Automotive Wiring Harness Market Summary

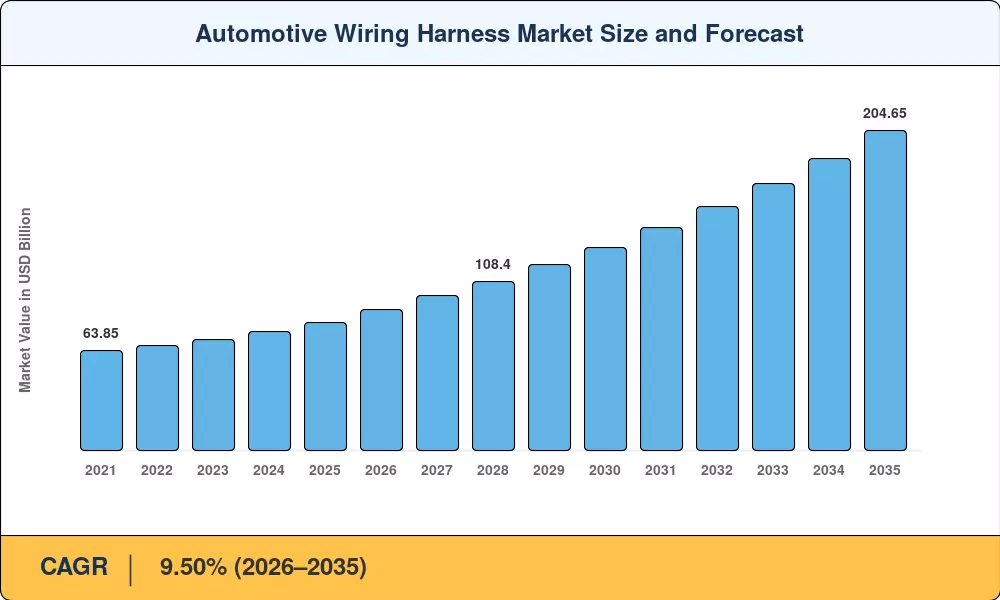

The Automotive Wiring Harness Market was valued at USD 82.10 billion in 2025 and is projected to grow from USD 90.40 billion in 2026 to USD 204.65 billion by 2035, registering a CAGR of 9.50% during the forecast period (2026–2035). Stricter vehicle emission mandates — including the European Union's Euro 7 proposal and China's Phase VI-B standards — are accelerating the shift toward electrified powertrains, each of which carries roughly twice the harness content of a conventional internal combustion engine vehicle [1]. Meanwhile, the U.S. Inflation Reduction Act has unlocked over USD 12 billion in EV-component manufacturing incentives, directly stimulating domestic harness capacity additions across Michigan, Tennessee, and Georgia [2].

The Automotive Wiring Harness Market is at the core of a fundamental technical shift. Domain-based and zonal electrical topologies, which condense data and power distribution into fewer, higher-capability trunk lines, are replacing legacy point-to-point wiring architectures, where individual circuits run from each sensor or actuator to a central junction box. Automakers from Volkswagen to Hyundai and GM have pledged over USD 1 billion apiece for platform-level electrical-architecture redesigns for 2026–2028 model years [3].

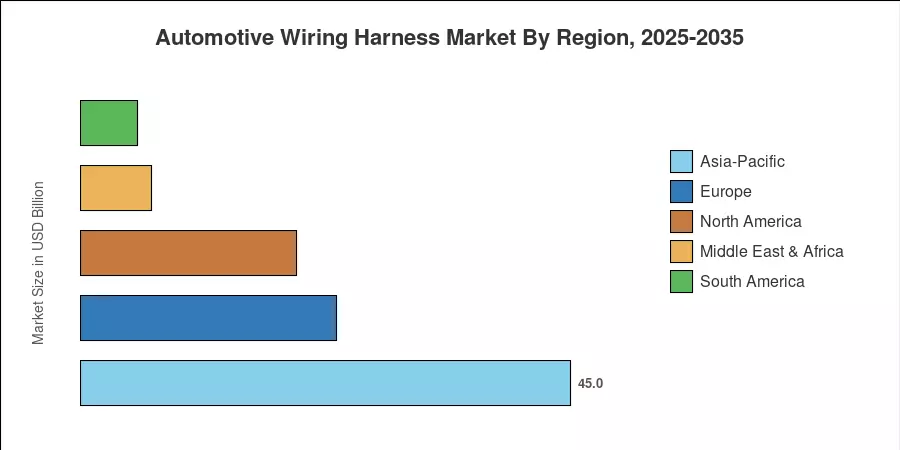

The Asia-Pacific region has the largest share of ~45.0% in the Automotive Wiring Harness Market, owing to the high EV production base in China and a growing industrial corridor in India along the Delhi – Mumbai Industrial Corridor [4]. The Middle East & Africa area is expected to have the highest CAGR of 12.60% over the projected period. The growth of this region is attributed to the burgeoning automotive cluster of Morocco and the Automotive Masterplan 2035 incentives in South Africa [5]. Europe is the second largest market, with a share of around 23.5%, with OEM giants in Germany driving demand for lightweight aluminum conductors and high-voltage cable systems.

Key Report Takeaways

• By Application Type

- Body, lighting, and cabin wiring harnesses captured a 32.9% share of the Automotive Wiring Harness Market in 2025, reflecting the growing proliferation of ambient lighting, seat actuation, and ADAS sensor feeds across mid-tier vehicle platforms.

- Charging and power supply harnesses are expanding at a 27.2% CAGR through 2035, as every new BEV platform requires dedicated high-voltage cable runs from battery pack to inverter and onboard charger.

• By Conductor Material

- Copper conductors accounted for 88.8% of the Automotive Wiring Harness Market by material value in 2025, though rising LME copper prices are accelerating aluminum substitution programs among European Tier-1 suppliers.

• By Geography

- Asia-Pacific captured a 45.0% share of the Automotive Wiring Harness Market in 2025, led by China, Japan, and India's combined automotive output exceeding 55 million vehicles annually.

- The Middle East & Africa region is projected to register the highest regional CAGR at 12.60%, buoyed by greenfield harness plants in Morocco, Egypt, and Ethiopia.

Automotive Wiring Harness Market Size and Forecast (2021–2035)

Market Research Future’s projections are based on deep-dive primary interviews with tier 1 harness makers, OEM procurement data and trade-flow analysis from UN Comtrade. The historical values (2021–2024) are validated to annual reports of leading public companies, and the forecast values (2026–2035) are extrapolated with a bottom-up model anchored on vehicle production forecasts from OICA and IHS Markit, corrected by harness-content-per-vehicle trends by powertrain type [6].