Beauty Tools Market Summary

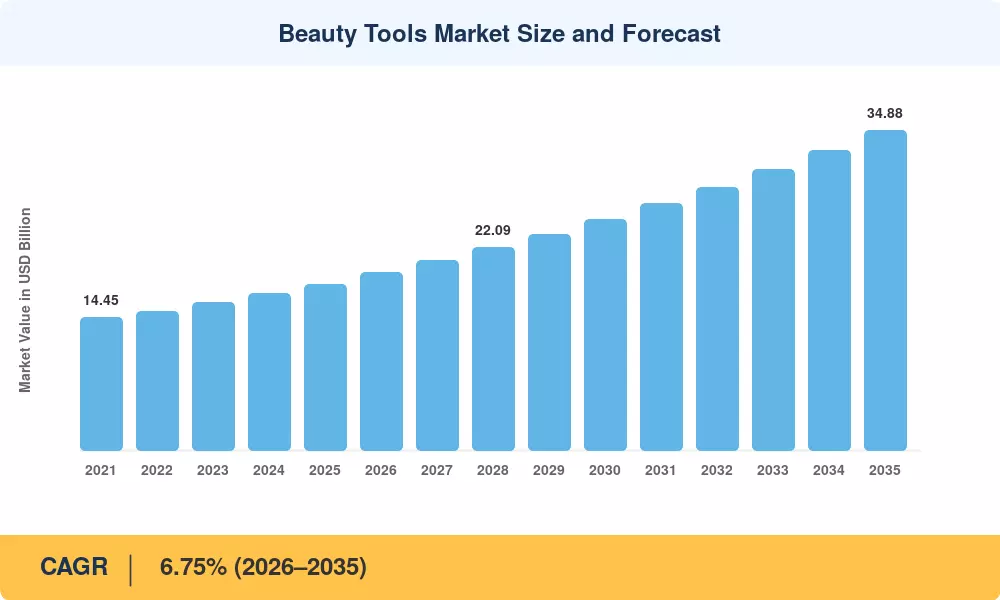

The Beauty Tools Market reached an estimated USD 18.07 billion in 2025 and is projected to climb to USD 19.38 billion in 2026 before expanding to USD 34.88 billion by 2035, registering a CAGR of 6.75% across the 2026–2035 forecast window. Two catalysts are accelerating this trajectory: rising disposable incomes across emerging economies — the World Bank recorded a 4.2% average income growth in middle-income countries during 2023–2024 [1] — and the rapid consumerization of professional-grade skincare and hairstyling routines at home, fueled by social-media tutorial culture [2].

The Beauty Tools Market is experiencing a technology-driven change from simple manual implements to smart, app-connected products. Electronic facial equipment that can analyze skin in real time is replacing simple curling irons, old-fashioned combs and passive skincare rollers, as are sensor-equipped hair products with customizable heat algorithms. In 2024, global consumer spending on personal care gadgets hit USD 8.5 billion, a number that highlights the extent to which technology has become intertwined in regular grooming [3].

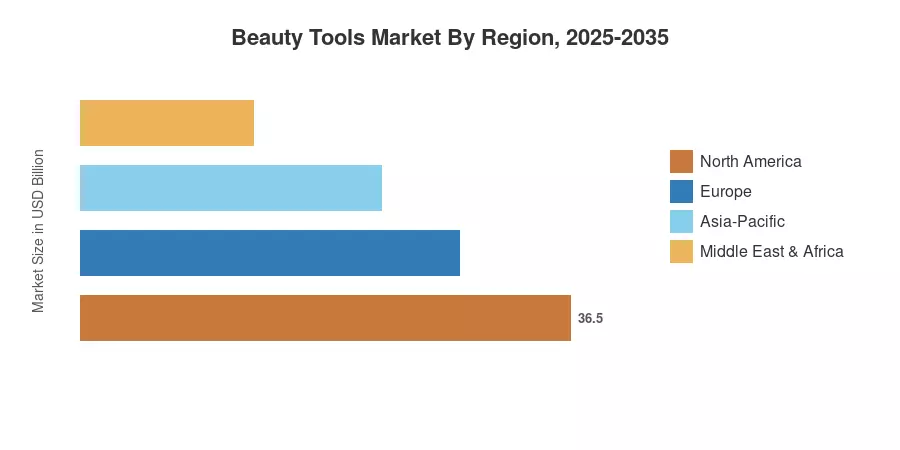

Asia-Pacific accounts for the biggest part of the Beauty Tools Market with around 38.2% of 2025 revenue owing to the dense beauty-conscious populace in China, Japan and South Korea. The Middle East & Africa area is projected to register the highest CAGR of 8.72% through 2035, owing to urbanization and premium brand penetration in the GCC countries. Europe has the second greatest regional share at 22.7%, led by Germany, France and the Nordic countries with innovation in sustainability. As customization technology matures and distribution channels digitize, the Beauty Tools market is expected to continue its double-digit expansion across numerous high-growth sectors.

Key Report Takeaways

• By Product Type

- Hair Tools dominated the Beauty Tools Market with a 62.4% share in 2025, reflecting strong global demand for advanced dryers, straighteners, and curling devices.

- Facial Tools are projected to register a CAGR of 8.07% during 2026–2035, the fastest-growing product category.

- Nail Tools and Makeup Tools collectively account for the remaining share, with makeup applicators gaining ground through e-commerce-driven awareness.

• By Distribution Channel

- Offline Retail Stores captured 48.1% of the Beauty Tools Market in 2025, though the channel's dominance is narrowing as digital commerce accelerates.

- Online Retail Stores are advancing at a 8.48% CAGR through 2035, making them the fastest-expanding sales channel.

• By Geography

- Asia-Pacific contributed 38.2% of the global Beauty Tools Market revenue in 2025, making it the single largest regional contributor.

- The Middle East & Africa region is projected to post the highest regional CAGR of 8.72% through 2035.

Market Size and Forecast (2021–2035)

The sizing methodology of Market Research Future (MRFR) is based on bottom-up revenue modeling using 120+ company filings, customs-trade databases, and proprietary retailer panel data, cross-validated with top-down macroeconomic variables such as household spending on personal care and beauty. Historical data represent reported sales. Forecast forecasts are derived from a calibrated compound growth model adjusted for regional demand elasticity and channel migration trends.

.webp?v=1783518715)