360 Degree Camera Market Summary

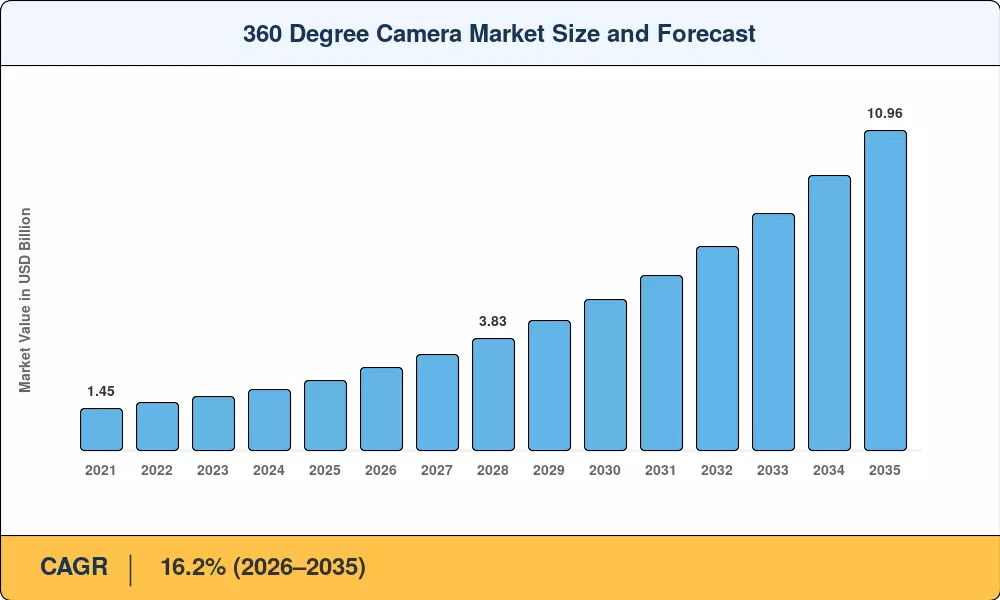

The 360 Degree Camera Market reached a valuation of USD 2.41 Billion in 2025 and is projected to grow from USD 2.84 Billion in 2026 to USD 10.96 Billion by 2035, registering a CAGR of 16.2% during the forecast period (2026–2035). Autonomous-vehicle development programs across North America and Europe now routinely specify surround-view camera rigs as a complement to LiDAR arrays, while fleet insurance mandates for 360° telematics-capable dash-cams are creating a durable OEM procurement cycle [1]. These twin catalysts have transformed the 360 Degree Camera Market from a niche consumer electronics category into a critical component of mobility and enterprise security infrastructure.

A broader technology shift is also accelerating demand. Legacy fixed-lens surveillance and single-viewpoint action cameras are giving way to multi-sensor omnidirectional systems capable of stitching real-time Ultra-HD feeds. Governments in the EU and the United States collectively allocated over USD 1.3 Billion in smart-city and connected-vehicle pilot funding between 2023 and 2025, much of it earmarking 360° perception hardware [2]. Meanwhile, media houses and esports producers are adopting glass-to-glass 360° production workflows to satisfy audiences streaming over 5G networks.

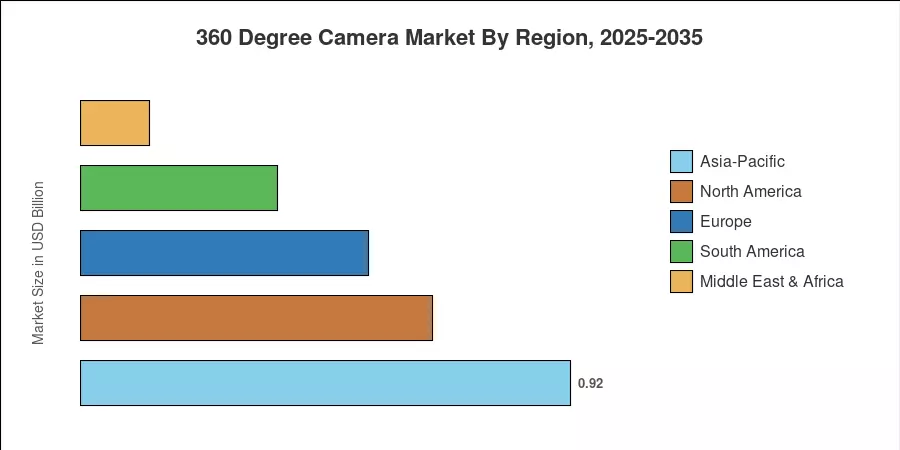

Asia-Pacific dominated the 360 Degree Camera Market with a 38.2% revenue share in 2025, driven by China's consumer-electronics manufacturing base and Japan's automotive-camera integration programs. The region also represents the fastest-growing geography at a 17.1% CAGR through 2035. North America held the second-largest share at 27.5%, anchored by defense training contracts and autonomous-vehicle pilots. Europe followed at 22.3%, with automotive safety regulation acting as the primary demand lever. As sub-7 nm imaging processors reach volume production and 8K sensor costs decline, the 360 Degree Camera Market is poised for sustained double-digit expansion through the forecast horizon.

Key Report Takeaways

• By Connectivity Type

- Wireless 360° cameras accounted for 61.1% of the 360 Degree Camera Market share in 2025, reflecting strong consumer preference for untethered, app-paired devices.

- Wired systems are expanding at a 15.8% CAGR (2026–2035), buoyed by professional broadcast and industrial inspection applications that require low-latency feeds.

• By Product Type

- Single-lens pocket cameras generated 49.2% of revenue in 2025, remaining the volume leader in the 360 Degree Camera Market.

- In-vehicle 360° dash-cams represent the fastest-growing product segment at a 16.6% CAGR, propelled by fleet-insurance mandates.

• By Resolution

- Ultra-HD 4K captured a 52.5% share of the 360 Degree Camera Market in 2025, serving as the mainstream resolution tier.

- Ultra-HD 8K and above is advancing at a 16.8% CAGR as professional content creators demand higher spatial resolution for VR post-production.

• By End-User

- Consumer applications held 34.8% of revenue in 2025.

- Automotive end-users are registering the strongest growth trajectory at a 17.3% CAGR through 2035.

• By Region

- Asia-Pacific led the 360 Degree Camera Market with 38.2% revenue share in 2025.

- North America contributed USD 0.66 Billion in 2025, underpinned by defense and AV-sector procurement.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with OEM procurement leads, component-supplier revenue disclosures, and trade-shipment databases cross-referenced with customs data from 22 countries. Historical figures (2021–2024) reflect reported actuals; the 2025 base year blends Q1–Q3 actuals with Q4 proprietary nowcasts. Forecast values (2026–2035) apply segment-level regression models calibrated to macroeconomic indicators and technology-adoption S-curves.