Aromatics Market Summary

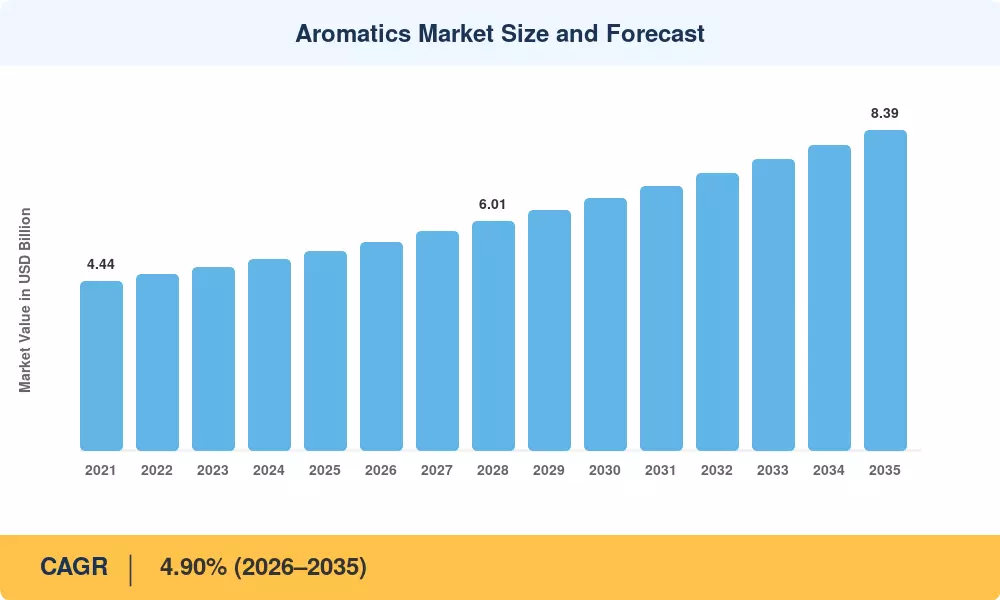

The global Aromatic Market was valued at USD 5.22 Billion in 2025 and is projected to grow from USD 5.46 Billion in 2026 to USD 8.39 Billion by 2035, registering a CAGR of 4.90% during the forecast period (2026–2035). Tightening chemical safety regulations across the EU and North America — particularly REACH amendments targeting sensitizer disclosure — and the rapid commercialization of bio-based production routes are reshaping cost structures and product development timelines across the Aromatic Market. Corporate sustainability pledges from consumer-goods multinationals have channeled an estimated USD 2.8 billion in cumulative R&D spending toward green chemistry platforms since 2022 [1].

Fermentation and enzymatic conversion approaches are replacing, to a growing extent, the legacy petrochemical synthesis routes. Microbial platforms are currently generating pilot to commercial quantities of limonene, linalool and santalene, a transition hastened by the USDA BioPreferred Program and the European Commission’s Chemicals Strategy for Sustainability [2]. Some companies have realized 15-20% unit-cost savings as they move terpene lines to yeast-based fermentation, an indication of a more fundamental shift away from crude-oil-linked feedstocks.

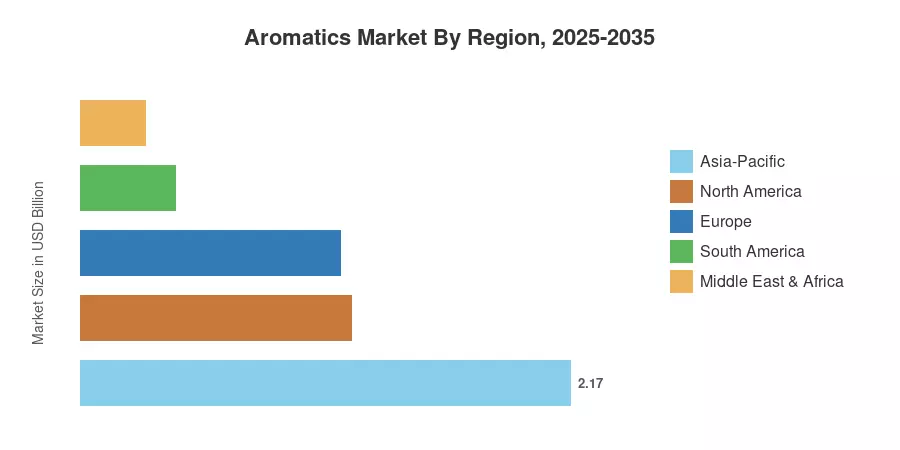

Asia-Pacific holds the greatest share of the Aromatic Market, with 41.5% of 2025 revenue, driven by a double-digit increase in prestige fragrance consumption in China and a developing specialty-chemicals production base in India. The region also has the fastest CAGR at 6.10% until 2035. Europe is the second largest market at 22.0%, supported by the fragrance tradition of France and the industrial flavoring cluster in Germany. The Aromatic Market is expected to continue its quality-driven growth over the next decade with premiumization trends and regulatory harmonization remaining on a convergent path.

• By Type

- Terpenes accounted for 41.2% of the Aromatic Market in 2025, bolstered by scalable microbial manufacturing platforms.

- Musk chemicals are forecast to expand at a 5.35% CAGR through 2035, driven by demand for biodegradable macrocyclic and alicyclic fixatives.

• By Application

- Cosmetics and toiletries held 36.6% revenue share in the Aromatic Market in 2025, reflecting global personal-care premiumization.

- Fine fragrances are projected to register a 5.52% CAGR through 2035, propelled by niche-brand proliferation and artisanal perfumery.

• By Region

- Asia-Pacific captured 41.5% of the Aromatic Market in 2025 and leads all regions with a 6.10% CAGR forecast.

- North America contributed 23.0% of 2025 revenue, underpinned by clean-label reformulation mandates.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates supply-side production data, trade-flow analysis, and downstream consumption surveys across 25 countries. Historical figures (2021–2024) draw on audited financial disclosures and customs databases; forecast values apply a constant-CAGR trajectory anchored to the 2025 base year.