Automated Border Control Market Summary

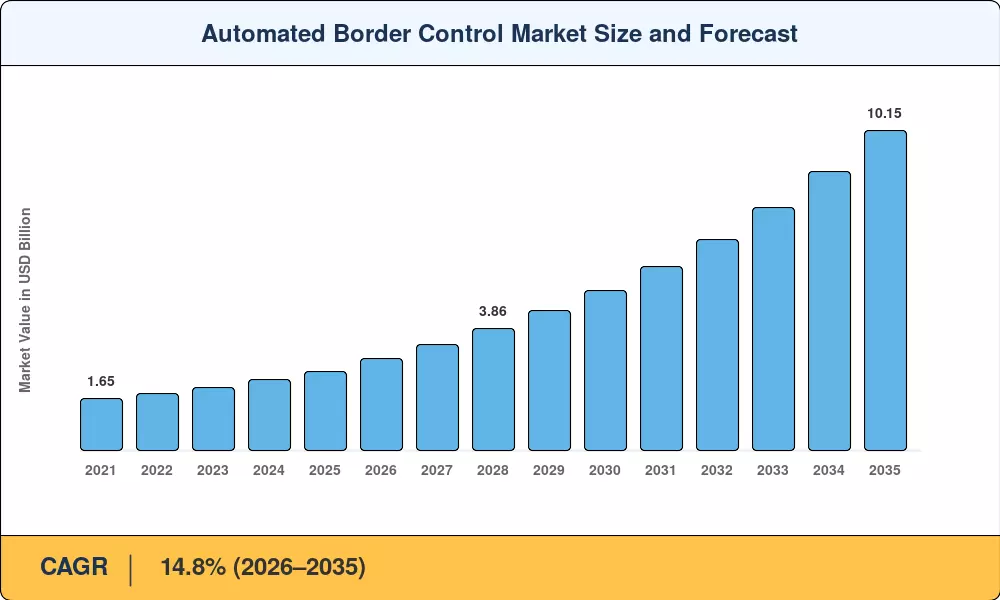

The Automated Border Control Market reached USD 2.52 billion in 2025 and is projected to grow from USD 2.93 billion in 2026 to USD 10.15 billion by 2035, registering a CAGR of 14.8% during the forecast period (2026–2035). Three policy-level forces are converging to push this acceleration: the European Union's Entry/Exit System (EES) mandate, which requires biometric verification at all Schengen external borders [1]; post-pandemic passenger volumes that surpassed 2019 levels by late 2024 [2]; and dedicated public-sector funding exceeding USD 4.5 billion earmarked globally for smart-border programs through 2030 [3]. Governments are no longer piloting automated border solutions — they are scaling them into national infrastructure.

The ongoing technology transition is moving away from manual document verification and towards officer-dependent queuing and integrated gate and kiosk architectures, which combine facial recognition with machine-readable travel documents. Legacy methods such as barcode scanners and single factor authentication are being replaced with multi-modal platforms combining iris, fingerprint and facial modalities in a single verification event of less than 12 seconds [4]. The EU alone invested EUR 1.3 billion on its Smart Borders Package, basing procurement on compatible hardware-software bundles [5].

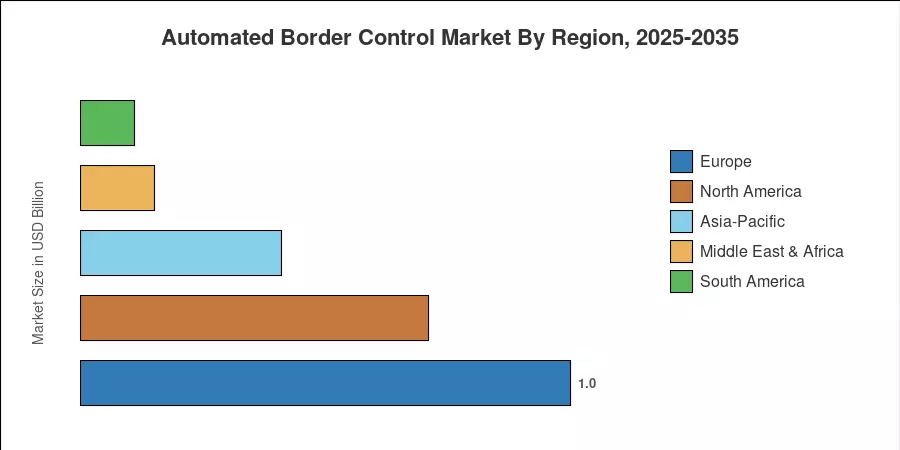

Europe accounts for some 39.8% of total revenue, driven by the Schengen-wide EES implementation and Frontex coordination duties. Asia-Pacific is the fastest developing region helped by airport expansion initiatives in China, India and ASEAN countries. The second is North America with a share of about 28%, driven by the biometric exit program of the U.S. Customs and Border Protection and the upgrade of NEXUS in Canada [6]. Geopolitical volatility and increasing quantities of cross-border travel will maintain identity assurance at the top of government procurement agendas until 2035, which will help the Automated Border Control Market.

Key Report Takeaways

• By Type & Offering

- ABC e-gates captured approximately 61% of the Automated Border Control Market in 2025, reflecting widespread airport deployment across Europe and North America.

- Software solutions are forecast to expand at a 14.9% CAGR through 2035 as cloud-native analytics and AI-driven risk scoring gain traction.

• By Solution Model & End-Use Application

- Fully automated systems accounted for around 65% of the Automated Border Control Market share in 2025, as governments prioritize touchless processing.

- Semi-automated models are advancing at a significant CAGR during the forecast period.

• By Geography

- Europe dominated the Automated Border Control Market with close to 39.8% of global revenue, anchored by the EES regulation.

- Asia-Pacific is projected to register the fastest CAGR through 2035, with China and India collectively accounting for over half the region's demand.

Automated Border Control Market Size and Forecast (2021–2035)

Market Research Future (MRFR) formulated the forecast model on the basis of bottom-up aggregation of revenue from hardware, software, and services procurement by border agencies in 45+ countries, triangulated with top-down macroeconomic indicators including international passenger arrivals (UNWTO) and government border-security budget disclosures.