest player with a market share of around 26.0%. Investment is being made in sovereign SDN controller platforms by the EU Chips Act and the GAIA-X program [8]. The Software Defined Networking Market is expected to grow at a rapid pace during the forecast period, owing to an accelerated cloud migration and AI-driven telemetry.

Key Report Takeaways

• By Component

- SDN Infrastructure captured roughly 48.0% of the Software Defined Networking Market in 2025, reflecting heavy white-box switch adoption across hyperscale data centers.

- Services and support are expanding at a 22.5% CAGR through 2035 as enterprises outsource centralized network management to managed-service providers.

• By Deployment Mode

- On-premise installations retained about 57.5% of the Software Defined Networking Market in 2025, favored by regulated industries requiring data-residency compliance.

- Cloud deployment is accelerating at a 24.1% CAGR through 2035, propelled by multi-cloud orchestration demand and virtual network overlay adoption.

• By Region

- North America led with a 39.5% revenue share in 2025, supported by federal zero-trust procurement mandates.

- Asia-Pacific is projected to grow at a 22.8% CAGR, the fastest of any region, fueled by 5G rollout timelines.

- The Software Defined Networking Market in Europe accounted for 26.0% of global revenue, driven by GAIA-X and open-source SDN controller platforms.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) Market Sizing combines a bottom-up revenue model (vendor shipping, subscription billings, and professional-services bookings) with top-down cross-validation through macroeconomic IT-spend ratios published by and[9]. Historical Figures (2021-2024) are actuals; 2025 is an estimate based on a base year; 2026-2035 are predictions based on a 21.5% CAGR.