Automotive Cybersecurity Market Summary

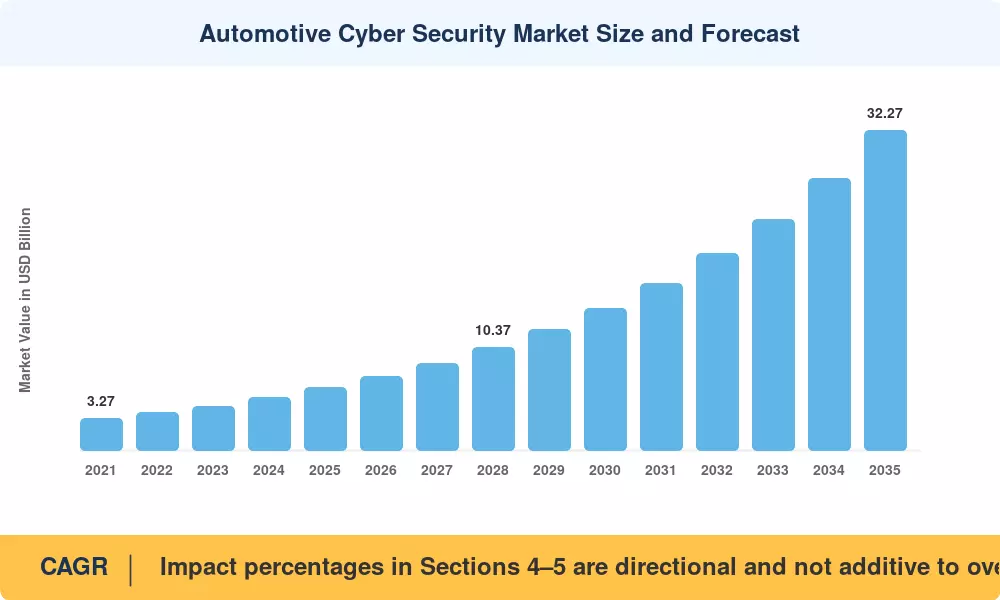

The Automotive Cybersecurity Market reached USD 6.38 Billion in 2025, and Market Research Future projects it will climb from USD 7.50 Billion in 2026 to USD 32.27 Billion by 2035, expanding at a 17.6% CAGR across the forecast window. This acceleration reflects a compliance-driven purchasing cycle that took shape after 54 countries began enforcing UN Regulation No. 155, mandating cybersecurity management systems for every new vehicle type approval [2]. OEMs that once treated cybersecurity as a bolt-on now treat it as a gating criterion for market access.

The industry's pivot toward software-defined vehicles is rewriting security architectures from the silicon up. Legacy point solutions guarding individual electronic control units are giving way to centralized domain-controller platforms capable of orchestrating real-time threat detection across 100+ ECUs per vehicle [3]. Cloud-delivered fleet analytics have become indispensable for managing over-the-air update integrity, and global automakers allocated an estimated USD 4.2 billion to cybersecurity R&D in 2024 alone [4].

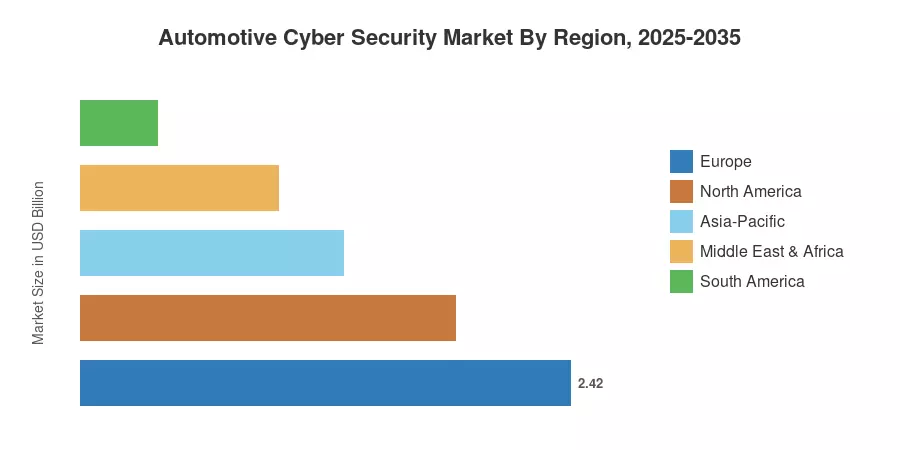

Europe commands the largest share of the Automotive Cybersecurity Market at roughly 38% of 2025 revenue, anchored by stringent EU type-approval deadlines. Asia-Pacific is the fastest-growing region with a projected CAGR exceeding 20%, driven by China's surging connected-vehicle fleet and India's emerging regulatory framework. North America holds the second-largest position at approximately 29% share, underpinned by NHTSA guidance and aggressive OEM investment cycles. As Level 3+ autonomy enters production, the Automotive Cybersecurity Market is set for a structural expansion that will outlast any single regulatory cycle.

Key Report Takeaways

• By Security Domain

- Vehicle/On-board Systems Security held a 49.2% revenue share of the Automotive Cybersecurity Market in 2024, reflecting concentrated spend on in-vehicle intrusion prevention.

- Production (OT and IIoT) Security is forecast to expand at a 22.8% CAGR through 2035, as smart-factory digitization widens the attack surface beyond the vehicle itself.

• By Solution Type

- Embedded Security Software accounted for a 40.5% share of the Automotive Cybersecurity Market in 2024, driven by OEM demand for tamper-proof firmware layers.

- Cloud-based Security Platforms are projected to register a 23.1% CAGR through 2035.

• By End User

- OEMs commanded 47.8% of the Automotive Cybersecurity Market in 2024, internalizing security operations to meet type-approval mandates.

- Smart-factory operators represent the fastest-growing end-user segment at a 22.0% CAGR.

• By Deployment

- On-premises solutions accounted for 43.8% of the Automotive Cybersecurity Market share in 2024.

- Cloud-based platforms are forecast to register a 24.4% CAGR to 2035.

• By Region

- Europe led with USD 2.42 billion in 2025 revenue, while Asia-Pacific is expected to grow fastest through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue estimates from OEM procurement disclosures, Tier-1 supplier filings, and cybersecurity vendor earnings with top-down macroeconomic adjustments. Historical figures (2021–2024) reflect actuals; 2025 is the calibrated base year; 2026–2035 values apply a constant 17.6% CAGR[4].