Agave Syrup Market Summary

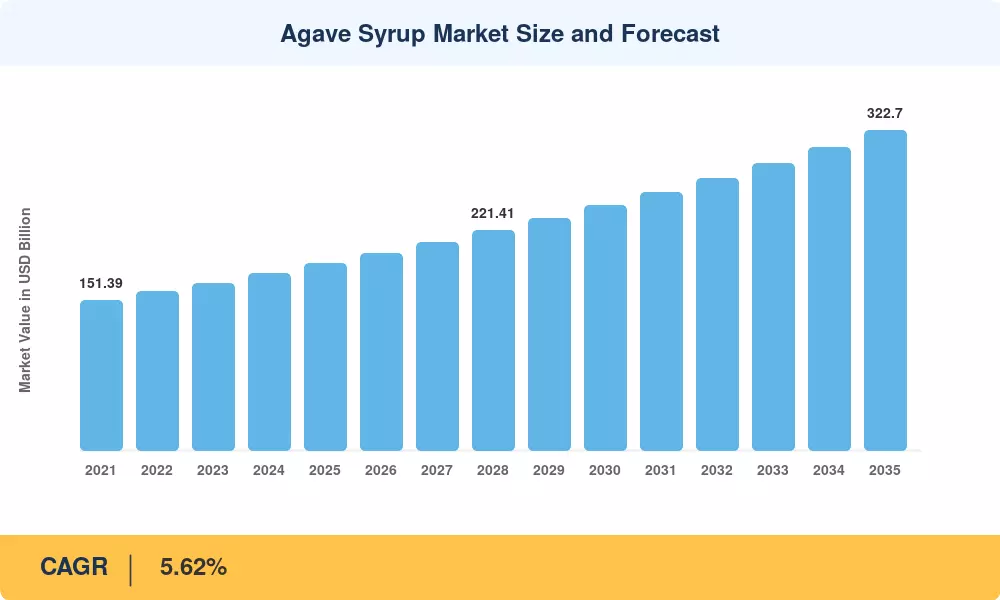

The agave syrup market is moving through a quiet but durable expansion, valued at USD 188.4 Million in 2025 and projected to open 2026 at roughly USD 198.9 Million before climbing to USD 322.7 Million by 2035, advancing at a 5.62% CAGR across the 2026–2035 forecast window. The trajectory tracks two reinforcing catalysts: the U.S. FDA's continued recognition of agave-derived sweeteners under "added sugars" labeling rules introduced under the Nutrition Facts overhaul, and Mexico's CONACYT-backed USD 42 million investment program announced in 2024 to modernize agave cultivation across Jalisco and Oaxaca. Together, these policies and capital signals are pulling the agave syrup market out of niche health-food shelves into mainstream foodservice procurement.

Production economics are being rewritten in real time. Legacy open-field harvesting and small-batch artisanal evaporation are giving way to closed-loop enzymatic hydrolysis lines and vacuum-concentration plants that lift output yield by 18–22%. Major beverage formulators have committed close to USD 310 million in supply-chain contracts over 2023–2025, locking in organic blue agave nectar volumes to hedge against sugar volatility flagged in the OECD-FAO 2025–2034 Outlook.

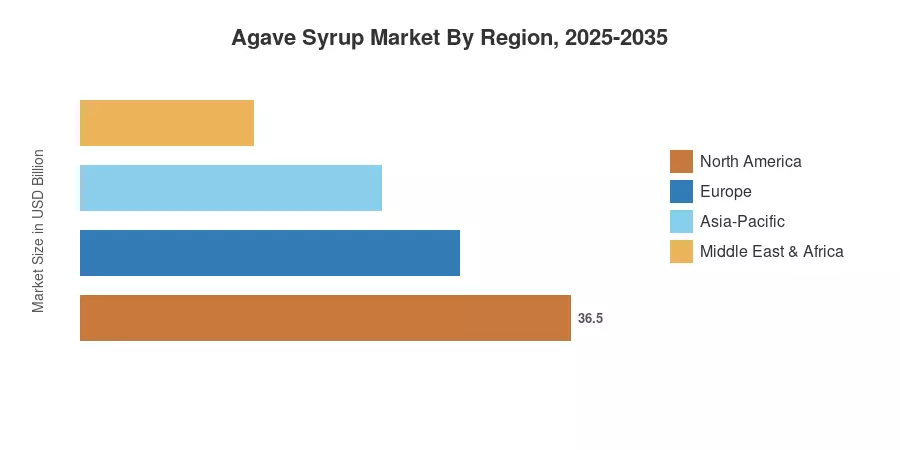

North America anchors the agave syrup market with a 32.8% share in 2025, while Asia-Pacific is the second-largest region, powered by a 6.21% CAGR. Europe sits as the third pillar, where clean-label regulation under EU 2019/787 keeps premium variants in steady rotation. The decade ahead will reward producers who pair traceability with scale.

Key Report Takeaways

• By Type

- Light agave syrup leads the agave syrup market with an estimated 56.4% revenue share in 2025, favored by beverage and bakery formulators

- Dark variants are projected at a 6.05% CAGR through 2035, lifted by craft cocktail demand and the tequila agave plant crop heritage halo

• By Category

- Organic agave is projected to reach USD 121.6 Million by 2035, driven by USDA NOP and EU organic certification uptake

- Conventional agave still anchors mainstream procurement, holding roughly 61% of 2025 volumes

• By Raw Material

- Blue agave dominates the agave syrup market raw material mix at approximately 72.5% in 2025

- Salmiana and other varieties are expanding at a combined 5.94% CAGR, opening alternative geographic supply

• By Distribution Channel

- Hypermarkets and supermarkets carry an estimated USD 78.3 Million of 2025 sales for the agave syrup market

- Online retail is the fastest-growing channel, posting a 7.85% CAGR through 2035

• By Region

- North America holds 32.8% of the global agave syrup market in 2025

- Asia-Pacific posts a 6.21% CAGR through 2035, the fastest globally

- Europe contributes roughly USD 51.8 Million in 2025 to the agave syrup market

Market Size and Forecast (2021–2035)

Historical figures draw on USDA Foreign Agricultural Service trade data, Mexico's Tequila Regulatory Council production reports, and customs filings cross-referenced with retailer scanner data. Forecast values apply a calibrated CAGR against demand elasticity for plant-based sweeteners, and the agave sweetener low glycemic appeal is documented in clinical reviews.

.webp?v=1782975675)