Agricultural Testing Market Summary

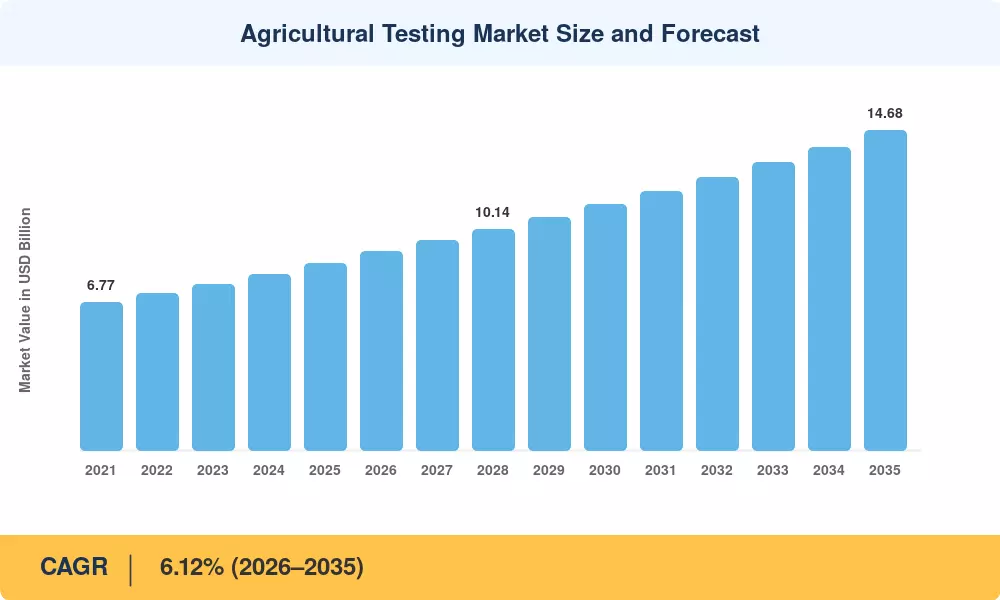

The agricultural testing market reached an estimated USD 8.45 billion in 2025 and is projected to expand from USD 9.12 billion in 2026 to USD 14.68 billion by 2035, registering a CAGR of 6.12% over the forecast period. Stricter maximum residue limit (MRL) enforcement across the EU and the United States—combined with the USDA's USD 300 million Organic Transition Initiative—has turned routine soil nutrient testing services and crop tissue analysis lab work into compliance necessities rather than optional expenditures [2]. Carbon-credit verification programs are also converting one-off soil assays into recurring annuity contracts, giving laboratories predictable revenue streams for the first time.

Legacy wet-chemistry workflows that once dominated pesticide residue agricultural testing are giving way to rapid immunoassay kits and portable near-infrared (NIR) spectrometers. The shift is not incremental: global investment in point-of-field diagnostics surpassed USD 1.2 billion in 2024, with lateral-flow devices for mycotoxin screening cutting turnaround from five days to under 30 minutes [3]. Laboratories pursuing ISO/IEC 17025 accreditation now treat blockchain-based certificate traceability as a baseline, especially for cross-border organic shipments where water quality farm testing documentation must accompany every consignment.

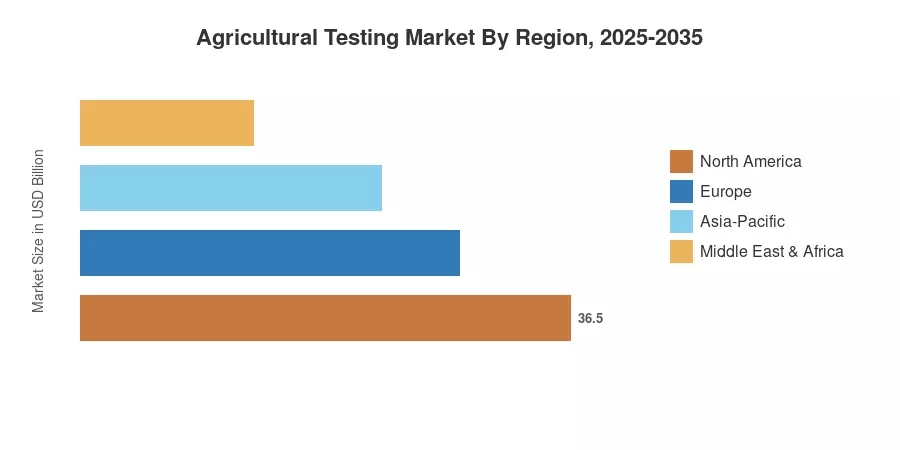

North America commands roughly 42% of 2025 revenue, anchored by the EPA's stringent drinking-water and irrigation runoff standards. Asia-Pacific is the fastest-growing region, advancing at a projected 9.5% CAGR through 2035 as India's Soil Health Card program and China's food-safety modernization drive expand demand for seed purity germination testing at scale. Europe holds the second-largest share at approximately 26%, buoyed by Farm-to-Fork traceability mandates. The agricultural testing market is poised for sustained double-digit regional growth in developing economies over the coming decade.

Key Report Takeaways

• By Sample Type

- Soil testing accounted for approximately 48% of the agricultural testing market in 2025, driven by carbon-sequestration measurement programmes and precision-agriculture adoption

- Seed testing is forecast to register a 9.4% CAGR through 2035, the fastest among sample categories, as phytosanitary certification requirements tighten globally

- Water quality farm testing represents the third-largest segment, valued at roughly USD 1.18 billion in 2025

• By Application

- Quality assurance commanded 57% of the agricultural testing market in 2025, reflecting the dominance of nutrient-profiling and grading contracts

- Safety testing is expanding at a 8.2% CAGR through 2035, fueled by pesticide residue agricultural testing mandates and mycotoxin screening protocols

• By Technology

- Rapid testing methods captured 59% of 2025 revenue, underscoring the shift toward lateral-flow and PCR-based field diagnostics

- Conventional methods still underpin complex crop tissue analysis lab services requiring mass spectrometry confirmation

• By Region

- North America led with 42% of global revenue in 2025, supported by the USDA and EPA regulatory framework

- Asia-Pacific is projected to reach USD 4.10 billion by 2035, growing faster than any other region

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines bottom-up laboratory revenue modelling with top-down regulatory-expenditure benchmarking. Historical figures (2021–2024) draw on audited annual reports from the top five testing networks, while forecast values (2026–2035) apply a calibrated CAGR with adjustments for anticipated regulatory phase-ins and technology substitution curves.