SEGMENTATION QUICK REFERENCE

| Dimension | Sub-Segments | Dominant Segment (2025) | Fastest Growing Segment (2026–2035) |

| Connectivity Type | Wireless, Wired | Wireless | Wired |

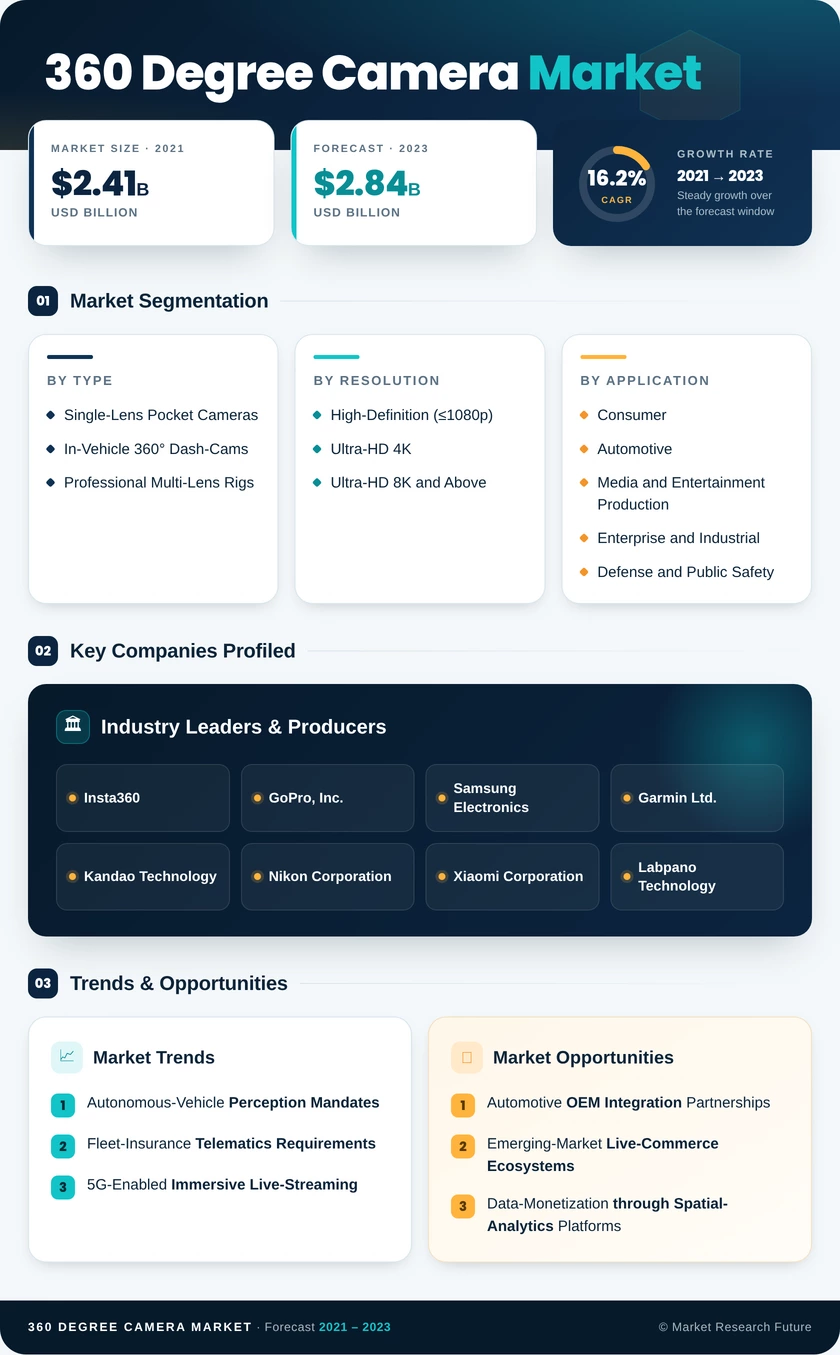

| Product Type | Single-Lens Pocket Cameras, In-Vehicle 360° Dash-Cams, Professional Multi-Lens Rigs | Single-Lens Pocket Cameras | In-Vehicle 360° Dash-Cams |

| Resolution | High-Definition (≤1080p), Ultra-HD 4K, Ultra-HD 8K and Above | Ultra-HD 4K | Ultra-HD 8K and Above |

| End-User | Consumer, Automotive, Media and Entertainment Production, Enterprise and Industrial, Defense and Public Safety | Consumer | Automotive |

| Distribution Channel | Online Marketplaces, Offline / Specialist Retail | Online Marketplaces | Offline / Specialist Retail |

MARKET SEGMENTATION OVERVIEW

By Connectivity Type

| Sub-Segment | Key Trend |

| Wireless | Wi-Fi 6E and Bluetooth 5.3 enabling near-wired throughput for prosumer workflows |

| Wired | Persistent demand from broadcast studios and industrial inspection requiring zero-latency feeds |

Wireless connectivity remains the default for consumer and prosumer 360° cameras, with app-paired ecosystems driving user stickiness. Wired variants continue to serve mission-critical enterprise and broadcast applications where latency tolerance is measured in single-digit milliseconds.

By Product Type

| Sub-Segment | Key Trend |

| Single-Lens Pocket Cameras | Sub-USD 300 price points expanding addressable market in emerging economies |

| In-Vehicle 360° Dash-Cams | Fleet-telematics mandates and ADAS integration driving double-digit growth |

| Professional Multi-Lens Rigs | 8K+ resolution and spatial-audio capture meeting XR content-studio specifications |

Single-lens pocket cameras lead on unit volume, while in-vehicle dash-cams are gaining revenue share as automotive OEMs embed 360° surround-view modules into standard ADAS packages. Professional rigs command premium ASPs above USD 5,000 and cater to cinematic VR, live-event broadcasting, and architectural documentation.

By Resolution

| Sub-Segment | Key Trend |

| High-Definition (≤1080p) | Declining share as 4K sensor costs approach parity |

| Ultra-HD 4K | Mainstream standard for consumer, enterprise, and automotive applications |

| Ultra-HD 8K and Above | Adoption accelerating in VR post-production and autonomous-vehicle simulation |

Ultra-HD 4K has become the resolution floor for new product launches, with sensor commoditization pushing even entry-level models toward 4K capture. The 8K-and-above tier is expanding as spatial-computing headsets and automotive simulation labs demand higher pixel density for depth-reconstruction workflows.

By End-User

| Sub-Segment | Key Trend |

| Consumer | Travel, social media, and lifestyle vlogging sustaining steady volume demand |

| Automotive | ADAS regulation and fleet-insurance incentives creating non-discretionary procurement |

| Media and Entertainment Production | Immersive live-event and esports broadcasting workflows expanding |

| Enterprise and Industrial | Digital-twin, facility-inspection, and training applications diversifying use cases |

| Defense and Public Safety | Simulation environments and perimeter-security systems driving long-cycle contracts |

Consumer applications anchor the market by volume, but automotive and enterprise verticals are growing faster and carry higher per-unit values. Defense procurement cycles, while smaller in total volume, provide multi-year revenue visibility that stabilizes supplier balance sheets.

By Distribution Channel

| Sub-Segment | Key Trend |

| Online Marketplaces | Amazon, JD.com, and brand-direct stores dominating consumer and SME purchasing |

| Offline / Specialist Retail | Professional buyers and enterprise accounts preferring hands-on demonstrations |

Online marketplaces serve as the primary discovery and purchase channel for consumer and small-business buyers. Offline specialist retailers and value-added resellers retain relevance for professional-grade equipment and enterprise accounts that require installation support, warranty customization, and volume-pricing negotiations.