Automated Material Handling Market Summary

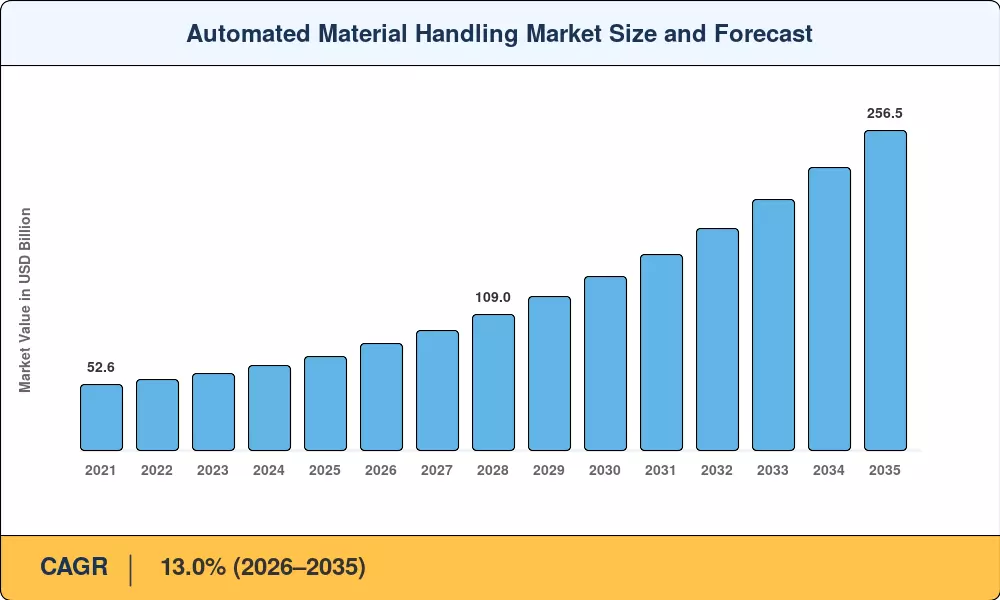

The Automated Material Handling Market was valued at USD 75.6 Billion in 2025 and is projected to reach USD 85.4 Billion in 2026 before climbing to USD 256.5 Billion by 2035, registering a CAGR of 13.0% during the forecast period (2026–2035). Accelerating e-commerce order intensity — global parcel volumes topped 160 billion units in 2024 [1] — has combined with tightening warehouse-labor availability across OECD economies to push logistics operators toward capital-intensive automation cycles. Government-backed Industry 4.0 programs in Germany, Japan, and China are funneling over USD 18 billion annually into smart-factory upgrades, directly benefiting the Automated Material Handling Market [2].

A sweeping technology transition is underway. Legacy fixed-conveyor lines and manual pallet-handling operations are giving way to AI-orchestrated fleets of autonomous mobile robots, cloud-based warehouse-execution platforms, and vision-guided picking systems. Amazon alone committed over USD 750 million to robotics R&D in 2024, while Walmart's next-generation distribution centers now run on end-to-end automated fulfillment architectures [3]. The shift is not merely about speed — it is about data-rich operational visibility that enables real-time throughput optimization.

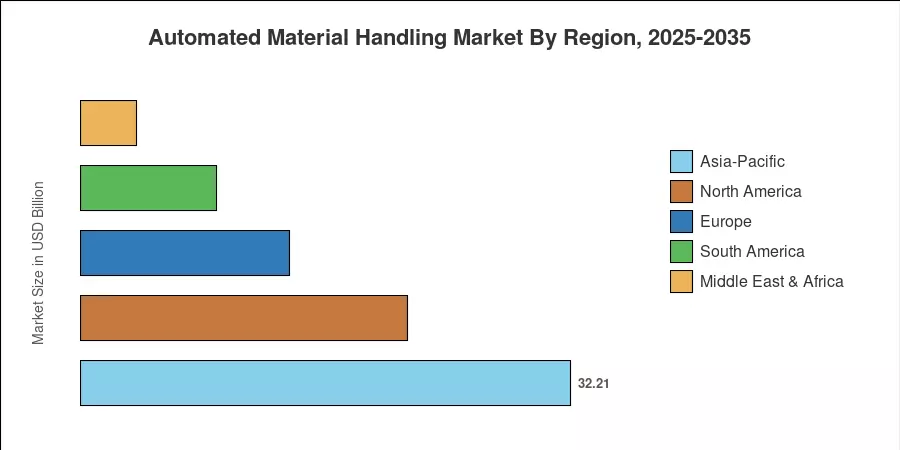

Asia-Pacific commands roughly 42.6% of global revenue and leads as both the dominant and fastest-growing region for the Automated Material Handling Market, expanding at a 13.6% CAGR through 2035. North America holds approximately 28.5% share, anchored by U.S. third-party logistics (3PL) modernization spending. Europe follows with an 18.2% share, driven by EU supply-chain-resilience directives. As labor costs rise across Southeast Asia and Latin America, investment in automated material handling infrastructure is set to intensify further through the decade [4].

Key Report Takeaways

• By Product Type

- Hardware retained a 65.9% revenue share of the Automated Material Handling Market in 2025, reflecting strong demand for robotic arms, shuttle systems, and palletizers.

- Software solutions are forecast to expand at a 19.6% CAGR through 2035, driven by warehouse-management and fleet-orchestration platform adoption.

• By Equipment Type

- Mobile robots captured 32.6% of equipment-level revenue in the Automated Material Handling Market during 2025.

- Autonomous Mobile Robots (AMRs) are advancing at a 28.3% CAGR, the fastest growth segment across all equipment categories.

• By End User

- Retail, warehousing, and distribution operators accounted for a 25.0% share of the Automated Material Handling Market in 2025.

- Food and beverage end users are projected to grow at an 18.4% CAGR through 2035 as cold-chain automation scales.

• By Region

- Asia-Pacific led the Automated Material Handling Market with 42.6% revenue share in 2025.

- North America represented the second-largest region, contributing approximately USD 21.5 Billion in 2025 revenue.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology integrating top-down macroeconomic modeling, bottom-up company-revenue aggregation, and demand-side order-book analysis from over 120 logistics operators. Historical figures (2021–2024) use audited annual reports; the 2025 base year blends Q1–Q3 actuals with consensus analyst estimates; and the 2026–2035 forecast applies a validated compound-growth framework calibrated against capex-cycle indicators.