Air Cargo Market Summary

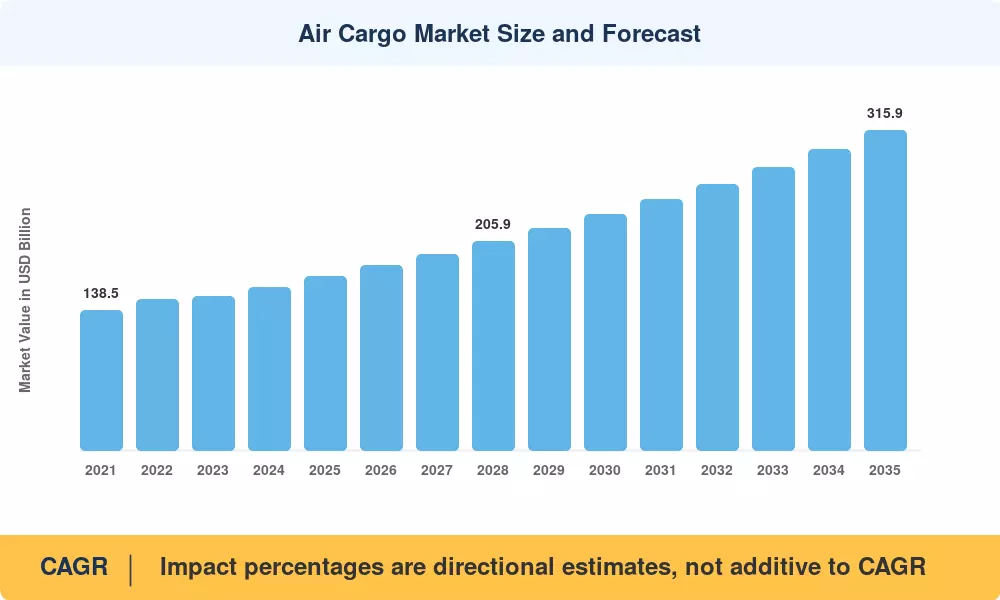

The Air Cargo Market stood at USD 171.40 Billion in 2025 and is projected to reach USD 315.90 Billion by 2035, advancing at a 6.30% CAGR through the forecast period (2026–2035). Two forces are pushing this trajectory: cross-border e-commerce volumes that doubled between 2019 and 2024 [1], and a global pharmaceutical supply chain that now routes over 15% of temperature-sensitive shipments by air [2]. Regulatory tailwinds — including ICAO's Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) Phase 2 mandates and the EU's ReFuelEU Aviation regulation requiring 6% sustainable aviation fuel (SAF) blending by 2030 — are reshaping the cost architecture of the Air Cargo Market without dampening underlying demand [10].

The technology transformation underway in the Air Cargo Market centers on digitization. Legacy paper-based airway bills and manual capacity allocation are giving way to ONE Record digital data-sharing frameworks and AI-powered dynamic pricing engines. IATA's target of 100% e-AWB adoption by end-2025 has accelerated investment in cargo management platforms, with airlines and forwarders collectively committing over USD 2.3 Billion to digital infrastructure upgrades between 2022 and 2024 [9]. Passenger-to-freighter (P2F) conversions reached a record 92 aircraft deliveries in 2024, adding critical widebody capacity as belly-hold supply from passenger flights continues to lag pre-pandemic levels on certain trade lanes [3].

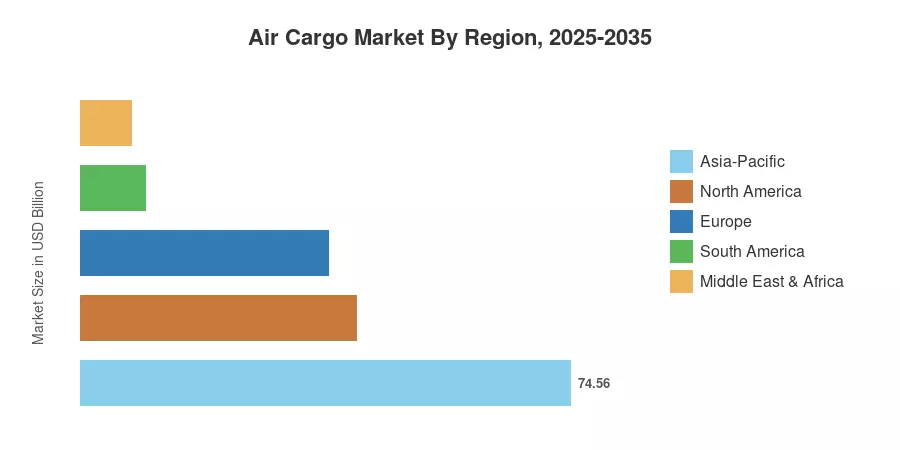

Asia-Pacific commands a 43.50% share of the Air Cargo Market, anchored by manufacturing export corridors in China and fast-expanding e-commerce fulfillment in India and Southeast Asia. The region is also the fastest-growing, posting a 6.80% CAGR through 2035. Europe holds roughly 22.00% of global volume, supported by pharmaceutical logistics hubs in Belgium and Germany, while North America — the second-largest region at 24.50% — benefits from an integrated express network density. The decade ahead will be defined by how quickly the Air Cargo Market absorbs SAF cost premiums while scaling digital booking and autonomous ground-handling capabilities.

Key Report Takeaways

• By Service

- Freight Forwarding held a 47.50% share of the Air Cargo Market in 2025, reflecting the dominance of third-party logistics orchestration in cross-border trade.

- Freight Transport is on track for a 5.40% CAGR through 2035, driven by airline-owned cargo divisions expanding dedicated freighter fleets.

• By Cargo Type

- General Cargo accounted for 57.90% of the Air Cargo Market in 2025, covering standard manufactured goods, textiles, and consumer electronics.

- International routes controlled the majority of volume, while Domestic traffic is advancing at a 5.80% CAGR as regional express delivery networks expand.

- Special Cargo is accelerating at a 5.10% CAGR, propelled by pharmaceutical cold chain and lithium-battery shipment protocols.

• By Destination

- International routes controlled the majority of volume

- While Domestic traffic is advancing at a 5.80% CAGR, as regional express delivery networks expand.

• By Region

- Asia-Pacific accounted for a 43.50% share of the Air Cargo Market, led by China's export manufacturing corridors and India's digital commerce surge.

- North America contributed 24.50% of global volume in 2025, anchored by integrated express carrier networks.

Market Size and Forecast (2021–2035)

Market Research Future's projections integrate bottom-up revenue models from airline cargo filings, freight forwarder disclosures, and customs trade databases across 45 countries. Historical values (2021–2024) reflect audited industry data, while forecast estimates (2026–2035) apply econometric modeling calibrated to GDP growth, trade-volume elasticity, and capacity deployment schedules [1][7].