Automotive Tire Market Summary

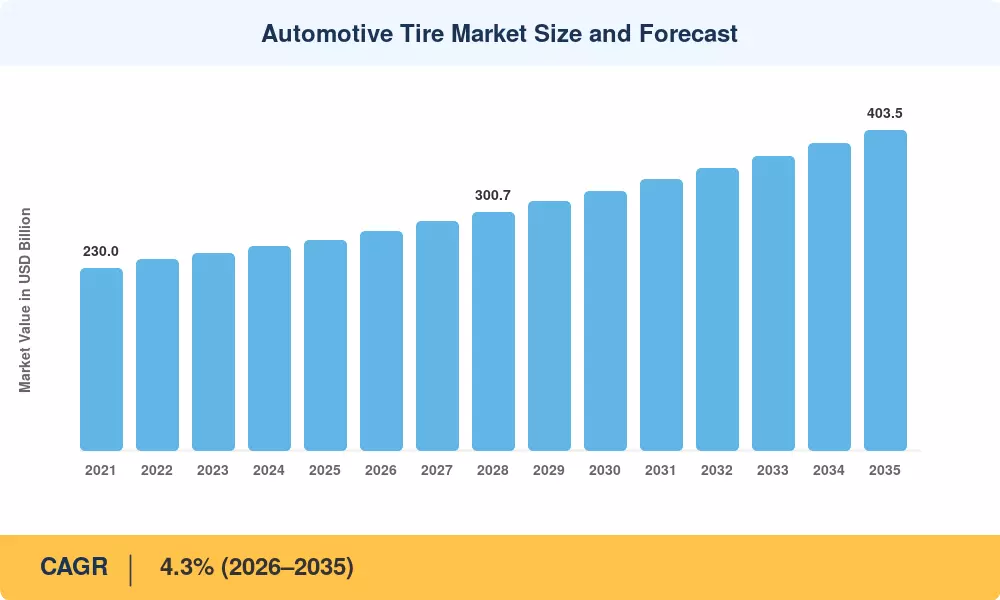

The global Automotive Tire Market was valued at USD 265.0 billion in 2025 and is projected to grow from USD 276.4 billion in 2026 to USD 403.5 billion by 2035, registering a CAGR of 4.3% during the forecast period (2026–2035). Two forces are reshaping spending patterns across the Automotive Tire Market: the rapid expansion of the global vehicle parc—expected to exceed 1.8 billion units by 2030 [1]—and tightening fuel-economy regulations that push OEMs toward lower rolling-resistance compounds. The EU's revised tire-labeling regulation (EU 2020/740) and the U.S. NHTSA CAFE standards for 2027 model-year vehicles both incentivize premium tire adoption, anchoring demand growth well above the GDP trajectory [2].

The Automotive Tire Market is technologically shifting from bias-ply constructions to radial layouts in almost all vehicle classes. Meanwhile, connected-tire sensor integration, which uses embedded RFID and TPMS 2.0 chips to transmit tread-depth, temperature and load information in real time, has garnered more than USD 1.2 billion joint R&D funding from the top five manufacturers since 2022 [3]. The EV push is amplifying this change, with the EV-specific tire, designed for higher torque loads and lower cabin noise, becoming a fast-growing specialty within replacement channels.

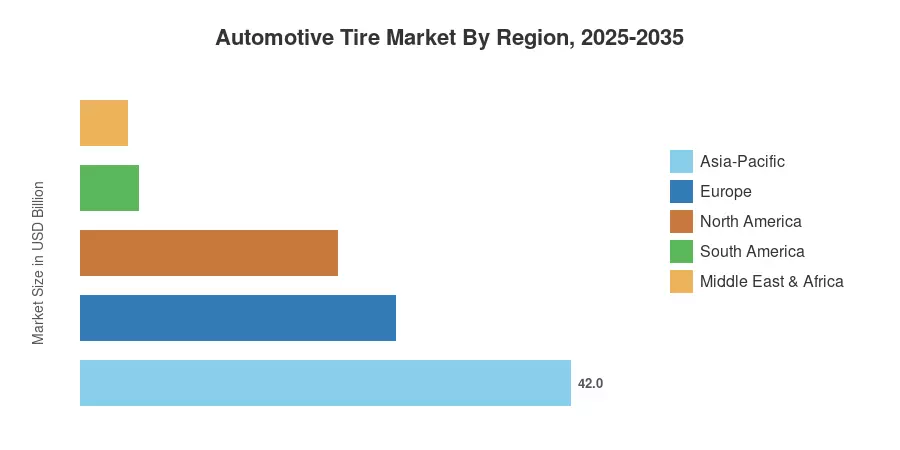

The Asia-Pacific region holds the largest revenue share of over 42% in the Automotive Tire Market, owing to the large production of vehicles in China and India. The region also has the highest CAGR through 2035 at 5.1%. Europe contributes approximately 27% of the worldwide value, with strict safety regulations and a mature replacement cycle, whereas North America is next with approximately 22% of the global value. With global electrification ramping up, the Automotive Tire Market is positioned at the confluence of material science innovation and regulatory compliance for the next decade.

Key Report Takeaways

• By Tire Type

- Radial tires command over 88% of the global Automotive Tire Market revenue, sustained by superior fuel efficiency and OEM standardization across passenger and commercial vehicles.

- Bias-ply tires retain a niche CAGR of 2.1% in agriculture and off-highway segments where puncture resistance outweighs fuel economy.

• By Sales Channel

- The replacement channel generates approximately USD 165 billion, reflecting the 3–5 year replacement cycle that keeps aftermarket volumes structurally high in the Automotive Tire Market.

- OEM sales are forecast to grow at 4.8% CAGR as rising global vehicle production lifts factory-fit demand.

• By Geography

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) has built the Automotive Tire Market size series by triangulating manufacturer revenue disclosures, customs trade-flow databases, and regional tire-industry association shipment statistics (ETRMA, RMA, ATMA). Historical data (2021-2024) are actual reported values adjusted for currency fluctuation. The base year (2025) is estimated from trailing-twelve-month results. Forecast figures (2026–2035) are based on a steady 4.3% CAGR, using vehicle-parc growth modeling and replacement-cycle analysis as a starting point.